Amid deafening buzz over Bitcoin over the past months due to its rising acceptability and bubbling price trend, world media and experts have apparently overshadowed the upcoming digital revolution by blockchain technology. Over the years, internet has been information-based, but now it is turning out to be 'information web of value'. Though Bitcoin and other crypto-currencies provide the buyers more liquidity, privacy, anonymity and personalised transactions, these expose the parties to a number of risks due to price fluctuation, risks of exchanges being hacked, malware attacks in e-wallets and lack of buyer protection.

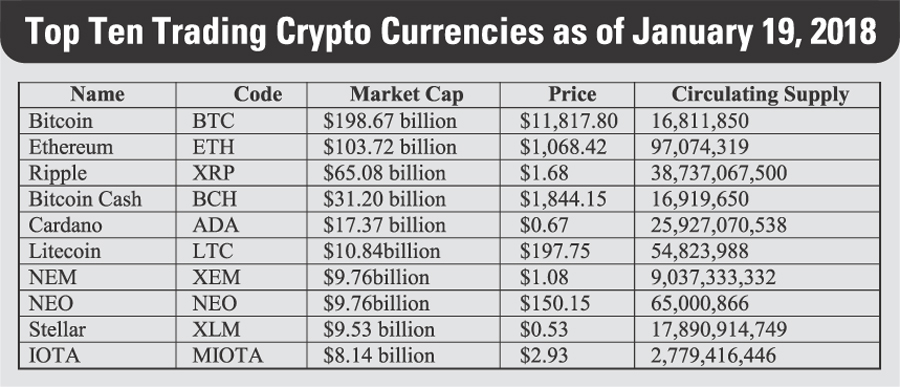

Most importantly, trading of crypto-currencies in online exchanges is a way far from the leashes of central banks around the world. This subsequently increases anti-money laundering threats and illicit purchases. Till date, there have been 1,453 crypto-currencies traded and used as medium of exchange around the world. As recorded on January 18, 2018, the total market capitalisation of all of cyber coins is US$ 592.61 billion, which is slightly higher than gross domestic product (GDP) of Sweden, the world's 22nd largest economy. Out of the total market capitalisation, Bitcoin accounts for around US$ 198.7 billion followed by Ethereum (US$ 103.7 billion) and Ripple (US$ 65 billion).

Since the digital currencies are grabbing attention causing bubbling price movements year by year, especially after the genesis of Bitcoin nine years ago by Satoshi Nagamoto (alias), the leading central banks are terming these as highly speculative assets which a large pool of investors or buyers use as medium of exchange and asset base. According to Bloomberg, the leading central bankers are concerned about emergence and growth of the private cryptocurrencies -- both for their volatile price moves and in the case of Bitcoin at least, their introduction on regulated derivatives exchanges. The second concern is whether to issue official versions.

Being one of the applications of blockchain technology, these digital currencies unearth several major risk-escalating events since there had been incidents where hackers demanded ransom in Bitcoin. It invariably gives whopping chances to tax evaders, drug dealers and parties in illicit transactions causing money laundering incidents. It has to be remembered that blockchain has many other applications to be innovated in the banking services in international trade, treasury, syndication, compliance and AML activities.

So how did the central banks in leading economies react to this non-grata techno currency? The Federal Reserve expressed its ocean-deep concern regarding the privacy issues of crypto-currencies. The Eurozone considers digital currencies' impact on its economy as being limited and posing no threat so far. China has been ready to embrace these currencies to improve payment efficiency and allow accurate control of currencies for which its' central bank is working from 2014. The Bank of Japan has no imminent plan to issue crypto-currencies and disregard these as an obstacle of Japan's monetary policy. Germany's Bundesbank is wary over the reverberating issuance of crypto-currencies having 'speculative character' and thinks that it would disrupt mainstream banks' business models. The Bank of England termed these as a sign of financial revolution and anticipates that these would help the central banks strengthen their defenses against cyber attacks. The Bank of France warned its citizens to exercise caution as these are not institutionalised to provide public confidence. Use of crypto-currencies is a violation of foreign exchange rules in India.

