Power sector: Looming challenges

Md. Sakib Chowdhury | Tuesday, 11 December 2018

![]() Bangladesh's power generation capacity increased from 5,201 MW in June 2008 to 20,133 MW in September 2018 and electricity consumption saw a staggering average annual growth rate of 9.0 per cent over the last decade. Eventually, access to electricity for the country increased from 48.4 per cent in 2010 to 80.0 per cent in 2017. Also, maximum load shedding, according to Bangladesh Power Development, has declined from 1,049 MW in FY'08 to 250 MW in FY'17. Moreover, transmission and distribution system loss was significantly reduced over the period. Such an outstanding development in the power sector is one of the key drivers of the country's impressive economic growth of above 6.0 per cent on an average per year over the last decade.

Bangladesh's power generation capacity increased from 5,201 MW in June 2008 to 20,133 MW in September 2018 and electricity consumption saw a staggering average annual growth rate of 9.0 per cent over the last decade. Eventually, access to electricity for the country increased from 48.4 per cent in 2010 to 80.0 per cent in 2017. Also, maximum load shedding, according to Bangladesh Power Development, has declined from 1,049 MW in FY'08 to 250 MW in FY'17. Moreover, transmission and distribution system loss was significantly reduced over the period. Such an outstanding development in the power sector is one of the key drivers of the country's impressive economic growth of above 6.0 per cent on an average per year over the last decade.

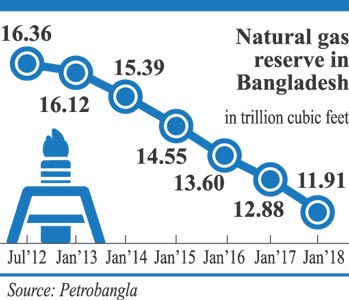

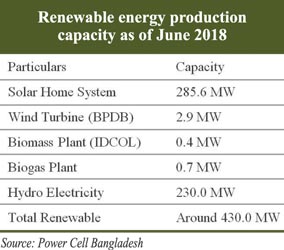

Over the last two decades, on an average, 77 per cent of total electricity supplied to the national grid of Bangladesh was produced from natural gas. Large and young population (median age of around 24 years only), growing urban population and potential for further industrialisation represent significant growth potential for the power sector. As the demand for Bangladesh's power keeps increasing, the primary fuel for electricity generation, natural gas, given its depleting reserve, is fast becoming insufficient to meet its growing demand. To overcome the crisis, the country came up with the Power System Master Plan (PSMP) in 2010 with a roadmap for meet its energy demands by 2030. The master plan rightly identified the depleting gas reserve of the country and envisaged generating around 50 per cent of the country's electricity from coal, 25 per cent from gas, 10 per cent from nuclear-based power plants, 10 per cent from renewables, and the rest from other resources. But things did not go according to the plan. The coal-based power plants particularly saw very little progress. Moreover, at present, renewables contribute only about 1.7 per cent of total electricity generation, the bulk of which comes from hydroelectricity and solar. At Kaptai in the South-east region of Bangladesh, the country has a hydroelectric plant with 230.0 MW generation capacity. The plant at Kaptai has a potential for extending capacity by 100 MW by utilising spill water. Apart from the site in Kaptai, Bangladesh has two more possible sites for constructing two medium-size hydro plants across the Sangu and Matamuhuri rivers in the same region. As the terrain of the country is flat, there is no realist prospect for building additional hydro units. Moreover, in Bangladesh, 60 per cent of the available land is used for food production, 20 per cent for various infrastructure including industries and 1-2 per cent for habitation. With land being short in supply, it is difficult to see commercial solar power generation becoming a significant contributor to the national electricity consumption. Thus, the target to product 10 per cent of the total electricity generated through renewables seems a little ambitions. And we may have to remain satisfied with small-scale household power generation using PV cells.

To overcome the crisis, the country came up with the Power System Master Plan (PSMP) in 2010 with a roadmap for meet its energy demands by 2030. The master plan rightly identified the depleting gas reserve of the country and envisaged generating around 50 per cent of the country's electricity from coal, 25 per cent from gas, 10 per cent from nuclear-based power plants, 10 per cent from renewables, and the rest from other resources. But things did not go according to the plan. The coal-based power plants particularly saw very little progress. Moreover, at present, renewables contribute only about 1.7 per cent of total electricity generation, the bulk of which comes from hydroelectricity and solar. At Kaptai in the South-east region of Bangladesh, the country has a hydroelectric plant with 230.0 MW generation capacity. The plant at Kaptai has a potential for extending capacity by 100 MW by utilising spill water. Apart from the site in Kaptai, Bangladesh has two more possible sites for constructing two medium-size hydro plants across the Sangu and Matamuhuri rivers in the same region. As the terrain of the country is flat, there is no realist prospect for building additional hydro units. Moreover, in Bangladesh, 60 per cent of the available land is used for food production, 20 per cent for various infrastructure including industries and 1-2 per cent for habitation. With land being short in supply, it is difficult to see commercial solar power generation becoming a significant contributor to the national electricity consumption. Thus, the target to product 10 per cent of the total electricity generated through renewables seems a little ambitions. And we may have to remain satisfied with small-scale household power generation using PV cells.

