Role of financial inclusion in women’s empowerment, economic development

Md. Anwarul Islam, Direndra Chandra Das and Bidhan Chandra Shahan | Sunday, 25 November 2018

![]() Financial inclusion aims at including the unbanked and unserved population under the financial services network. Financial inclusion initiatives try to ensure that all adult population, irrespective of income level, have right to effectively use the financial services that are suitable to them and by using those services they can improve their lifestyle. Financial inclusion targets address both financial and social objectives of a country. The ultimate target of financial inclusion is economic development through inclusive growth and financial deepening. Financially excluded population are those who generally do not have much money, but still they have to save, borrow and manage money for their livelihood. Without access to formal financial services, they have to rely on informal source of money. This might include moneylenders, family and friends, brokers, pawn-traders etc. which are expensive, uncertain and risky.

Financial inclusion aims at including the unbanked and unserved population under the financial services network. Financial inclusion initiatives try to ensure that all adult population, irrespective of income level, have right to effectively use the financial services that are suitable to them and by using those services they can improve their lifestyle. Financial inclusion targets address both financial and social objectives of a country. The ultimate target of financial inclusion is economic development through inclusive growth and financial deepening. Financially excluded population are those who generally do not have much money, but still they have to save, borrow and manage money for their livelihood. Without access to formal financial services, they have to rely on informal source of money. This might include moneylenders, family and friends, brokers, pawn-traders etc. which are expensive, uncertain and risky.

The pursuit of financial inclusion targeted at bringing the 'unbanked' population into the formal financial services platform and allowing them to use these services which are profitable for both the service receivers and providers. There is a realisation that absence of proper access to financial system badly affects the economic development and poverty reduction, as the poor find it difficult to accumulate savings, make assets to protect themselves against risks as well as invest their savings in income-generating schemes. Financial inclusion targets to enhance the access of poor people to the financial services which in turn gives them more money and brings speed to their money as well. It helps reduction of poverty first and then lowers the income inequality. The empirical evidence shows that higher financial inclusion reduces income inequality (Park and Mercado, 2018).

The Bangladesh Bank, the central bank of Bangladesh, is the apex financial regulator of the country being empowered vide the President's Order No 172 of 1974 exercises the specific mandate for financial inclusion and financial literacy. After the independence of the country, the inclusion activities focusing the agro-based financing were started through the nationalised commercial banks. In the year 1972, government allowed the non-governmental organisations (NGOs) to run the microfinance operation along with the aid operation in the rural areas of Bangladesh. The Bangladesh Rural Advancement Committee (BRAC), the world's largest NGO, was established and it started limited scale microfinance operation in the selected areas. In 1973 a specialised bank named Bangladesh Krishi Bank was set up to bring in more agricultural farmers under the banking system and the bank's branch network was extended to almost every union (the second last rural administrative level) in Bangladesh. A decade later, the Bangladesh Bank started licensing commercial banks to extend the financial network so that more people can have access to the formal financial system. The Grameen Bank introduced an innovative, group-based collateral-free lending model with a view to ensuring low-cost and easy access to finance for the poor in 1983. With the passage of time, the Bangladesh Bank and the government of Bangladesh started allowing more players in the financial service industry to boost-up the efforts towards greater financial inclusion.

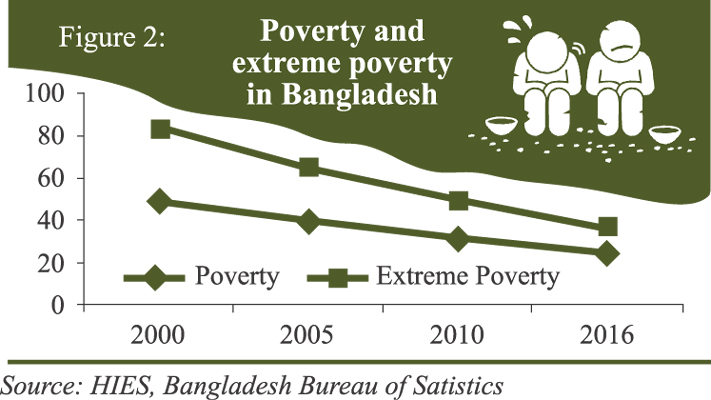

Bangladesh has been experiencing a GDP growth rate over 6.0% in the last decade and the poverty rate has also been significantly declining. During this period, the number of bank branches and their network has also notably increased.

