Bangladesh's graduation from LDC

A 'development surprise'

Dr. Atiur Rahman | Monday, 12 November 2018

![]() Defying all the pessimistic predictions like `an international basket case' or ` a test case of development' Bangladesh is now all set to graduate from the group of least developed countries (LDCs) to that of developed countries by 2024. Bangladesh has been carrying the baggage of being LDC for more than four decades which is considered to be `the poorest and the most vulnerable'. "These countries are characterised as caught in a low-income trap, and risk failure in their efforts to overcome poverty and deprivation; they predominantly depend on primary commodities for production and export with extremely inadequate opportunities for diversification and are heavily reliant on foreign aid due to limited economic activity." (Razzaque, A, 'The Tipping Point: Bangladesh's Graduation From The Group Of Least Developed Countries', Harvard International Review, Summer 2018). This graduation is overseen and managed by the Committee for Development Policy (CDP), a group of independent experts reporting to the United Nations Economic and Social Council (ECOSOC). Bangladesh achieved this qualification from the latest round of CDP review in last March satisfying all the three criteria, namely, per capita income, human assets and economic vulnerability. This was, indeed, a rare feat for Bangladesh as it could meet simultaneously all the three criteria.

Defying all the pessimistic predictions like `an international basket case' or ` a test case of development' Bangladesh is now all set to graduate from the group of least developed countries (LDCs) to that of developed countries by 2024. Bangladesh has been carrying the baggage of being LDC for more than four decades which is considered to be `the poorest and the most vulnerable'. "These countries are characterised as caught in a low-income trap, and risk failure in their efforts to overcome poverty and deprivation; they predominantly depend on primary commodities for production and export with extremely inadequate opportunities for diversification and are heavily reliant on foreign aid due to limited economic activity." (Razzaque, A, 'The Tipping Point: Bangladesh's Graduation From The Group Of Least Developed Countries', Harvard International Review, Summer 2018). This graduation is overseen and managed by the Committee for Development Policy (CDP), a group of independent experts reporting to the United Nations Economic and Social Council (ECOSOC). Bangladesh achieved this qualification from the latest round of CDP review in last March satisfying all the three criteria, namely, per capita income, human assets and economic vulnerability. This was, indeed, a rare feat for Bangladesh as it could meet simultaneously all the three criteria.

There will be another round of such a review in 2021 and if Bangladesh can again meet the graduation criteria, which is most likely, it would be fully eligible to graduate from the LDC group to the next group i.e. of developing countries by 2024. So far five countries including Botswana, Cape Verde, the Maldives, Somoa and Equatorial Guinea have been able to make this transition. Bangladesh is now poised for the same transition.

Compared to what it was in the 1970s Bangladesh made a spectacular journey of socioeconomic transformation, particularly during the last decade for which many experts tend to call it a `development surprise'. What made this possible? Both positive internal and external factors made this stunning transformation a reality. Of the internal beneficial factors one may like to include stable macro- economy, large expansion of the private sector, consistent and robust growth in exports driven by the readymade garments, similar growth in remittances, resilient growth in the agricultural sector, significant expansion of social protection programmes, wide coverage of the economic and social activities of the NGOs, developmental role of the central bank pushing inclusive and sustainable finance and, of course, a reasonable level of political stability. The strong and courageous leadership given by the Honorable Prime Minister from the front in reshaping the development journey of Bangladesh deserves to be recorded here, in particular. Under her strategic leadership, the recent increase in public investment for a number of mega projects including the Padma Bridge, Dhaka Metro Rail, Rooppur Atomic Energy Project, Matarbari coal-based electric plant, Karnafuli Tunnel, a number of special economic zones and IT parks have been providing new push for increased domestic and foreign investment in Bangladesh. Simultaneously some of the external factors have been quite favourable including greater market access in major export destinations, stable political relations with neighbouring countries (except, of course, Myanmar for creating a human disaster on the border by pushing out a million plus Rohiyanga population out of their homes in Rakhine), leading to some degree of regional cooperation, and weak financial linkage with the global economy (which cushioned Bangladesh from the last global financial crisis).

The outcomes of these favourable internal and external factors have been extremely rewarding indeed. Bangladesh was 50th top economy measured in PPP at constant 2011 US$ in 1990. By 2015, Bangladesh improved its position in this ranking to 31st. PWC projects that Bangladesh should become the 28th largest economy by 2030 and 23rd largest economy by 2050. Yet, HSBC, in its latest projection says Bangladesh may be the 26th largest economy by 2030.

