Mazher Mir in the first of a two-part article titled Bangladesh's robust growth, momentum and recent regional conflict | March 08, 2018 00:00:00

Bangladesh has been drawing lots of attention due to its economic growth, young population and commitment to innovation and economic activities. The 2016 gross domestic product (GDP) growth emphasises an impressive economic success story that has been on the rise over the last two decades. In fact, the country saw GDP rise by approximately 180 per cent from 2005 to 2015. Bangladesh has been successful in developing an economy capable of establishing itself in the global marketplace as a financially independent nation.

While the historic performance has been impressive, the current economic and regional conflicts raise questions in regards to the future outlook for Bangladesh's economy. Bangladesh would benefit by looking at the economy as a business where they need international stakeholders to be on its side. To bring in international investors to participate in the local companies, the government should create a condition where local large companies have access to the global equity market through the international stock exchanges. In any global or regional financial or political turmoil, Bangladesh needs the international community to find interest in it as we know often time human rights issues were neglected when economic issues didn't break the deal.

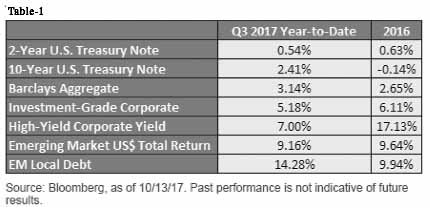

No one knows when volatility may arise. The government needs to utilise this time of success to take advantage of opportunities and hedge against adverse conditions. This has to start with the Treasury taking a proactive approach to structuring the financial accounts and actively managing the reserves. A well-coordinated strategic plan should incorporate the use of derivatives for the securities held in the US Treasuries as well as holdings in foreign currencies. The use of covered calls is the safest inclusion of derivatives, and it not only increases the current income of a holding but also hedges against volatile markets. Understanding that Bangladesh investing currently in US Treasury Securities may arguably be one of the safest investments in the world. There is also an opportunity to add yield well above the current interest rates. A majority of the country's reserves are held in foreign currencies, that they are not actively managed. Like many countries, Bangladesh holds a large amount of US treasury as its stability is well accepted. Yet, it's hard to accept this following return (shown in Table 1) when the market is doing so well.

If we look at the history of currency, we see that nothing is set in stone for the perpetuity. It is beneficial to be able to explore and actively manage US Treasury account and perhaps consider alternatives to avoid more opportunity cost.

ACTIVELY MANAGING THE US TREASURY ACCOUNT: The use of options in this manner is available to add an additional source of revenue and increase yields. An active strategy should increase yields on US Treasury holdings by an additional 2.0-3.0 per cent, and increase the yields on reserves in foreign currencies by an additional 4.0-8.0 per cent. At the same time, hedging against volatile markets and establishing a plan to move the Balance of Payments (BoP) into the positive can be done by accessing international commodity's supply and demand. Here are some strategies:

Investment objectives: In the foreign exchange (FOREX) marketplace and with the use of derivatives for both US Treasuries and foreign currency the Bangladesh Bank (BB)'s treasury portfolio should be structured in such a manner that it will yield above current treasury rates, using securities in conjunction with covered call positions that are both at-the-money and out-of-the-money. Additionally, including foreign currency in the portfolio will both create a hedge against global economic uncertainties, as well as become an additional revenue stream with the use of covered calls in the same manner as the treasuries. This can be done in conjunction with the Treasury Board to add value by generating revenue to pay debts, hedge against currency exchanges, hedge against fluctuating interest rates, and provide an additional inflow of revenue to support the BoP.

Customisation: The strategies employed and the portfolio construction can both be customised based on current financial needs, as well as to adjust to changing economic and market conditions. Depending on economic and market conditions different tactics and securities may be employed to take advantage of opportunities or hedge against adverse conditions. The structure of the portfolio will be inclusive, based on the entire treasury reserves and investments, and the current objectives set by the treasury board. Examples of this would be selecting specific covered call positions, foreign currency positions, or foreign currency covered call positions to assist in meeting an upcoming debt repayment. Continuous monitoring of economic conditions and working directly with the treasury department will ensure that the portfolio and strategy will be adjusted to meet the financial requirements.

Treasury strategy: The portion invested in Treasury securities should be approximately 1/4th of the reserve. The portfolio will be laddered to include short term and long term ranging from one month to five-year maturities and will include a portion invested in treasury futures to write calls against. The futures positions will be purchased to mature one period into the future and then a call will be written against this position. The target goal will be to increase annual yield by 2.0-3.0 per cent through the use of covered calls against the treasury future positions. Additional benefits would be the additional capital received by the option position can be used to fund debt repayments as opposed to selling a treasury position outright and losing that yield.

For an example, if invested simply in two-year (2Y) T-Notes the current yield would be 1.3 per cent. Now if we employ the use of covered calls we would take half these funds and instead invest in 2Y T-Note futures. We then write calls against these positions with a premium that yields 5.0 per cent annualised. The result then would be an increase of 2.5 per cent on the overall position, and the total yield is increased to 3.8 per cent. These option premiums are also useful for funding without the need to close out a position. Using the same example, a $1.0 billion position would net a monthly premium of approximately $4.5 million without the need to sell any security.

This shows the average returns for simply buying and holding US Treasuries vs additional active management through the use of covered calls with an investment of $8.0 billion. The average return for treasuries is 1.2 per cent, and the average additional value from active management is 2.0 per cent (3.2 per cent total).

Over the course of five years' active management would outgrow the current treasury's investment strategy by $873 million. If we assumed active management averaged 2.5 per cent additional annual yield, it would have been over a billion more. And at 3.0 per cent, it would nearly be a billion and a half. The greatest part is this additional yield comes with no great assumption of risk. (Table II)

Mazher Mir works in the US financial industry and has experiences

in the sector for last 15 years.

mazhermir2100@gmail.com

© 2026 - All Rights with The Financial Express