Microenterprises (MEs), one of the major driving forces of Bangladesh's economy, are facing a severe finance gap. The actual supply of finance to MEs lags far behind their potential demand. Considering the current position of Bangladesh's economy, this is high time to reduce that gap through coordinated public and private sector initiatives.

Microenterprises (MEs), one of the major driving forces of Bangladesh's economy, are facing a severe finance gap. The actual supply of finance to MEs lags far behind their potential demand. Considering the current position of Bangladesh's economy, this is high time to reduce that gap through coordinated public and private sector initiatives.

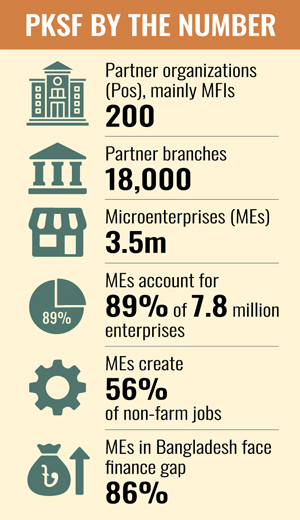

![]() Palli Karma-Sahayak Foundation (PKSF), an apex development institution established by the Government of Bangladesh, has long been implementing a comprehensive microenterprise development programme combining various financial and non-financial services for sustainable poverty alleviation through self and wage employment. With support from development partners and the government, PKSF works through an institutional network of around 200 Partner Organizations (POs), mainly Microfinance Institutions (MFIs), operating from 18,000 branches. Currently, around 3.5 million MEs receive services under PKSF's microenterprise development programme.

Palli Karma-Sahayak Foundation (PKSF), an apex development institution established by the Government of Bangladesh, has long been implementing a comprehensive microenterprise development programme combining various financial and non-financial services for sustainable poverty alleviation through self and wage employment. With support from development partners and the government, PKSF works through an institutional network of around 200 Partner Organizations (POs), mainly Microfinance Institutions (MFIs), operating from 18,000 branches. Currently, around 3.5 million MEs receive services under PKSF's microenterprise development programme.

Despite public and private initiatives, the average finance gap for MEs continues to widen each year. In response, PKSF has initiated a strategic intervention: the Credit Enhancement Scheme (CES), with financial and technical support from the Asian Development Bank (ADB). This initiative aims to boost credit flow from banks and financial institutions to MEs.

Role, potential of MEs: MEs account for 89% of Bangladesh's 7.8 million enterprises and generate approximately 56% of the total non-farm employment. Scattered across the country, MEs add value to local raw materials and provide employment for both skilled and unskilled local workers. Their contributions to local economies make them essential to building a sustainable national economy. The majority of those employed in MEs belong to low-income groups, making MEs a crucial means of reducing income inequality and alleviating multidimensional poverty.

Nearly 70% of MEs are based in rural areas. By strengthening rural economies, these enterprises help curb rural-urban migration and bridge the rural-urban economic disparity. A large number of MEs are owned or managed by women, which promotes gender equity and empowers women by giving them financial control.

Nearly 70% of MEs are based in rural areas. By strengthening rural economies, these enterprises help curb rural-urban migration and bridge the rural-urban economic disparity. A large number of MEs are owned or managed by women, which promotes gender equity and empowers women by giving them financial control.

Meanwhile, the youth unemployment rate in Bangladesh stands at around 15.74%. Every year, more than 2 million young people enter the workforce. Expanding support for MEs, especially startups, presents a strong opportunity to create employment and uphold socio-economic stability.

Many MEs have substantial growth potential. With appropriate support, they can play a significant role in Bangladesh's transition from Least Developed Country (LDC) status to a developing nation. MEs can also help diversify the country's export base, which remains heavily dependent on the ready-made garment sector. Many MEs already contribute -- directly or indirectly -- to exports, highlighting their potential to reduce dependence on a single industry.

There is a national consensus on achieving inclusive, equitable economic development and sustainable poverty alleviation. Given their geographical spread, employment of low-income populations, and growth potential, MEs are vital to achieving these goals.

Finance gap: Despite their importance, many MEs remain excluded from essential financial and non-financial services. Even those receiving support often find it insufficient. Studies by institutions such as InM, the World Bank, IFC, and ESCAP indicate that inadequate access to capital remains the primary constraint on ME's growth and productivity. While loan disbursements to MEs are rising each year, demand is outpacing supply. ESCAP (2020) shows, MEs in Bangladesh face an average finance gap of 86% -- a figure that underscores the urgent need for new, innovative financing mechanisms.

Limitations of existing financial infrastructure: The current financial infrastructure of banks and financial institutions (FIs) is not well suited to meet the financing needs of geographically dispersed MEs. For banks and FIs, offering numerous small loans may not be financially viable. MFIs, while being the largest lenders to MEs, have limited funding capacity to meet growing demand.

PKSF has been supporting ME development across the country for over three decades through its POs. PKSF employs an effective appraisal and monitoring system, along with a robust MFI rating framework, to assess and mitigate risks -- enabling it to finance MFIs efficiently. Nevertheless, PKSF alone cannot bridge the massive financing gap.

Banks and FIs also finance many of PKSF's POs. As banks and FIs are not as specialized in MFI financing as PKSF, their reliance on financial statements and secondary data limits their ability to provide adequate financing. A strategic partnership between banks and PKSF could bridge this gap, reduce risk of the banks, and benefit all stakeholders, including MEs.

An innovative solution: In this context, PKSF has launched a pilot Credit Enhancement Scheme (CES), a risk-sharing process distinct from traditional credit guarantee schemes. CES addresses risk at multiple levels:

1. Credit guarantee: PKSF will directly bear a portion of the banks' credit risk arising from loan defaults by POs through providing credit guarantee.

2. Credit appraisal and certification: PKSF will appraise the creditworthiness of the POs and certify them to receive loans from banks, leveraging its comprehensive rating system.

3. Field-level monitoring: PKSF will also closely monitor the utilization of bank-financed loans under CES at the field level.

Many POs struggle to meet banks' collateral requirements, such as lien on fixed deposits or physical assets, limiting their ability to expand ME financing. CES will mitigate such constraints and improve access to bank financing, especially for small and geographically disadvantaged POs.

Banks often prefer to lend to large POs to reduce perceived risk. CES will help the banks for more equitable distribution of loans among POs of varying sizes and locations.

Impact and future outlook: The CES will act as a collaborative platform for PKSF, banks, and MFIs, working together to boost credit flow to MEs. By reducing institutional barriers and financial risks, CES will enable banks and FIs to scale up financing to MEs significantly.

The scheme is expected to:

1) Enhance financial inclusion

2) Support underprivileged and underserved MEs

3) Reduce income inequality

4) Accelerate inclusive and equitable economic development

By promoting ME growth, CES has the potential to transform Bangladesh's development landscape by boosting productivity, creating jobs, and helping the nation meet its long-term development goals.

Dr Mesbahuddin Ahmed is coordinator, MFCE Project, PKSF.

Email: mesbahpksf@gmail.com

© 2026 - All Rights with The Financial Express