Overnight cash rates have shot up on Bangladesh's interbank money market largely for expensive dollar buy by banks and cash holdback, amidst the ongoing global crunch.

Sources say the bank-to-bank lending rates have marked a steep rise by 31 per cent since last June and over 148 per cent since a year before in 2021.

Bankers say they faced difficulty in meeting urgent needs of cash in recent weeks as liquidity in the banking system was inadequate to meet the banks' funding needs.

At end of Thursday, the one-day interbank money rate was 5.78 per cent (weighted average), up by nearly 5.0 per cent in a month.

The bankers argue that this dearth is for a lack of adequate liquidity on the market. For this reason, banks borrow from other banks to meet their needs.

Call-money rate is the interest rate on overnight or short-term loans from one bank to another to meet urgent needs-and this is annualized rate.

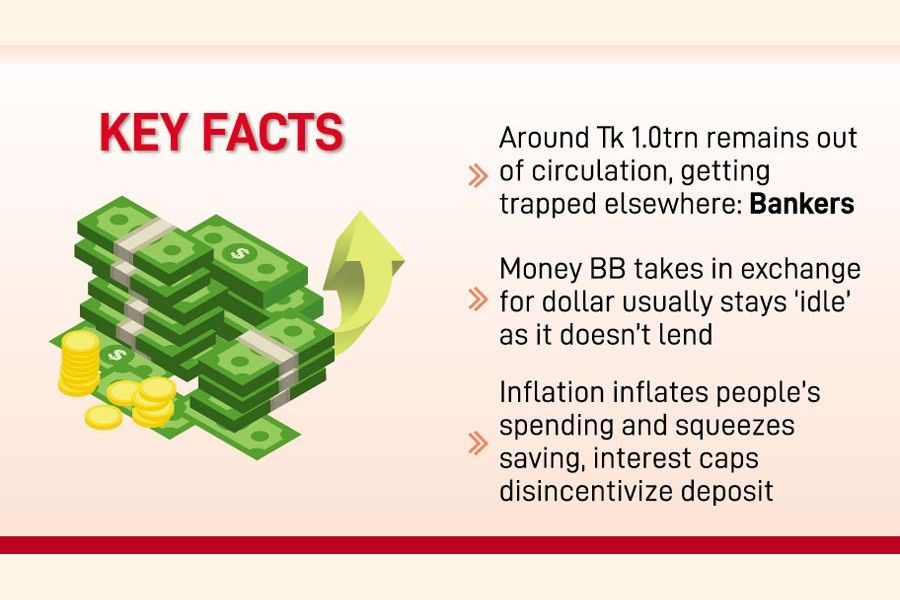

"To my mind, around Tk 1.0 trillion remained out of circulation," says Syed Mahbubur Rahman, Managing Director and CEO at a leading private-sector bank -- MTB.

He mentions a number of reasons behind the demand-supply mismatch. Inflationary pressure which forces people to spend money instead of saving, and market cap on both lending and deposits are among the factors.

"Those who have the cash are not becoming interested in deposit with the banking system," the leading banker says about the cascading impact of interest cap -- an interventional measure meant for taming incendiary inflation.

And many may convert their earnings to dollar which is the most stable currency in the world, and in hot demand amid war and sanctions.

Mr Rahman also points out that credit growth is higher than deposit growth, leading to the shortages.

Another banker told the FE that banks were buying the high-priced US dollar from the central bank to meet import-payment obligations.

"We're buying dollar from the central bank. So our liquidity shrinks fast," said Md. Shaheen Iqbal, a deputy managing director at the SME-focused-bank BRAC Bank.

This, on the other hand, is depleting the country's foreign-exchange reserves fast, as inflows have slowed. The reserves now stood at US$35.853, or down by more than 14 per cent since June last, according to Bangladesh Bank data.

However, there have been discussions about real reserves after investments, including in EDF.

He said when the central bank takes money in exchange for dollars that money usually remains idle as the Bangladesh Bank does not lend it.

"If the money remains idle, then it is one kind of money outside circulation," Mr Iqbal argues.

Liquidity surplus also comes down if the central bank raises banks' cash-reserve requirements. On September 30, Bangladesh Bank raised the repo rate, known as repurchase agreement in banking parlance, by 25 basis points for a second time in three months to put a brake on the expansionary monetary regime and hence contain inflation.

But, bankers argue, this is not the main reason.

The central bank has tightened its belt by deploying repo rate to deal with rising inflation, which hit nearly a double-digit zenith in September last.

Another banker, wishing anonymity, says many banks having adequate liquidity are not participating in the call-money market. They are either in favour of holding the cash or investing in risk-free treasury bonds.

The long-term treasury bonds' yield now has inched up to nearly 9.0 per cent and can be traded both on stock-exchange platforms and Bangladesh Bank's MI module.

jasimharoon@yahjoo.com

© 2026 - All Rights with The Financial Express