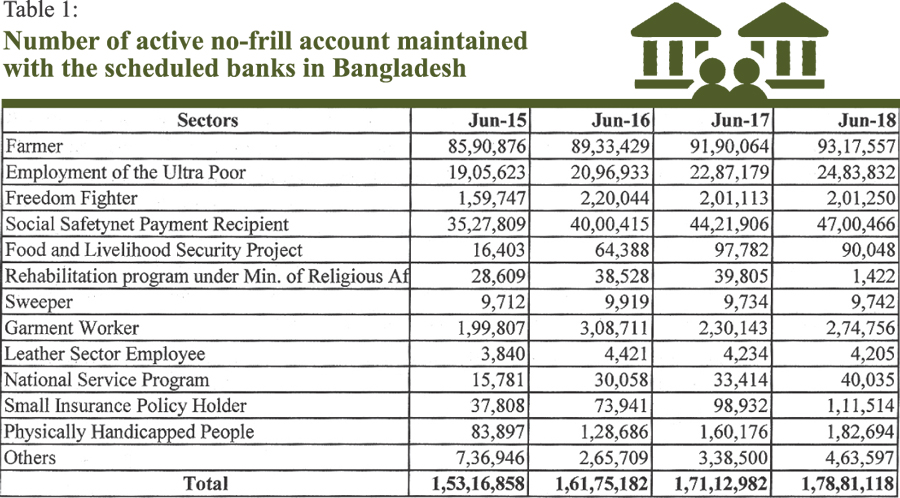

A lot of financial services including mobile banking services have been introduced and captured significant market share in Bangladesh. The government of Bangladesh (GoB) has also launched many social safety net programs, such as Allowances for the Widowed, Deserted and Destitute Women, Food for Work, Stipend and Access Increase for Secondary and Higher Secondary Level, Honorarium for Insolvent Freedom Fighters and Allowance for the Financially Insolvent Disabled, which allowed the extremely poor people to get on board of financial services. Some of those programs are specially designed for the women. These initiatives play a significant role in reducing poverty from the society. The Bangladesh Bank issued several instructions for banks to open special types of accounts called No-Frilled Accounts (NFA) for the marginal segment of people in society. NFAs are being maintained with the scheduled banks and thus banking services are provided to the under-privileged people. Banks are also instructed not to realise any fees and charges from those accounts. In addition, banks are to offer special interest rates against the balances kept in those NFAs. As of June 2018, about 18 million active NFAs are maintained with the scheduled banks in Bangladesh.

The Bangladesh Bank issued several instructions for banks to open special types of accounts called No-Frilled Accounts (NFA) for the marginal segment of people in society. NFAs are being maintained with the scheduled banks and thus banking services are provided to the under-privileged people. Banks are also instructed not to realise any fees and charges from those accounts. In addition, banks are to offer special interest rates against the balances kept in those NFAs. As of June 2018, about 18 million active NFAs are maintained with the scheduled banks in Bangladesh.

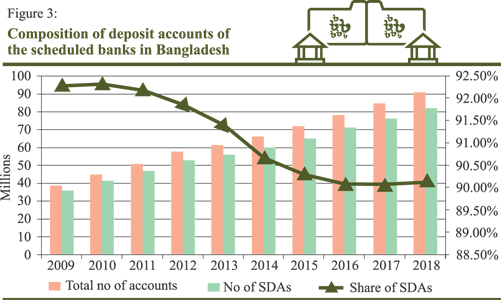

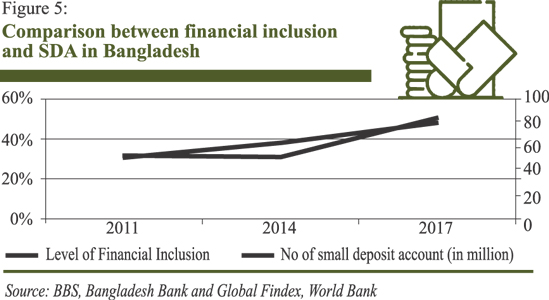

All of these initiatives have increased the level of financial inclusion of the country as well as the number of small deposit account for the banks. The number of small deposit accounts has more than doubled since 2009 (Bangladesh Bank). On the contrary, the share of small deposit accounts has decreased over time with the incremental rise in the number of total accounts. This is an indication that the number of accounts with more account balance has increased over time. This also denotes the growth in the income level and economic condition of the people of Bangladesh. Despite those efforts from the government's side and the Central Bank, targeting the same audience, almost half of the population in Bangladesh remains unbanked. According to the Global Findex (2017), 170 million working-age adults globally are out of formal financial network. Almost half of the world's unbanked population belongs to the seven countries including Bangladesh. There is an estimation that around three per cent of those unbanked population live in Bangladesh. The gender gap is also wider than the global average in Bangladesh. Women need full and equal participation and empowerment in all areas to achieve Sustainable Development Goals by 2030 (United Nations).

