Once, banks catered exclusively to well-off entrepreneurs, with their doors hardly accessible to those most in need of financial resources to build a better future. This left small investors and farmers at the mercy of local moneylenders, known as 'Mohajon,' who exploited them with high-interest loans secured against collateral, often resulting in the loss of their property. However, a silent revolution began in the late 1970s.

Microfinance institutions (MFIs) have emerged as a transformative force, now reaching over 42 per cent of a population previously invisible to the formal financial system (Microfinance in Bangladesh - Annual Statistics, 2023). These institutions have not only addressed the struggles of the extreme poor but have also extended their services to the 'missing middle'-those often overlooked by traditional banks and MFIs.

Today, MFIs employ 206,000 people and have disbursed an impressive amount of BDT 2493.02 billion to clients across the country, playing a crucial role in GDP growth and promoting financial inclusion. These once modest microcredit ventures have now become significant contributors to the nation's economic development.

These institutions extended their support to the most vulnerable: the farmer dreaming of a bountiful harvest and the weaver with the skill but lacking the means to purchase materials. Microfinance became the catalyst for unlocking their potential, enabling the creation of exquisite fabrics and the sustenance of families. As a result, markets flourished with entrepreneurship, families envisioned brighter futures, and Bangladesh's economic landscape began its transformation.

The recent student movement has exposed and dismantled deep-seated governance failures, leading to the formation of an interim government under the leadership of Nobel Laureate Professor Muhammad Yunus. Renowned for his pioneering work in global microfinance and advocacy for social business, Professor Yunus is now spearheading the nation's reconstruction with a renewed emphasis on resilience.

Microfinance, under his guidance, is poised to be a powerful tool, facilitating connections between millions of women, entrepreneurs, and farmers with technology. Envision a network of tech-enhanced MFIs reaching every corner of Bangladesh, serving 66.82 million clients, including 45.30 million borrowers. Imagine farmers accessing financial advice through mobile apps, young entrepreneurs applying for loans online, and entire communities rising from poverty. These figures are more than mere statistics-they represent real stories of transformation in progress.

Addressing key challenges and leveraging opportunities

High borrowing costs and operational expenses: One key challenge for MFIs is the cost of fund. While MFI provides microfinance at a relatively low rates, they often rely on loans with higher interest rates ranging from 13.5 per cent-14.5 per cent. In addition, they have to keep collateral of around 10 per cent-20 per cent despite low interest rates. This creates a crucial financial squeeze, limiting their ability to support the most vulnerable populations effectively. Additionally, operational efficiency is critical. Reaching remote areas and serving a vast clientele necessitate innovative solutions and streamlined processes. Every cost saved translates to a wider reach and increased impact for MFIs.

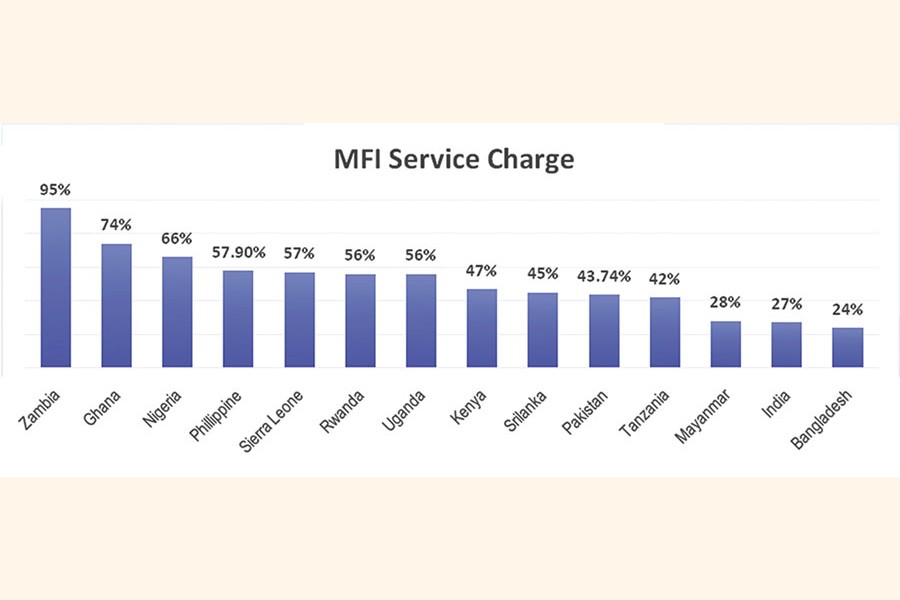

Comparatively low interest rates and the need for safeguarding: A crucial differentiator for Bangladesh's microfinance sector is its remarkably low interest rates compared to regional counterparts.

This achievement reflects the success of past policies and regulations in fostering an inclusive financial environment. However, the recent hike in cost of fund, and operational cost need to be revised. Currently, Bangladeshi MFIs' service charges rise to a high of 24 per cent in a declining method (Yield around 22%).

Looking Ahead: a supportive national budget for continued growth

The National Budget for the fiscal year 2024-2025 can further nurture the microfinance ecosystem. Strategies such as low-cost funding from Bangladesh Bank, tailored regulations recognising the unique needs of MFIs, and investments in digital infrastructure can empower these institutions to reach even the most remote corners of the country. This will enable them to thrive, expand their services, and unlock the full potential of financial inclusion for a brighter economic future for the people of Bangladesh.

National budget proposals for MFI growth:

1. Low-Cost Funding: Create low-interest loan facilities for MFIs via Bangladesh Bank to enable more affordable client rates.

2. Regulatory Support:

• Adapt regulations to balance financial inclusion with operational sustainability.

• Provide legal protections for MFIs in disaster-prone areas to mitigate risks.

3. Capacity Building:

• Implement training programmes for MFI staff on best practices and digital finance.

• Allocate budget for business support services to empower MFI clients.

4. Technological Investments:

• Invest in digital infrastructure for mobile banking and online lending.

• Offer grants or subsidies for technology adoption to improve remote services.

5. Disaster Relief Funds:

• Establish contingency funds for MFIs during crises to ensure continuous service and stability.

• Develop risk mitigation mechanisms for loans to protect institutions and clients.

6. Public-Private Partnerships:

• Foster collaborative projects to enhance resource mobilisation and impact.

Balancing service charges for sustainability

Unlike traditional banks, MFIs incur higher operational costs by delivering diverse small and medium loan products directly to borrowers and providing continuous support for better utilisation of the funds. Inflation and rising operational expenses further limit the growth potential of MFIs.

The service charges of MFIs in Bangladesh are lower compared to regional peers. A moderate, well-structured increase in these charges could help MFIs cover their operational costs without significantly affecting borrower affordability.

Revising service charges for a more sustainable MFI ecosystem could lead to:

• Improved Services: More resources for technology, broader reach, and diverse financial products.

• Enhanced Financial Inclusion: Serving a larger population, especially those excluded from traditional banks.

• Long-term impact: Securing the financial health and sustainability of microfinance for poverty alleviation and economic empowerment.

In the spirit of progress and innovation, the MFI sector looks forward to the continued support of Professor Yunus and the interim government in shaping up a national budget that champions MFIs in Bangladesh for greater good of the economy. To rebuild the economy with inner strength, MFIs can play a vital role through financial inclusion and empowerment of the millions. This approach aligns with the broader goal of building a nation where technology and financial access uplift every corner of society, transforming lives and driving economic prosperity.

The author is Executive Director, POPI and Chairman of Credit Development Forum (the largest and sole forum representing the MFI sector in Bangladesh)

© 2026 - All Rights with The Financial Express