In a determined effort to combat the high rate of inflation, the interim government has taken a significant step by increasing the rate of profits on various savings certificates from the beginning of the current year. This move, in line with the central bank's tight monetary stance and rate hike, is aimed at curbing the money supply in the market and thereby reducing inflation. The surge in interest rates on deposits and loans in the banks, a direct result of the central bank's persistent repo rate hike, is a clear indication of the government's commitment to this cause.

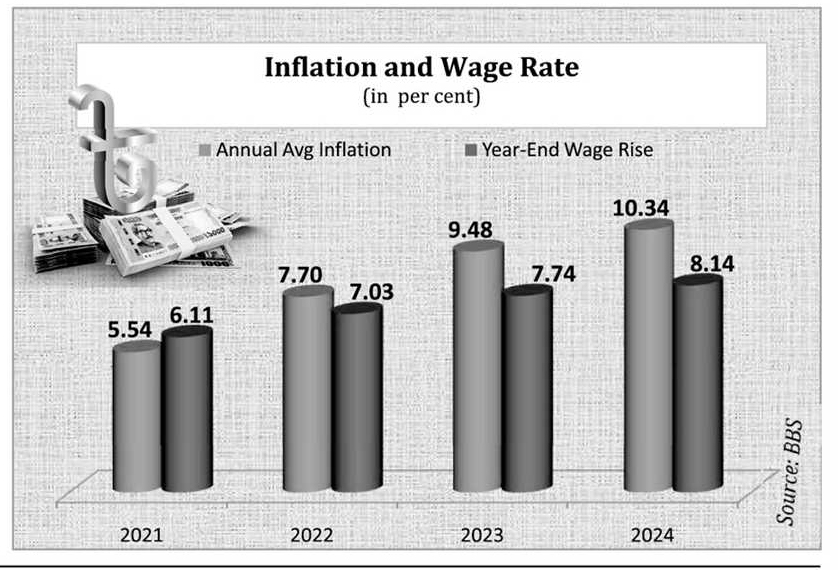

Despite rate hikes for the last couple of months, the inflation rate is yet to come down significantly. Monthly headline inflation initially reduced to 9.92 per cent in September last from 10.49 per cent in August. Later, the rate increased to 10.87 per cent in October, 11.38 per cent in November, and cane down to 10.89 per cent in December. Thus, the annual average inflation at the end of 2024 stood at 10.34 per cent, reflecting the rise in cost of living.

The half-yearly monetary policy statement (MPS), announced in July last by the ousted Hasina regime, set a target to bringing down the inflation rate to 6.50 per cent at the end of the current fiscal year (FY25) or by the end of June next. As it was in the previous year, it will not be achieved.

Now, the yield rates on four types of savings certificates have increased to as high as 12.55 per cent on January 1 this year from a minimum of 9.50 per cent. Earlier, the profit rates stayed between 9.50 per cent and 11.76 per cent depending on the amount of investment ceilings and types of savings certificates. The rates were lower for higher investments. After the latest hike, profit rates ranged between 12.25 per cent and 12.55 per cent, aligning with the average yields of 2-year and 5-year treasury bonds at 12.27 per cent and 12.32 per cent, respectively.

The hike in profit rates of savings certificates is likely to extract more money from the public into these non-tradable fixed-income securities and also help the government to finance part of the budget deficit, especially when the inflow of foreign financing is not adequate.

Prior to the hike in the rates of non-tradable government debt instruments, the government made another significant move by increasing value-added tax (VAT) and supplementary duties on more than 100 products and services. This mid-year hike, aimed at collecting some Tk 120 billion, is a clear response to the lack of adequate revenue mobilisation. It also serves as a step towards fulfilling the conditions of the International Monetary Fund (IMF) as part of fiscal reform. The ousted Hasina regime sought IMF support to manage the looming economic crisis, and the IMF agreed to provide $4.70 billion in three years, subject to the fulfillment of various conditions.

Some of these products and services are non-essential or semi-luxury and unlikely to affect the cost of living despite increases in prices due to tax rises. For instance, despite the increase in prices of products like cigarettes and artificially flavoured drinks, it is unlikely to put any real burden on consumers. However, for the average consumer, the rise in VAT and duties on essential products and services could significantly impact their budget. Moreover, these products are known as health hazarding and require some prohibition. National Board of Revenue (NBR) is also expecting that over one-third of the projected Tk 120 billion in additional revenues in the next six months through a surprise VAT hike will come from four prohibitively taxed items. These are cigarettes, artificially flavoured drinks, and both carbonated and non-carbonated electrolyte drinks. Thus, the overall impact of the sudden rise in VAT should be mixed. As VAT is an indirect tax, it is applicable to all those who use or consume products. So, both the rich and the poor have to pay the same amount of VAT. The move, thus, indicates that the government is relying more on indirect taxation to generate revenue, which is easy and less efficient.

The main problem is that the rise in VAT and duties comes at a time of high inflation, which has also eroded the real income of fixed-income people significantly. The trend has continued for more than two years. In 2023, the annual average rise in the national wage index was slightly higher than 7 per cent against the average yearly inflation of 9.48 per cent. Again, in 2024, the annual average inflation was 10.48 per cent when the country's average wage increased by 8 per cent.

It is now clear that the battle against inflation has already become harder for the government, and more people are suffering due to the high cost of living. The persistent rate hike, though necessary, has yet to contain the surge in inflation adequately. So, bringing inflation down to the optimal level seems like a long way to go. The rate hike or application of monetary instruments has now exposed its limitations. Moreover, the rise in interest rates has made the investment and business costly. Central bank statistics showed that the Weighted Average Interest Rate (WAIR), a key economic indicator that measures the average interest rate paid on advances in banks, increased to 11.77 per cent in October from 11.52 per cent in June last year. The rate for SMEs surged to 12.09 per cent from 11.80 per cent during the period under review.

There are indications that the upcoming half-yearly monetary policy, expected to be announced in the next week, will maintain the current stance due to the ongoing inflationary pressures. This suggests that further rate hikes may be on the horizon. The potential impact of this move on the economy remains uncertain. In this context, the government's focus on fixing the supply chain and ensuring a steady flow of products to stabilise prices becomes even more crucial. It is imperative that the market operates efficiently, as any inefficiency could exacerbate the current economic challenges.

asjadulk@gmail.com

© 2026 - All Rights with The Financial Express