Despite those efforts from the government's side and the Central Bank, targeting the same audience, almost half of the population in Bangladesh remains unbanked. According to the Global Findex (2017), 170 million working-age adults globally are out of formal financial network. Almost half of the world's unbanked population belongs to the seven countries including Bangladesh. There is an estimation that around three per cent of those unbanked population live in Bangladesh. The gender gap is also wider than the global average in Bangladesh. Women need full and equal participation and empowerment in all areas to achieve Sustainable Development Goals by 2030 (United Nations). Empowerment is the process of becoming stronger and more confident, which is not possible without the control of financial assets. Having access to financial service and ownership to financial assets people feel themselves empowered. Women have less access and right to financial assets and so as in the decision making process in a family. Generally, the status of woman empowerment in Bangladesh is not equal to that of men. Most of Bangladeshi women are still dependent on their husbands and one in every three married women has no control over their household spending (United Nations, 2015). About ten per cent women are not consulted the way of their own earnings spent (United Nations, 2015).

Empowerment is the process of becoming stronger and more confident, which is not possible without the control of financial assets. Having access to financial service and ownership to financial assets people feel themselves empowered. Women have less access and right to financial assets and so as in the decision making process in a family. Generally, the status of woman empowerment in Bangladesh is not equal to that of men. Most of Bangladeshi women are still dependent on their husbands and one in every three married women has no control over their household spending (United Nations, 2015). About ten per cent women are not consulted the way of their own earnings spent (United Nations, 2015).

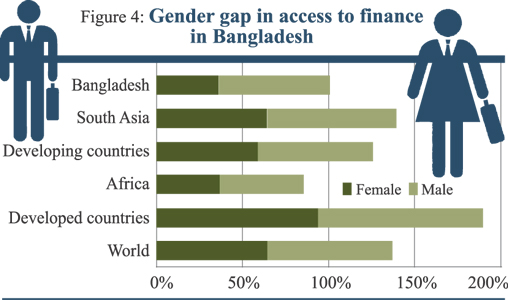

Garment industries are booming in Bangladesh and their contributions accounts for more than 80 per cent of Bangladesh's total exports. 85 per cent of the total garments workers of Bangladesh are women (The World Bank, 2018). They are playing an important role by supporting their family with their earnings and so in advancing rural economy. Despite those important advances, the access of women to the formal financial services in the recent years in Bangladesh shows a significant gap. This gender gap is nearly 30 per cent between men and women in Bangladesh, whereas the gap is around 7.0 per cent globally (The Global Findex, 2017).

To address these shortcomings and to implement sustainable financial inclusion strategies, Bangladesh Bank has taken many initiatives. A new era of financial inclusion journey was started after joining to the Alliance for Financial Inclusion (AFI) network. AR is a global alliance for financial inclusion which empowers policymakers around the world to increase access to quality financial services for the poorest populations. Bangladesh Bank has also made several commitments regarding financial inclusion in the Maya Declaration. The public commitments made and reviewed in the Maya Declaration created an inherent pressure to the financial regulators and the respective government to act vigilantly for increasing total banked population, reducing gender gap and setting clear strategies regarding financial inclusion. The visible progress of this pressure is a set of strategies which will drive country's financial inclusion journey further. The progress of this effort is the comprehensive and country's first ever National Financial Inclusion Strategy (NFIS) which is being formulated through a wider consultative approach from all the relevant stakeholders. Empirical studies concluded that policy measures taken by the regulators to increase financial inclusion would have the side-benefit of contributing to financial stability as well (Morgan, 2014).

After the recent global financial crisis, the need for financial stability is largely realised by the policymakers around the world. Though there is a limited work which established the specific linkage between financial stability and financial inclusion. Financial instability in the market started increasing the panic among people about their savings with banks and they started rushing towards the bank's counter for withdrawal of their money. The small deposit holders are believed to be less informed about the instant market situation and they are the last group that generally rush to the banks for their money in case of a crisis. Though few, but empirical studies support this statement. An important work done by Han and Melecky (2013) who analysed 95 country's data to established an association between decline in deposit growth and access to deposit for a period of 4 years starting from 2007. They uncover that country where there is a greater financial inclusion, the lesser the trend of fall in deposit growth.