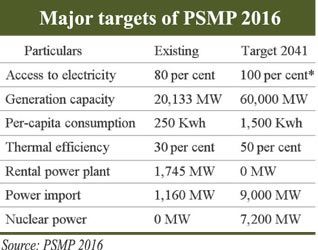

Under such circumstances, the PSMP 2016 was unveiled. According to the revised master plan, Bangladesh by 2041 envisions reaching a power generation capacity of 60,000 MW, taking the per capita electricity generation to 1,500 Kwh from existing 250 Kwh, increasing thermal efficiency to 50 per cent form 30 per cent while completely getting out of rental power plant model to reduce power generation cost. Unlike PSMP 2010, PSMP 2016 did not give any definite target mix of fuel for power generation. Rather, the latest master plan presented five scenarios of the energy mix for power generation. In all scenarios, the PSMP 2016 outlines high dependence on imported primary energy (LNG, coal, and oil), given the limited reserves of domestic natural gas and coal. The master plan also addresses that such over-reliance on imported energy

According to the revised master plan, Bangladesh by 2041 envisions reaching a power generation capacity of 60,000 MW, taking the per capita electricity generation to 1,500 Kwh from existing 250 Kwh, increasing thermal efficiency to 50 per cent form 30 per cent while completely getting out of rental power plant model to reduce power generation cost. Unlike PSMP 2010, PSMP 2016 did not give any definite target mix of fuel for power generation. Rather, the latest master plan presented five scenarios of the energy mix for power generation. In all scenarios, the PSMP 2016 outlines high dependence on imported primary energy (LNG, coal, and oil), given the limited reserves of domestic natural gas and coal. The master plan also addresses that such over-reliance on imported energy  (particularly LNG) will significantly increase power generation cost. Accordingly, PSMP 2016 plans to gradually increase electricity to eliminate the gap between production cost and selling price. The PSMP 2016 also suggests gradually increasing gas price to get rid of the subsidy given to Petrobangla.

(particularly LNG) will significantly increase power generation cost. Accordingly, PSMP 2016 plans to gradually increase electricity to eliminate the gap between production cost and selling price. The PSMP 2016 also suggests gradually increasing gas price to get rid of the subsidy given to Petrobangla.

Overall, the revised master plan is more realistic compared to PSMP 2016 in addressing and solving upcoming problems in primary energy and power generation arena. However, there are some challenges/risks in implementing the master plan 2016 -

Ambitious targets: The PSMP 2016 targets for 2021 will probably be met, but the 2041 targets are ambitious and are unlikely to be met. Specifically, we think that extraction of 2,000 mmcfd domestic gas and 11.0 million MT/year of domestic coal by 2041 is highly ambitious. Notably, concerns related to method, technology, and social consequences still remain as the major obstacles to coal mining in Bangladesh. Moreover, the PSMP presented three cases to project electricity peak demand. The average GDP growth rates until 2041 for the cases are high case with 6.4 per cent, base case with 6.1 per cent and low case with 5.9 per cent. And the growth rates of peak demand for each case are 7.0 per cent per year in high case, 6.7 per cent per year in base case and 6.3 per cent per year in low case. We think the country will have to show remarkable economic progress to be able to have such a high level of electricity demand.

Over-reliance on import: The PSMP 2016 will create more than 90 per cent import dependency of fuel for electricity by 2041. Since most of the energy will be imported, the impact on the tariffs of natural gas and electricity must be carefully managed.

Inadequate infrastructure support: The country has not yet started developing the infrastructure - ports to facilitate mass import of coal, railway and inland waterway communication to carry the coal to the power plants or a coal extraction policy to exploit the local coal, which is essential for the successful implementation of the master plan. Moreover, the country will have to establish LNG re-gasification facilities on time to reach the power generation targets; any delay in LNG projects would lead to more dependency on oil.

The delay in project implementation: Historically, projects do not get implemented on time in Bangladesh. As mentioned earlier, none of the coal-based power projects was going according to plan. Even after almost three years of publishing the PSMP 2016, the coal-based power plants have seen very little progress. Notably, different Chinese companies have committed to investing more than USD 12.0 billion in coal-based power projects in the past few years; however, only half of them have seen some progress.

Pressure on exchange rate: The last important aspect of all these huge expenditures for the energy and electricity infrastructure is the pressure on the foreign exchange rate and debt servicing.

.................................................................

Md. Sakib Chowdhury, Research Analyst, BRAC EPL Stock Brokerage Ltd. sakib17du@gmail.com