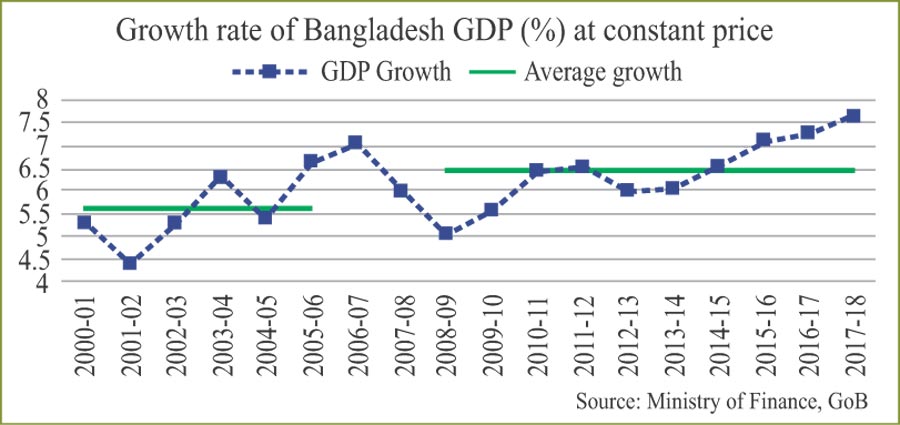

Despite all the past successes and optimistic future projections as indicated above, one may certainly raise the question how sustainable this forward march of Bangladesh can be. If past is a guide, the future of Bangladesh's development journey looks very promising indeed. Since the 1990s, Bangladesh economy has been growing consistently at an enhanced pace. The 1990s witnessed an average GDP growth rate of 5.6 per cent. The comparable growth rate for the last decade or so has been 6.3 per cent. The growth rate during last three years has been even more buoyant remaining above seven per cent and touching nearly 8.0 per cent (7.86%) in the fiscal year 2017-18. Over the last 27 years the economy of US$ 35 billion has jumped to US$ 270 billion. The figure may go up to US$ 285 billion plus even if the growth rate remains as it is. The per capita income increased nearly two and a half times over the last decade (from US$ 759 in 2008-9 to US$ 1751 in 2017-8). This has increased by more than five times since 1990s. The consistent growth in per capita income allowed Bangladesh to become a "lower-middle" income country in 2015. The growth cake has also been shared by all in Bangladesh. The stable inflation kept the real per capita income stable as well. This has been reflected in the three times growth in the consumption level of the people during the last decade.

The progress in poverty reduction, life expectancy at birth and other human development indicators speak a lot about the phenomenal progress in the domain of shared prosperity in Bangladesh. In particular, the poverty level has come down to about 22 per cent from 60 per cent in 1990s. The number of the poor too declined 63 million to less than 40 million over this period. The Human Development Index of Bangladesh has increased by 57 per cent since 1990 (from 0.387 to 0.6o6). In comparison, the Global HDI has increased by 21 per cent and that of Developing Countries by 32 per cent. On both counts the gains made by Bangladesh are simply impressive. The average life expectancy at birth in Bangladesh is now 73 years (as against 47 years in 1972). The same for India and South Asia is 69 years. The infant mortality rate per one thousand live birth for Bangladesh is 24 and that for children below five years is 34 years. These two figures for Developing Countries are 33 and 43 respectively. The maternal mortality rate for Bangladesh is 176 per one hundred thousand compared to 232 for Developing Countries. Bangladesh, however, need to do more on registration of births where it is significantly lagging behind the developing countries. We still have to cover many more miles in the areas of health and education where the per capita public expenditure remains pretty low. The literacy rate for girls is 94 per cent. And that for boys is 91 per cent. The per capita income growth rate for the last fiscal year was 6.2 per cent compared to 5.4 per cent for India. Ninety seven per cent of people in Bangladesh have access to safe drinking water compared to 86 per cent for the Developing Countries.

Thus, it can safely be said that Bangladesh outshines many other countries of comparable level of development in various indices of social development. Indeed, it has performed far better in the areas of social development compared to its economic growth performance. The success story of Bangladesh in Ready Made Garments export industry has made it a role model among its peers. The country's export increased from merely US$ 2.0 billion in 1990s to US$ 37 billion in 2017-18, an annual average export growth twice as high as the world average. The success of Bangladesh in diversification of its export basket far away from the primary commodities (less than 10 per cent) makes it a distinct story amongst LDCs.

Simultaneously, the contribution of this industry from virtually nothing to more than 80 per cent of total exports has made the story even more fascinating. The consistent growth of this sector has been a great source of indigenous growth generating massive employment opportunities, including four million plus new jobs in the RMG factories, mostly going to women coming from rural Bangladesh. Despite the challenge of diversifying the export sector, Bangladesh can surely be proud of significant economic transformation taking place over time. While agriculture accounted for 40 per cent of GDP in the mid-1990s declined to 15 per cent in 2017, the share of manufacturing doubled to 20 per cent during this period. In addition, the productivity of agriculture increased significantly due to mechanisation and strategic innovations in seeds and fertilizer use leading to tripling of the staple food, rice. The production of non-cereal food items also made quantum jump contributing towards improved food security.