Financial stability can play an important role towards national economic growth. For banks, stable deposits not only enhance the loanable funds but also generate more income and reduce the operating costs. Thus the small deposits can help boost the level of resilience of banking system. When the other source of funds become scare for banks, these small deposit holders continue the cash inflow of the bank and help the bank to continue lending operation. In absence of such deposits, it would be tough for banks to continue credit business. This credit channel has the prospect to intensify the impact of the crisis on the local economy more than would otherwise be the case.

The literatures that evident a relation between small-scaled deposit and loan account with the financial inclusion in Bangladesh is scarce. This paper assesses the empirical evidence of financial inclusion taking into consideration of small bank deposits and small loan accounts using data from the Scheduled Bank Statistics report of Bangladesh Bank over the period 2009-2018.

Financial inclusion and small bank deposit in Bangladesh

The expansion of bank branch network and the evolution of microfinance significantly reduced financial exclusion, poverty and income inequality in Bangladesh. But the Global Findex 2017 shows a large segment of population is still deprived of the basic financial services in Bangladesh. Despite the expansion of branch network, banks have been unable to reach the underprivileged population (Pierce, 2011). As such situation, the duty of the regulators is to create an enabling environment for financial inclusion. Regulators should come up with the favourable policies that welcome innovative technologies to reduce transaction costs and bring speed to the delivery channels. Efficient and convenient financial system can easily accommodate the broader section of the population.

The higher income economies are experiencing a lower poverty rate and there exists a higher rate of financial inclusion and the adverse situation is prevailed in the middle-income and lower-income economies (Park and Marcado, 2018). Similar studies have found a strong association between financial access to banking services and economic development and growth. The higher income allows people to get them banked and thus their income can be further increased and thus creates a virtuous circle of income generation. Empirical evidence shows that countries with higher number of bank branches and deposits have higher level of income and financial inclusion. Those studies demonstrate a positive correlation between financial inclusion and per capita GDP. Some studies have also found the relationship between financial inclusion and income inequality is still not established (Dhrifi, 2013).

Financial inclusion activities persuade small deposit holders to anchor their deposits to financial institutions which improve the process of intermediation between savings and investments. This helps banks to widen their customer base and diversify their balance sheet. Risk diversification approach makes banks more resilient to defy unexpected losses, Financial inclusion involves wider segments of the society into its financial system which also helps policy makers in formulating various policies accurately. Financial excluded populations rely greatly on cash transactions and their monetary decisions do not necessarily reflect in the national policies. So the gap persists between financially excluded and included population which in turn promotes financial instability in the economy. Financial inclusion is one of the powerful tools to reduce the gap between rich and poor by providing opportunities of getting easy and low cost credit to the poor.

Does financial inclusion have any correlation with small deposit account in Bangladesh? In answering this question, past studies shows contradictory results. While studying cross-country data on 95 countries to determine the relationship between a measure of access to deposits and the maximum decline in deposit growth in 2007-2010, Han and Melecky (2013) find higher access tends to lead to a smaller drop in deposit growth. In another study, Morgan and Pontines (2014) construct two indicators of bank risk, the "bank z-score" and non-performing loans using the country-level panel data from the World Bank and IMF for 2005-2011. They show that a greater share of lending to small firms tends to reduce both indicators of bank risk. In contrast, Dante B. Canlas, J. N. E., Ravalo & Eli, M. R., (2018) investigate the behaviour of deposits of different account sizes around three significant bank closures in the Philippines. They find no difference between large and small deposit while analysing the contagion effect in case of bank failure and thus, conclude financial inclusion is unlikely to be correlated with financial instability. Hence, the relationship among financial inclusion, small bank deposit and financial stability varies from country to country.

