Adnan Rashid and Kamrul Hasan Azad | December 25, 2017 00:00:00

Small and medium enterprises (SMEs) are inherently considered risky financing option for financial institutions (banks and non-bank financial institutions) around the world. This is due to their unstructured and low equity position and limited product mix. Thus they have a crowded market positioning. SMEs also lack collateral that most banks consider quintessential for any sort of loan exposure to its clientele.

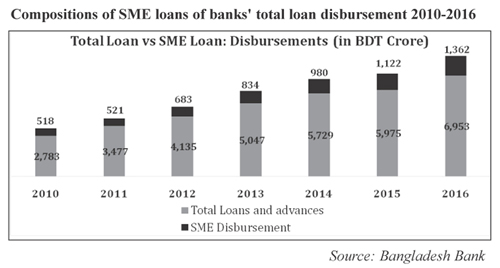

Although proven profitable and sustainable by many financial institutions in Bangladesh, if we still look at the central bank data, only 29 per cent of the total loan portfolio of the banking industry is provided to SMEs. At the end of June 2017, only 23 per cent of total loan disbursed by banks went to SMEs. In fact, SME financing got major headwind mainly in last 10 years, thanks to our central bank's initiatives for financial inclusion via various refinancing facilities and directives.

Still, many banks are yet to develop noteworthy SME-focused business strategy and essential products to cater to growing and diverse needs of financing requirement for the SMEs. More than one-third of the scheduled banks in Bangladesh are yet to invest even one-fifth of their loan portfolio in SME financing. One of major reasons behind this phenomenon is the lack of understanding of the risks associated with SMEs and the unpredictability of their cash flow. In addition, the absence of collateral creates hesitation in banks to fully invest its money in SME market where loans are bit-sized, these require several years to develop a sizable portfolio and need substantial investment in processes and resources.

In many countries, Credit Guarantee Scheme (CGS) is deployed to nudge reluctant banks to enter the unchartered territories of SME markets that can further boost financial inclusion and spur economic growth alongside generating a sustainable revenue stream for banks. It also helps banks undertake higher risk by providing limited coverage and hence, helps financial institutions to penetrate higher risk premium market and reinforce its already razor-thin interest margin.

CGS helps banks to share the risk of loan default for a specific type or market of customers via a simple process. A regulatory body or similar organisation provides or issues credit guarantee via CGS method to a financial institution to minimise or share the risk financing to SMEs and help these enterprises get loans at their expected level with insufficient collateral. Usually, financial institutions have to sign a memorandum of understanding with the guarantee issuing organisation and pay an annual fee to participate in the CGS programme. If the loan to a CGS-supported SME goes south, that guarantee issuing organisation will bear the burden of a certain portion of the defaulted loan upon guarantee fee paid at the time of loan disbursement. This limits banks' possible loss from that client in the grimmest situation and acts as an alternative of a partial collateral against the loan.

The guarantee scheme can come in different shapes and ways. CGS can be contract-wise for a certain type of customers, where, for instance, 50 per cent of loan loss can be covered.

It can be of portfolio-wise, where 30 per cent of the loss of an entire portfolio can be covered, for instance. Also, it can be a hybrid one where there is a cap on the loss of the entire portfolio and also on each contract within that portfolio.

It can be of portfolio-wise, where 30 per cent of the loss of an entire portfolio can be covered, for instance. Also, it can be a hybrid one where there is a cap on the loss of the entire portfolio and also on each contract within that portfolio.

Generally, the higher the loss coverage, the higher is the guarantee fee. Like an insurance product, the guarantee fee works here as a compensation to undertake the higher risk of loss for the guarantee issuer. Interestingly, it is not necessary for a credit guarantee scheme to serve solely for development purpose. It can also have a business angle whereby guarantee fee works as revenue. As long as the accumulated loan loss amount plus CGS management costs does not exceed the accumulated fee income, there is a profit to be made. In many countries, there are well-managed credit guarantee schemes running profitably. However, the economic benefit and financial inclusion aspects of CGS are substantial in the sense that it can assist a financial institution to venture into an unknown market or go deeper into the bottom of the pyramid admitting more businesses in banking coverage and injecting much-needed fund to collateral-strapped micro and small businesses to spur economic growth.

Apart from many countries in Africa and Europe, many Asian countries have success stories of CGS in SME financing, namely India, Japan, South Korea, Taiwan and Thailand. Of these, Thailand has a strong institutional presence in government-sponsored credit guarantee scheme. Thai Credit Guarantee Corporation (TCG) is an autonomous body that once started under government subsidy, but over the years became financially independent, playing a pivotal role in SME and micro credit development in urban and rural Thailand via several credit guarantee schemes through public and private sector banks. In India, Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) is another such institution that facilitates the flow of collateral-free credit to local MSEs. Such institutional presence of regulatory body allows SMEs of that country to take full advantage of CGS and its benefits of financial inclusion, and thereby, help banks to venture into different untouched areas and market segments that considered vital for economic emancipation. For instance, Japan and Korea, both with vibrant SME sectors, have outstanding SME credit guarantees in excess of 5 per cent of their gross domestic product (GDP).

In Bangladesh, there had been a few attempts at launching credit guarantee scheme that did not work out as planned due to lack of proper planning, understanding and moral hazard. One of the major lessons was to educate borrowers and lenders not to treat funds under guarantee as a free fund or government subsidy since it is guaranteed. If the loan loss is properly shared with the lender (bank), the scheme is properly priced (guarantee fee), and borrower's funding need is properly assessed and monitored by both lender and guarantor, such pitfalls can be avoided. Therefore, a proper, well-thought-out and visionary approach is needed to develop a feasible and sustainable mechanism of credit guarantee scheme in Bangladesh for extracting its true benefits.

The potential of credit guarantee scheme is enormous in Bangladesh specially in bringing our formal banking sector to unserved and under-served SME market in need of greater financing penetration. Credit guarantee is also a great substitute for collateral, and hence, an ideal tool for small borrowers who do not have any funding option or completely dependent on informal borrowing only due to lack of collateral. Credit guarantee scheme can also play a significant role in the development of target segments, such as woman entrepreneurs, start-ups, or target sectors or industry, such as handicrafts, jamdani manufacturers, light engineering and so on. A concerted effort by the government, central bank, and financial institutions is necessary to evaluate and assess the prospect of a well-engineered credit guarantee scheme to bring home greater benefit of financial inclusion and economic development through widened and deeper SME financing.

Adnan Rashid is Assistant General Manager and Head of Credit (Small Business) at IDLC Finance Limited and Kamrul Hasan Azad? is Deputy Director of Bangladesh Bank

adnan.rshd@gmail.com

© 2026 - All Rights with The Financial Express