The consistent growth in agriculture also helped reduce rural poverty and improve social development indices. The buoyant growth of the apparel industry contributed towards huge improvement in employment opportunities leading to income generation for the poor households and empowerment of women. The remittance flow increased from US$ 2.0 billion in 2000 to US$ 15 billion in 2016. This also helped improve standards of living of rural poor households in a significant way in addition to contributing towards maintaining stable balance of payment. The spurt in the growth of rural small and medium enterprises (SMEs) may be related to the greater flow of remittances which used to be mainly invested in building houses. The low-cost solutions to difficult social development challenges through NGO interventions have also been facilitating social mobilisation and enhancing population mobility.

The Challenges:

Despite the above eye-catching success story of Bangladesh in getting the UN's CDP nod to graduate out of the LDC status by the middle of the next decade some observers caution about the cost of this transition. Others, of course, find these challenges over-estimated. The former group are concerned about the loss of trade preferences which Bangladesh has been enjoying as an LDC. For example, about 60 per cent Bangladesh's exports go to European Union where duty-free access provides 6.0 to 12 per cent preferential tariff margin for LDC exporters over other exporters.

Also Bangladesh's exports to EU have been enjoying relaxed 'rules of origin' provisions. Other developed countries like Australia, Canada, Japan, the Republic of Korea, New Zealand and even developing countries like China and India also have been providing attractive preferential market access to LDCs.

UNCTAD estimates that if these trade preferences are fully withdrawn, this could cost as much as 7.0 per cent of Bangladesh's exports. There are also concerns that concessional external financing, particularly from international multi-lateral financial institutions like World Bank, Asian Development Bank (ADB) and Asian Infrastructure Investment Bank (AIIB), may be affected. Even bilateral development finance from JICA and DFID may become costlier for Bangladesh. However, the other group argues that the higher costs of graduation for Bangladesh may have been exaggerated. For example, this group says that Bangladesh never got any preferential market access from the US, the largest single destination of Bangladesh apparel exports. Yet, Bangladesh could enhance its total apparel exports to the US from US$ 2.4 billion to US$ 5.2 billion. Similarly, concessionary external finance has never been a binding constraint for Bangladesh.

The problem lies elsewhere. Due to lack of its implementation capacity, Bangladesh lagged behind in utilising the committed loans and grants resulting in the build-up of unutilised pipeline of the same of close to US$ 36 billion. The annual disbursement of it hovers around US$ 2 to 3 billion for Bangladesh. This indicates the weak absorption capacity of Bangladesh originating mainly from its complex rules and procedures including poor regulatory institutional quality, political instability and as well as lack of skilled implementers of projects. All these have also been constraining the flow of foreign direct investment (FDI) to Bangladesh.

The Way Forward: Notwithstanding the above challenges, Bangladesh is poised to make the graduation to a developing country well ahead of the deadline. The roadmap has been laid down and it is time to move on steadfastly. The present government has been able to focus exclusively on infrastructure development including a number of mega projects, in particular its courageous move to develop one hundred Special Economic Zones both in the public and private sectors, could indeed turn out to be a game changer for enhancing investment to maintain a high level economic growth rate.

In addition, the government has come out of the short-termism and is moving ahead with long-term perspective plans including farsighted Delta-Plan spanning over next eight decades. The success of Bangladesh in achieving strong and consistent economic growth and social development indicators provides enough hope of its desired transformation into a developing one and then a developed country. As already indicated by PWC and HSBC projections, we should, certainly, be proud of this 'booming Bangladesh' (reference: Kaushik Basu, Project Syndicate,1 May 2018) story. Yet, to make this story sustainable we must remain focused on the challenges normally faced by a middle income country and take necessary preparations to overcome the same.

Therefore, Bangladesh should continue to work hard to further consolidate its initial gains (which look almost similar to most East Asian countries) in the strategic development policy arenas like better economic management, higher investment in infrastructure (along with ensuring energy security, if possible, more of renewable energy) and human development (including higher skill development), continued greater participation of females in education and smart work places, taking further advantage of labour-intensive export-oriented industry (enhancing export volume faster), improved institutional base for faster easing of doing business, greater technological readiness (as the future business will be essentially digital and e-commerce-based), remaining on track in implementing sustainable development goals (SDGs) (like its success in the case of MDGS), further mechanisation of agriculture, smart urbanisation, making ICT the new 'RMG sector, taking advantage of Bangladesh's strategic regional position as a centre-point of the 'dynamic growth triangle' made by China, South East Asia and India, continued larger space to the private sector including SMEs, improving significantly Revenue- GDP ratio and finally making the buoyant growth process more adaptive to climate change.

Given its past record of spectacular socio-economic progress despite so many challenges, its transition to the status of a developing country and finally to a developed country by 2041 will certainly be noted as a 'development surprise' by the keen development watchers.

Dr. Atiur Rahman is a noted economist and a former Governor

of Bangladesh Bank. dratiur@gmail.com