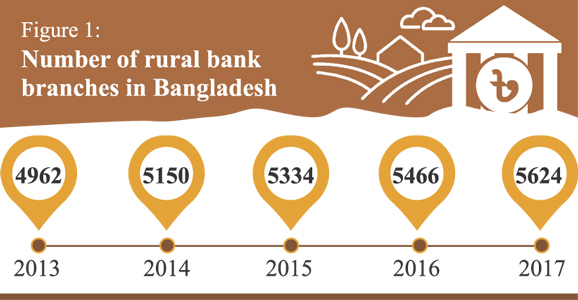

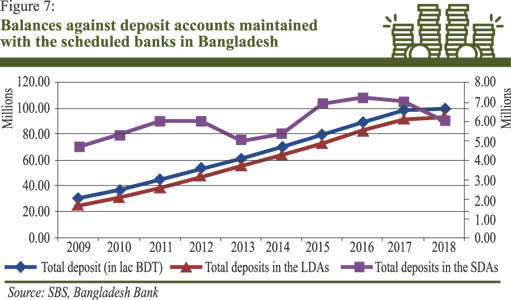

To investigate the correlation, we analyse the deposit account data of Schedule Bank Statistics (SBS) report of Bangladesh Bank. Since there is no nationwide financial survey or baseline survey exists in Bangladesh, we look at Bangladesh Bank's data to observe the impact of financial inclusion initiatives. It may be mentioned that the Micro Finance Institutions (MFIs) represent a large portion of small deposit account holders in Bangladesh. However, SBS data only represents the information for the Scheduled Banks in Bangladesh. There are 57 commercial banks operating in Bangladesh with 9,955 branches where 5,624 branches are located in rural areas and 4331 branches are in urban areas (Bangladesh Bank, 2017). In 2009 total number of deposit account was 38.05 million out of which number of small deposit account (SDA) was 35.12 million which is 92.29% of total deposit account. After almost a decade in 2018, the number of deposit accounts has more than doubled and now stands at 90.23 million. Number of SDA also shows the similar trend and reaches at 81.33 million in 2018. However, number of large deposit accounts (LDAs) increase three times from only 2.93 million to 8.91 million during the same period, which indicates the economic prosperity of the country.

We assume the deposits in the smallest size cohort to be associated with financial inclusion, and we compare their behaviour to that of larger deposits. We compare the behaviour of the small deposit account with the financial inclusion level of the country as shown in the Global Findex database of the World Bank.

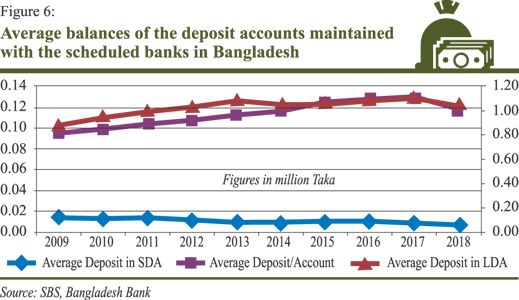

We also study the average balances of the deposit accounts maintained with the scheduled banks in Bangladesh from the period 2009 to 2018. We find a decreasing trend in the balances against the small deposit accounts while we observe the opposite pattern for the total deposit account and the large deposit account. Though the result is not conclusive, we might say that the small deposit accounts are less volatile than other deposits.

We also analyse the trend of deposit accounts balances from two different perspectives and find a different pattern. Since the number of large deposit account has trebled and the income gap persists in Bangladesh, we observe a continuous rise in the case of large accounts while a moderate fluctuation against the small deposit accounts.

Woman empowerment and financial inclusion:

Financial inclusion is strongly positively related with the citizen empowerment. Access to credit has a positive link between economic opportunities and outcome. Hence, empowering mass population to utilise economic opportunities, financial inclusion can be a powerful tool for sustainable and inclusive growth. This is how equal participation of women, half of the total population, is crucial for equitable development. Ensuring sustainable financial inclusion will require supply-side and demand-side challenges to be addressed simultaneously through systemic solutions. All stakeholders of the financial inclusion ecosystem, including financial institutions, regulatory agencies, technology service-providers and civil society organisations, will need to play their parts effectively.

Increasing women's financial inclusion is especially important as women disproportionately experience poverty, stemming from unequal divisions of labour and a lack of control over economic resources. Many women remain dependent on their husbands, and about one in three married women from developing countries has no control over household spending on major purchases (United Nations, 2015). About one in 10 are not consulted about the way their own earnings are spent (United Nations, 2015). In addition, women often have more limited opportunities for educational attainment, employment outside of the household, asset and land ownership, the inheritance of assets, and control over their financial futures in general. Despite important advances in expanding access to formal financial services in the developing world in recent years, a significant access gap remains between men and women. This is illustrated through a basic measure of financial inclusion: account ownership. Globally, only 58 per cent of women hold an account in a formal financial institution, compared to 65 per cent of men (Demirguc-Kunt et al., 2015). This gender gap is even more pronounced between men and women in developing markets,

Financial services are a core enabler for consumption smoothing, risk mitigation, self-employment, SME growth, asset accumulation, and wealth creation. Lack of access to financial services reduces women's ability to climb out of poverty; increases their risk of falling into poverty; contributes to women's marginalisation to the informal sector; and reduces their ability to fully engage in measurable and productive economic activities.

