Finance Minister Amir Khosru Mahmud Chowdhury recently told parliament that the government has prepared an action plan to build a trillion-dollar economy by 2034. The plan covers investment, employment, exports, remittances, skills development and macroeconomic stability. But the trillion-dollar target is less an economic growth problem than an exchange rate problem. So the issue is not just how fast the economy grows, but how much of that growth survives in dollar terms.

That trillion-dollar target was a centerpiece of the BNP manifesto, which helped carry the party to its victory in February 2026. Now in government, BNP must convert a campaign number into a policy framework. The problem is that the arithmetic behind the number is more fragile than the slogan suggests.

Dollar GDP depends on three things: real output growth, inflation, and the taka-dollar rate. To go from around $470 billion today to $1 trillion by 2034 requires roughly 10 per cent annual growth in dollar terms.

If Bangladesh grows at 5 per cent in real terms and inflation runs at 7 per cent, the economy grows by about 12 per cent in nominal taka terms. But if the taka depreciates by 3 per cent a year against the dollar, three percentage points are lost in conversion, leaving nominal dollar growth to about 9 per cent, short of the required 10. So, even fairly strong growth at home may not be enough if the currency keeps losing value.

If Bangladesh grows at 5 per cent in real terms and inflation runs at 7 per cent, the economy grows by about 12 per cent in nominal taka terms. But if the taka depreciates by 3 per cent a year against the dollar, three percentage points are lost in conversion, leaving nominal dollar growth to about 9 per cent, short of the required 10. So, even fairly strong growth at home may not be enough if the currency keeps losing value.

The ongoing US-Israel-Iran war has made this arithmetic harder for Bangladesh. Oil prices touched $117 a barrel before a fragile two-week ceasefire pulled them back to around $94, still 40 percent above pre-war levels. At this price, the energy import bill has already risen by several billion dollars, squeezing foreign exchange reserves and pushing up transport and electricity costs. A breakdown of the ceasefire would make things considerably worse.

Since the fiscal year began in July 2025, Bangladesh Bank has bought about $4 billion from the interbank market. As a result, gross reserves had risen to $34 billion by early February, the highest level in more than three years. This is enough to cover about five months of imports. With remittance inflows coming at a strong pace in recent months, the taka was under upward pressure and would likely have appreciated if the market had been left on its own. Instead, Bangladesh Bank continued buying dollars to keep the exchange rate broadly stable at around Tk 122 per dollar. Since March 8, however, it has started to let the taka weaken gradually as the risks from the war have become more apparent. The rate has since moved closer to Tk 123.

This shift exposes a basic tension at the center of the trillion-dollar plan. From the standpoint of rebuilding reserves, buying dollars makes sense. We all know that between 2022 and 2024, the official reserve has fallen from $48 billion to $24 billion. But a weaker taka, while helpful for exporters, undermines the effort to reach a trillion dollars in nominal dollar terms. In other words, the same policy that is helping to rebuild reserves is also pushing us away from the dollar target.

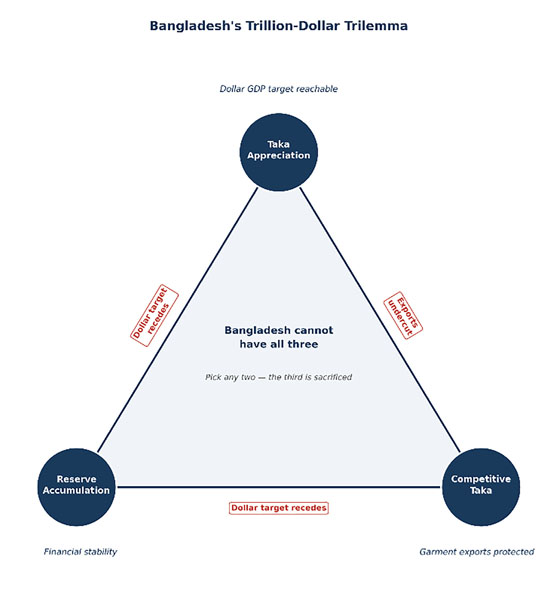

The problem is threefold, and no country can pursue all three objectives at once. A weaker taka helps exporters stay competitive and makes it easier to buy dollars for reserves. A stronger taka, by contrast, means the same output converts into more dollars and raises dollar GDP on paper, but it squeezes export margins. Building reserves means buying dollars by releasing taka into the market, which weakens the currency. So the three objectives - reserve adequacy, export competitiveness, and a trillion-dollar GDP target - pull Bangladesh Bank in incompatible directions. Only two can be served well at any one time; the third must give way. This is the trilemma at the heart of Bangladesh's exchange rate policy. The following picture summarizes it visually.

It should be pointed out that stronger productivity growth could ease this tension in that exporters can stay competitive even with a stronger domestic currency. But this would require the kind of industrial upgrading which we have not achieved in Bangladesh. Moreover, the BNP manifesto does not face this trade-off directly. It promises all three.

None of this means the trillion-dollar target is misguided. The trilemma only lays bare the contradiction embedded in the plan. If Bangladesh can maintain the growth pace it experienced in the last decade, with moderate inflation and contained depreciation, the country could reach roughly $900 billion by 2034 and cross a trillion a year or two later.

Much also depends on how Bangladesh Bank manages this trilemma going forward. Continuing with the current policy of letting the taka depreciate slowly and predictably is probably the safest route, as it protects exporters, helps rebuild reserves, and avoids a sudden currency shock. But the compounding effects of a gradual depreciation will erode dollar GDP over time, and Bangladesh Bank will eventually have to be open about which of the three objectives it is willing to sacrifice, and when. The trillion-dollar figure makes for a compelling campaign slogan, but it is a poor policy anchor. What matters most are the fundamentals: growth, export diversification, and reserve adequacy. If Bangladesh gets those right, the dollar number will take care of itself, perhaps by 2035 rather than 2034. That is not failure; it is honest arithmetic.

Syed Abul Basher is an independent researcher and former professor of economics at East West University, Dhaka. syed.basher@gmail.com

© 2026 - All Rights with The Financial Express