While Bangladesh has been praised in the media for its success in various socio-economic indicators (e.g. poverty reduction, education and child mortality), mounting non-performing loans (NPLs) arising from financial scandals, mismanagement and nepotism certainly undermine the overall progress of the country in the global arena.

The negative consequences of rising NPLs are now the wake-up call to the management, regulatory authorities, and government to streamline the banking industry.

Non-performing loans, which stood at 10.67 per cent in September 2017, generally mean loans which are in default or close to default, afflict the banking industry in Bangladesh. Considering the crucial link of finance and banking in various sectors in the economy, the troubles of the banking sector embarrass both the banking authorities and the government.

A comparison between the formal banking industry and the microfinance sector may offer some key policy lessons to mitigate such a pressing problem. The microfinance industry constituted Tk 423.5 billion of asset, which was equivalent to only 4.11 per cent of the overall banking sector (Tk 10,314.6 billion of asset) in 2015. Despite being a tiny sector compared to the giant banking industry, it does have some interesting features.

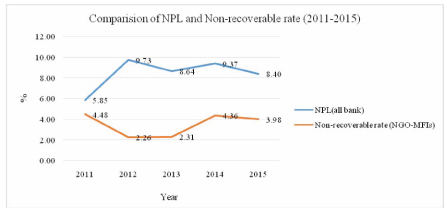

For example, the loan recovery rate, which is often known as collection rate or loan repayment rate, is used to estimate non-recoverable rates of the microfinance industry. The non-recoverable rate, which is estimated by taking the difference between ideal 100 per cent loan collection rate and recovery rate is shown in the graph (non-recoverable rate =100-recovery rate) with NPLs of the banking sector. Since the estimates of NPLs are not available for the microfinance industry in Bangladesh, non-recoverable rate is used for the comparison purpose. However, it should be reminded that the pedagogy may differ between NPLs and non-recoverable rate, but these two terms in general carry the same meaning: both of them are hazardous for the industry's overall financial sustainability.

The graph says it all. While NPLs are soaring in the banking industry, microfinance industry is able to manage a substantial increase in recovery rates, thus, a lower non-recoverable rate: reduced to 2.26 per cent from 4.48 during 2011-12, thanks to the management of microfinance institutions and the Microcredit Regulatory Authority (MRA). NPLs have, on the other hand, increased in the banking sector from 5.849 per cent to 9.728 per cent during the same period and left many in the country terribly shocked, in particular, the depositors.

Overall, NPLs in the banking sector are two to three times higher than the microfinance industry in all the years except 2011. These simple but thoughtful findings have a crucial implication for the banking industry to carefully look at the operational strategies and regulatory environment of the microfinance industry like the loan selection and screening process, collateral and its substitutes, follow-up strategies and innovative demand-based loan products, etc. Simultaneously, the structure of the regulatory authority may provide important lessons to the banking sector which may help reduce NPLs to some extent.

Dr. Aslam Mia, Faculty of Economics & Administration, Centre for Poverty and Development Studies, University of Malaya, Kuala Lumpur, Malaysia.

mdaslam.mia@siswa.um.edu.my

© 2026 - All Rights with The Financial Express