Forty-two per cent of women and girls worldwide - approximately 1.1 billion - remain outside the formal financial system, according to the Global Findex, 2017. Despite recent progress in financial inclusion rates in general, the gender gap has not narrowed: While account penetration increased by 13 percentage points among men and women between 2011 and 2014, the gender gap remains a steady 7.0 percentage points. Among adults living in the poorest 40 per cent of households in developing economies, the gender gap is 11 percentage points. The gap varies significant by region and is highest in South Asia.

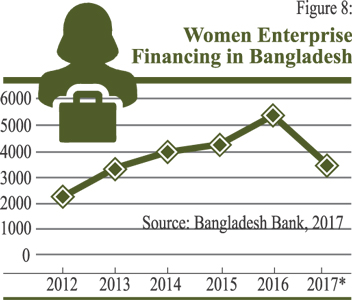

Bangladesh has long been a success story for women's financial inclusion, where 90% of the 21 million clients served by MFIs are women. And in terms of access to formal financial services, 35% per cent of women in Bangladesh hold a bank account, which is above the regional average for South Asia (Global Findex, 2017). But in terms of digital finance, the story is very different. Despite being identified as a "mobile money sprinter" by the GSMA, only 18% of digital finance users in Bangladesh are women, with even fewer holding registered accounts. This is perplexing, given the rapid growth of digital financial services now reaching more than 21 million registered account holders. Finally, despite the progress made in advancing financial inclusion globally, women remain disproportionately excluded from the formal financial system. According to the Global Findex Database (2017), more than one billion women are still excluded with a 7.0 percentage point gender gap in access to financial services globally. Inadequate financial infrastructure, such as a lack of interoperable digital payment platforms, credit bureaus and collateral registries, can restrict women's financial inclusion. Moreover, in Islamic countries, women are usually excluded from the economic activities due to religious reasons. Greater focus on the value proposition of women's financial inclusion, with explicit policy objectives and quantitative targets, can lead to transparent and inclusive policies for women. Digital platform could be one solution instead of traditional and costly women only concept. However, it is also true that women are less likely to use technology than their male counterpart and hence, significant importance should be given on financial literacy of women.

Finally, despite the progress made in advancing financial inclusion globally, women remain disproportionately excluded from the formal financial system. According to the Global Findex Database (2017), more than one billion women are still excluded with a 7.0 percentage point gender gap in access to financial services globally. Inadequate financial infrastructure, such as a lack of interoperable digital payment platforms, credit bureaus and collateral registries, can restrict women's financial inclusion. Moreover, in Islamic countries, women are usually excluded from the economic activities due to religious reasons. Greater focus on the value proposition of women's financial inclusion, with explicit policy objectives and quantitative targets, can lead to transparent and inclusive policies for women. Digital platform could be one solution instead of traditional and costly women only concept. However, it is also true that women are less likely to use technology than their male counterpart and hence, significant importance should be given on financial literacy of women.

Financial stability and financial inclusion

A well number of empirical research argue that an inclusive financial sector confirms more diversified, resilient bank balance sheet including a stable retail deposit base, which ultimately ensures the macro-prudential financial stability (Cull, Robert, Ash D. K. & Lyman T., 2012; Prasad, 2010). In contrast, some economists pointed out that excessive financial inclusion promotes financial instability if it is unregulated (Rajan, G.R., 2010).

The relationship of financial inclusion and inclusive growth has already been established by well number of researches (Swamy, 2012; Zwedu, 2014; Migap, Okwanya, and Ojeka, 2015). One of such researches on Nigerian economy conducted by Migap et. al. (2015) concluded that the financial inclusiveness has significant impact on African inclusive economic growth. However, research on the relationship between financial inclusion and financial stability is just beginning (AFI, 2013; Cehak, Mare, and Melecky, 2016; Morgan & Pontines, 2014). The studies have pointed some direct and indirect linkage between financial inclusion and financial stability. They have argued that financial inclusion promotes a more diversified funding base, it diminishes the appeal of potentially unstable savings channels, and finally it promotes an inclusive financial sector with greater political legitimacy. Moreover, financial inclusion promotes financial stability at the household level and it promotes greater income equality, thereby fostering financial stability. In contrast, some studies argue that there is a trade-off between financial inclusion and financial stability. For example, Rajan (2010) opines that unregulated expansion of financial inclusion can lead to financial instability. Therefore, it is the time to analyse the relationship between financial inclusion and financial stability.

