Commercial banks have changed strategy on foreign-currency management with its concentration on interbank swap and dollar-euro trades to avert shocks stemming from crawling- peg regime, thereby leaving the interbank forex market virtually derelict.

As part of the changing approach in using foreign currencies in a more sustainable way in this critical period of time, banks having good stock of foreign trading currencies, the American greenback in particular, are averse to going for outright transaction in dollar on the interbank spot market where the ceiling of taka- dollar exchange rate is capped at Tk 120 under the crawling-peg mechanism prescribed by the International Monetary Fund (IMF).

As the commercial banks continues sourcing dollars from remitters and exporters at rates higher than the official cap, they pass by spot market and largely trade their precious dollars through byways like interbank swapping and cross-currency transactions, specially dollar-euro transactions, where the crawling-peg-determined exchange rate is not applicable. They have invented such novel forex kerb market to ensure viable returns.

As a matter of fact, the interbank spot market looked almost derelict for months--causing a pain in the neck of both the IMF and the regulator, the central bank of Bangladesh.

Interbank currency swap is an arrangement where a bank lends foreign currencies to another for a short period of time with a provision of swapping back the same amount to the lending bank once the time is over. On the other hand, cross-currency exchange is a platform where local banks transact only foreign currencies with international banks.

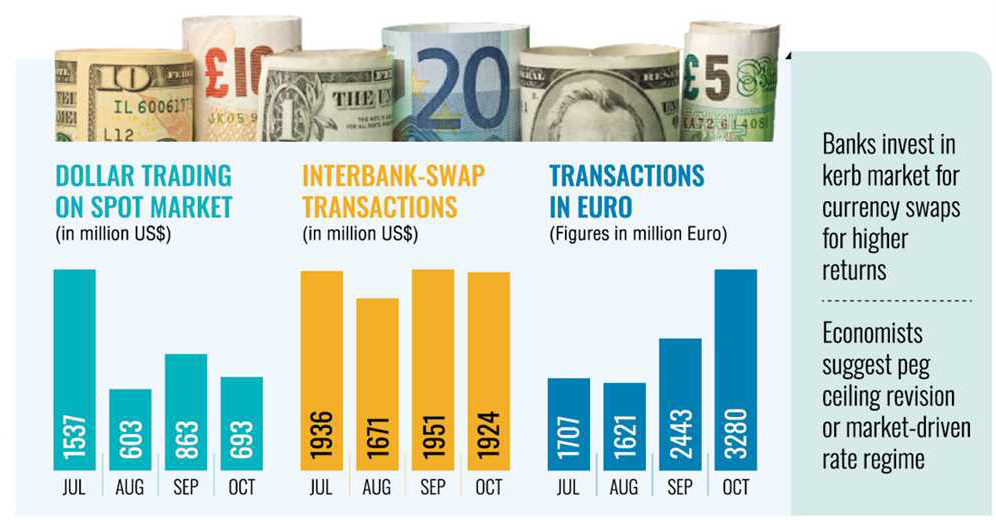

The changing foreign- currency-trading scenario in the banking industry is spotted in a month-long investigation by The Financial Express to find why the spot market lies dysfunctional in the crawling-peg period.

According to statistics collated from market players, banks made outright transactions of US dollars amounting to $1537 million on the spot market in July last. Afterwards, the volume dropped to $603 million in August before a slight upturn to $863 million in September. In October, the amount plummeted again to stand at $693 million.

The reverse course was observed in the interbank- swap transactions as $1,936 million (over 1.9 billion) of the monthly volume of dollar trade was recorded in July. The figures were $1671 million, $1951 million and $1924 million in August, September and October respectively.

In the cross-currency segment, euro becomes a lucrative option for the banks which purchased €1707 million in July last followed by € 1621 million, €2443 million and €3280 million in August, September and October respectively.

Seeking anonymity, an official at the Bangladesh Bank (BB), the central bank, said banks seemed not interested to trade dollars on the interbank spot market. Instead, they find swapping arrangement suitable for them.

"If we look at the data, dollar transactions at the spot market keep dropping significantly while the scenario was almost opposite in the swap transaction," says the central banker about the silent switch.

He mentions that the IMF representatives during their recent visit as part of its $4.70-billion-lending package pinpointed the matter on a note of concern. "If the spot market does not vibrate, we will not be able to get an equilibrium price that will help readjust the crawling-peg band," the official says about the downside risks of the market distortions.

The FE correspondent talked to a dozen bank executives, including managing directors and treasury officials, over the changing foreign-currency -management patterns. But all of them agreed sharing their thoughts on conditions of not disclosing their identity.

The treasury head of a leading private commercial bank said the central bank fixed maximum ceiling of exchange rate against the US dollar at Tk 120 under the crawling-peg-based exchange-rate mechanism.

But the banks have been sourcing the foreign currency from the remitters at more than Tk 121 per dollar.

Simultaneously, some of the exporters developed nexus with the importers and sold CM (contribution margin) portion of their export receivables to the importers that has prompted the banks to pay over Tk 120 to the exporters instead of Tk 119 a dollar.

"So, trading dollars on the spot market under the crawling-peg mechanism is not financially viable for the banks. That's why banks are concentrating more on dollar-euro transactions," the treasury official said.

Another treasury head of another private bank said the central bank officials, early last month, sat with the treasury heads of the commercial banks and verbally asked them to keep the dollar rate maximum at Tk 121 in case of purchasing euro.

But, the fact is banks have been buying the euro at the exchange rate as high as Tk 122 while officially reporting Tk 121 to the BB. After purchasing the euro-zone currency, the banks converted those to dollar again or sold to the local market at the market rate in -between Tk 130 and Tk 133.

"So, US dollar-euro transaction pays both ways to the banks. I think, the central bank should allow completely market-driven exchange rate to keep the spot market effectively vibrant," he said.

Chairman of the Policy Exchange of Bangladesh Dr M Masrur Reaz says the discrepancy between the crawling-peg upper ceiling and remittance-receiving rate needs to be revisited and adjusted accordingly.

The adjustment can be done in two ways: either upward adjustment of the crawling-peg upper ceiling or curtailing the official exchange rate the remitters used to get, he suggests.

But cutting down remittance rate may discourage the remitters and drive them to informal channel that could be a disaster for the economy under the prevailing macroeconomic situations, the economist says about the forex dilemmas.

"So, the BB can readjust the crawling-peg system with strong monitoring over interbank forex transactions," he says.

Former lead economist of World Bank's Dhaka office Dr Zahid Hussain also feels that the crawling peg is not working here because it does not crawl at all since its launch.

"As a matter of fact", the noted economist notes, "bankers have logically been finding alternative ways to make business because putting dollars in spot market under the existing crawling-peg system will not be viable for them."

He says the central bank is missing out the opportunity to leave the exchange rate onto the market at the moment when the forex supply riding on growing inflow of remittance is more than that of the demand because of economic slowdown in the post-uprising regime.

On the other hand, some 2.5 billion-3.0 billion US dollars are expected to come by the end of the fiscal from global lenders like the World Bank and the Asian Development Bank.

"I think the banking regulator can take the opportunity to go for market-centric exchange -rate regime," Mr Hussain suggests.

jubairfe1980@gmail.com

© 2026 - All Rights with The Financial Express