Seemingly, the most apparent threat for investing in crypto-currencies is having no regulatory protection for investors. Investors can lose money and get involved in illegal transactions or may be exposed to cyber threats for which they would not be able to obtain any insurance scheme. The movement of actual currencies would also be in question. It would also be paradoxical if money laundered in the coming years declines (currently, money laundering equals 2 per cent-5 per cent of global GDP), according to the United Nations Office on Drugs and Crime due to shift in delivery channel from traditional paper money to crypto-currencies.

Keeping untoward dangers arising from crypto-currencies which would expose the international banking system and regulations to formidable risks and loss of public money, can we envisage regulated and bank-accepted digital currencies to level the polarised game? Perhaps, the situation has the answer itself. Out of thousands of cryptos, Ripple is the only digital currency that has been accepted by some large global banks where the funds for transactions are held in settlement accounts in segregated manner. Ripple's goal is to enable secure, instant and nearly free global financial transactions.

Based on centralised blockchain enterprise solution, Ripple payment protocol has been being experimented from 2004, five years before release of Bitcoin, under the name 'RipplePay'. In 2012, it descended in the crypto-currency market after Bitcoin. In terms of market capitalisation, Ripple holds the third place after Bitcoin and Ethereum with total market cap of US$ 65 billion. Rather than a currency, Ripple protocol is payment network used by several banks as their forward-looking settlement infrastructure. So far, it has been able to partner with leading global banks like Unicredit, American Express, UBS, Santander Bank, Siam Commercial Bank, CIBC, Deloitte, Accenture, Temenos Group, Westpac Banking Corp. and others to secure payment network and strengthen e-commerce through specific focus on B2B transactions and remittance transfers.

So, why would an investor choose Ripple over Bitcoin? There are certain advantages of Ripple that Bitcoin or other strong digital currencies do not promise. Such as, Ripples are designed to be a passageway for transactions to take place and as a bridge between other currencies. While Bitcoin and others are being traded or mediated in decentralised ledger technology, Ripple is being traded in centralised enterprise blockchain solution for banks, payment providers and digital asset exchanges, which provide more security to the buyers' fund. As expert banks and tech companies are coming up with regulations to control and oversee crypto currencies, Ripple would not be adversely affected by the looming regulations as it has already been accepted by global banks. Most of the digital currencies use third-party or exchange to convert local currency to crypto currency and vice versa. Ripple protocol can conduct full transactions without third-party which reduces counter-party risk drastically. It is designed to be able to be compliant with banking security, risk and privacy requirements such as Anti-money Laundering (AML), and Know Your Customer (KYC) practices.

Ripple provides instant settlements for interbank transactions which are normally conducted through decades-old SWIFT messaging. Some exchanges, i.e., Plus 500 offers the Ripple buyers with compensation fund up to 30,000 euros. These exchanges are regulated by Financial Conduct Authority (FCA), Cyprus Securities Exchange and Australian Securities and Investment Commission.

In April 2017, Ripple was being traded at US$ 0.03 whereas it hit US$ 3.37 at the beginning of January 2018. A hedge fund of US$ 100 million denominated in Ripple is being launched by prominent tech figure Michael Arrington. The fund would be used to invest in crypto currencies to minimise the risk of the crypto-investors. In fact, not only does Ripple provide liquidity for cross-border payments, it's the fastest, most scalable and stable digital currency, making it the most appropriate for institutional use and banking system.

US Equity Research estimates the crypto-currency market is expected to grow at a 32 per cent rate by 2023. The world is about to experience a financial revolution powered by e-commerce where internet would not be a source of information only; rather it would be a massive powerhouse for cross-border businesses, instant payments, robust data security and profit-for-all eco-system. Accepted crypto-currencies are a part of where blockchain would be a platform. However, would it be possible to address the AML risk and ensure KYC for current banking system all around the world? Where does the currency exchange get going? Can terrorist financing and illicit transactions be combatted through a separate global regulator? Which party would be responsible if investors lose a big fortune by being hacked? What is the dispute resolution method for crypto-currencies? These un-answered issues are still to be addressed and till then, the features of crypto-currencies do not make these probable substitute currencies; rather these are just speculative assets.

The writer is working as Senior Risk Manager in a private bank in Bangladesh.

adnaan.jml@gmail.com

© 2026 - All Rights with The Financial Express