Financial stability:

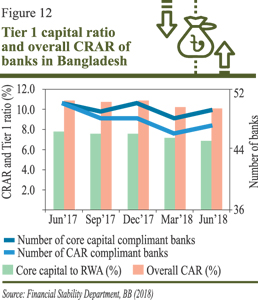

ECB Financial Stability Review (2012) defines financial stability as "A condition in which the financial system - comprising of financial intermediaries, markets and market infrastructure - is capable of withstanding shocks and the unravelling of financial imbalances, thereby mitigating the likelihood of disruptions in the financial intermediation process which are severe enough to significantly impair the allocation of savings to profitable investment opportunities." Like any other developing countries, financial stability has got high priority in Bangladesh after global financial crisis. Bangladesh Bank has taken various policy measures to ensure financial stability in Bangladesh including creating of a new department call Financial Stability Department in Bangladesh Bank. Due to the initiatives taken by the central bank, Bangladesh has achieved Ba3 (Moody's) and BB-(Standard and Poor's) country rating with stable economic outlook consecutively for six times. This stable outlook of Bangladesh economy is mostly attributed to the innovative and inclusive policies taken by its central bank (Rahman, 2013). By analysing Bangladesh economy some notable achievements can be listed as below:

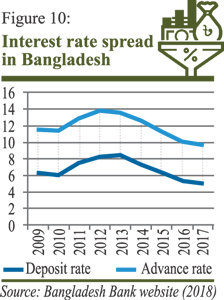

* The interest rate spread has remained at a stable level at near about 5% since 2017;

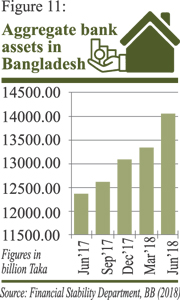

* The balance sheet size that includes loans and advances to total assets and the share of investment has been growing significantly during last couple of years;

* Asset quality, measured by non-performing loans (NPL) to the aggregate loan portfolio, and NPL to regulatory capital improved significantly over the preceding quarter;

* Key profitability indicators, i.e., Return on Assets (ROA) and Return on Equity (ROE) has been increasing moderately;

* It is in the second position in terms of foreign exchange reserve (USD 32.4b, 2018) after just India in South Asia;

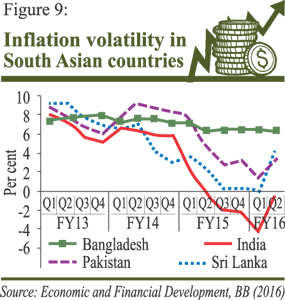

* Inflation volatility of Bangladesh is lowest among South Asian countries and GDP growth rate shows steady upward trend during last decade, which reaches at 7.68% in 2017; and

* Minimum regulatory capital to risk weighted asset ratios (CRAR) of the most of the banks is above 10.0 per cent which is in line with Pillar I of the Basel III capital framework.

Relationship between financial inclusion and financial stability

Both the financial inclusion and financial stability got their priority after the global financial crisis and these two have been implanting by the major central banks simultaneously overlooking the linkage between them. Researchers found both positive and negative linkage between financial inclusion and financial stability.

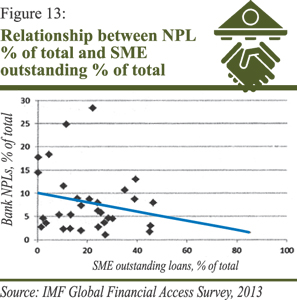

Greater financial inclusion extends the asset portfolio base of a bank. Diversification of loan portfolio can reduce the risk of bank default and can improve the quality of the balance sheet. A survey conducted by IMF (2013) shows that there exists a negative relationship between the non-performing loan and outstanding of SME finance-a proxy of access to credit.

Greater financial inclusion extends the asset portfolio base of a bank. Diversification of loan portfolio can reduce the risk of bank default and can improve the quality of the balance sheet. A survey conducted by IMF (2013) shows that there exists a negative relationship between the non-performing loan and outstanding of SME finance-a proxy of access to credit.

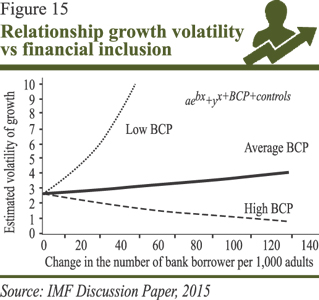

Moreover, highly concentrated loan portfolio can also impose a great threat towards financial instability. In contrast, some researchers argue that a broader base of loans and advances can also related to higher volatility. However, this increase in growth volatility can be suppressed by close supervision and better regulation.

