Bangladesh's economic growth may stay stymied to 4.7 per cent in the current fiscal year for elevated inflationary pressure and delays in financial and fiscal reforms, and there's no better luck next.

The International Monetary Fund (IMF) has come up with such observations after a protracted spot assessment by its staff mission, and prescribed a slew of macro-level dos to avert looming financial and fiscal risks, including "sovereign debt distress".

Tight policies, weak investment amid financial-sector strains, election-related uncertainties, and higher US trade tariffs are expected to constrain the growth to 4.7 per cent in 2025-26, the Washington-based monetary observer said Saturday.

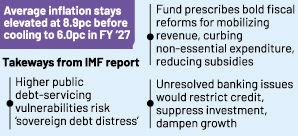

The IMF has cautioned that the unresolved banking issues would restrict credit, suppress investment and dampen growth.

It further warns about significant additional liquidity support to weak banks -- assumed to avert a loss of confidence.

This would "compress short-term interest rates, raise exchange -rate -risk premium and fuel capital outflows, triggering significant and rapid depreciation and inflation", said the IMF, following its Article-IV mission completed recently.

Delaying fiscal and banking reforms would dampen growth, raise inflation, and heighten macro-financial instability, the Fund alerts.

And the Gross Domestic Product (GDP) rate in the next fiscal year (FY2027) might not change as the inflation is likely to stay elevated above the target range in the near term and the downside risk stems from delays in the timely implementation of urgently needed financial and fiscal reforms.

Persistently weak revenue and large subsidies would squeeze public capital and social outlays, assuming the primary deficit path is maintained at the baseline path to protect debt sustainability, it also forecasts.

"The baseline scenario assumes that the authorities adopt critical and decisive measures to address interlinked fiscal and banking challenges. These include implementing tax revenue policies -- such as VAT reform and increasing the minimum turnover tax rate -- and cutting non-productive spending, alongside decisive action on the banking front to resolve and restructure weak banks."

About the banking sector, the Washington-based lender in its staff report says lower financial inflows -- including reduced multilateral disbursements -- would significantly limit foreign reserves accumulation.

Banks' significant undercapitalization would affect their capacity to absorb increases in government debt, contributing to higher public debt costs.

"Negative feedback loops, eroded monetary policy credibility and weaker external buffers would further elevate risks to inflation and the exchange rate, weighing on growth and macro-financial stability."

About inflation, the global monetary watchdog, which has provided Bangladesh with a tied lending package of $4.7 billion, says the annual average inflation is projected to remain elevated at 8.9 per cent in FY2026 before subsiding to around 6.0 per cent in FY2027, provided there is no premature policy easing or further supply-side disruptions.

The IMF statement says this policy package is necessary for Bangladesh to ensure macro-financial stability, bolster robust medium-term growth, and safeguard debt sustainability.

An alternative scenario illustrates the consequences of delayed or inadequate policy action in these areas.

The IMF has also cautioned Bangladesh on higher public debt-servicing vulnerabilities, saying that it would also raise the risk of "sovereign debt distress", underscoring the need for a subsequent tighter policy mix.

Delays in other reforms assumed under the baseline scenario, unsustainable increases in public expenditure and reversal of the exchange -rate reform would further heighten risks, the global lender says.

The inflation remains above the target and foreign reserves buffers have yet to fully recover earlier losses.

"Revenue-mobilisation efforts have so far failed to generate results while delays in subsidy reforms have constrained fiscal space," the IMF notes in the report.

Banking-sector vulnerabilities have worsened amid widespread undercapitalization.

The IMF offers some policy recommendations that include bold fiscal reforms for mobilizing revenue, curbing non-essential expenditure, and reducing subsidies.

Creating fiscal space is essential for development spending to sustain job-friendly growth and support the banking -sector cleanup, it also suggests.

The IMF report says banking -sector restructuring should be anchored in a credible strategy with assessment of system-wide undercapitalization, defined fiscal support, and legally robust resolution plans.

Delivering well-governed and solvent banks without reliance on regulatory forbearance is critical for addressing the near-term vulnerabilities and supporting financial stability.

The IMF asserts that maintaining tight monetary policy and consistently implementing the new exchange- rate regime are needed to address near-term macroeconomic vulnerabilities of high inflation and low foreign reserves.

It suggests comprehensive structural reforms to strengthen governance, enhance transparency, and promote export diversification are prerequisites for attracting FDI and ensuring inclusive development.

Legal and central bank-governance reforms should be aligned with best international practices.

Continued policy and reform efforts are essential to advance climate-resilient infrastructure, effectively manage fiscal and financial risks associated with climate-related events, and accelerate climate finance.

The IMF thinks credible restructuring of weak banks will restore confidence and ease credit constraints, while additional fiscal space will support social spending and public investment.

Sustaining reform momentum after the elections is essential for delivering inclusive and robust growth as Bangladesh prepares for LDC graduation, the Fund suggests.

© 2026 - All Rights with The Financial Express