Financial inclusion can ensure better monetary transmission by facilitating greater participation by different segments of the economy in the formal financial system. If a large portion of the population are excluded from the formal financial system, their behaviour would be unaffected by the monetary policy action of the central bank, which can weaken the transmission channel.

A more inclusive financial sector governance structure can also be important for financial stability. Financial access to larger population can have a multiplier impact on the economy. When more people have access to financial system, it can create more employment that could enable them for a higher disposable income which can ultimately enhance the deposit base of the financial institutions. It would be easier to the government to channelise all kinds of subsidies and social fund transfer in an efficient way. For example, Bangladesh government is efficiently providing all kinds of social safety net funds through 1.78 million "10 Taka" bank accounts all over the country.

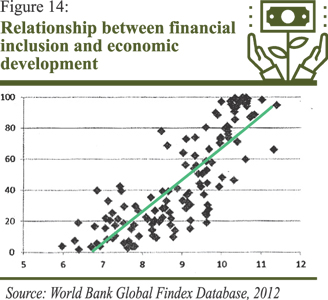

An analysis by World Bank shows a significant linkage between access to finance (proxy by number of account) and economic development (Fig-14). Therefore, an equitable growth can be achieved by ensuring financial services to all irrespective of gender, age, poor, and rich, which can ultimately contribute to increasing the overall efficiency of the economy and the financial stability.

Conclusion:

In developing economies like Bangladesh, banks work as the important agent of mobilising financial resources as savings and allocating those resources as credit or advance for the betterment of the economy. Banks have an important role in the development of a country. As a financial intermediary, the banks can identify the surplus groups as their deposit base and channel those funds to the deficit groups that generate income and economic activities.

Financial access can really boost the financial condition and standards of life of the poor and the disadvantaged population of the country. Lack of accessible, affordable and appropriate financial services has always been a problem and effective inclusive financial system is needed for economic growth of the country.

The number of bank account is increasing as a measure of financial inclusion initiatives. The average balances in the deposit accounts are also on the rise. The share of small deposit accounts is decreasing since the income level of the people is increasing. A steady decline in the average deposit in the small bank accounts is observed which may be an indication to the widening gap between rich and poor in Bangladesh. There might be some other reasons be in the decrease of average balances against small accounts, such as availability of payment instruments like mobile financial services, microfinance institutions and even they might have other reasons, the benefits that marginal people are getting from banks against their savings may not be attractive to them but those are not conclusive. The balances shown against the deposit accounts are for a particular point of time, not throughout the year and there might be some shifts from small deposit accounts to large deposit accounts. The effect of economic transformation during this period is not studied in this paper.

Financial market imperfection that creates due to exclusion of a significant part of a society from formal financial system leads to an unequal society which ultimately hampers the financial stability as a whole. The role of financial inclusion in sustainable economic development is inevitable and well established. However, there is positive and negative impact of financial inclusion on financial stability. Nevertheless, it is quite proved by several researches that financial inclusion coupled with proper and efficient supervision can foster and ensure financial stability much better than any other measures. Therefore, we can conclude about the relationship between financial inclusion and financial stability by mentioning the following findings:

* Financial inclusion is the key to inclusive growth with its motto of empowerment of underprivileged and low income, skilled rural/urban households;

* Inclusive financing has served Bangladesh well to retain real and financial sector stability;

* Inclusive and environmentally responsible financing is of high urgency for low income climate change threatened economies like Bangladesh.

Bangladesh Bank is one of the pioneer central bank which is implementing policies for financial inclusion through unconventional monetary policy. However, there are quite a few things where Bangladesh Bank needs further measures to get fullest benefit of financial inclusion:

* Bangladesh Bank should keep promoting financial inclusion for economic growth to increase the banking penetration in the country;

* Bangladesh Bank should advise Banks for designing more inclusive banking product for financial inclusion;

* Monitoring and supervision of banks through policy intervention is required to ensure broader financial stability and to offset volatility due to financial inclusion;

* Services, such as Agent Banking, ATMs, branches, transaction accounts, and closing gender gaps in account usage, should be promoted as these are supporting financial stability;

To get full benefit of financial inclusion, proper usage of all kinds of financial service, such as account operation, loan, and deposit should be ensured.

Md Anwarul Islam is general manager and Birendra Chnadra Das and Bidhan Chandra Shaha are deputy directors of the Bangladesh Bank. This article is an edited version of a paper presented by the bankers at the Annual Banking Conference held recently under the auspices of the Bangladesh Institute of Bank Management (BIBM).