The central bank's liquidity-sterilisation instrument, called Bangladesh Bank (BB) bills, has failed to attract commercial banks' attention, leaving the regulator's move to mop up high-powered money in doubt, officials and bankers have said.

They said commercial banks mostly borrowed money from the central bank amid persistent liquidity tightness at policy rate (now 10 per cent) and invested in government securities - treasury bills and bonds.

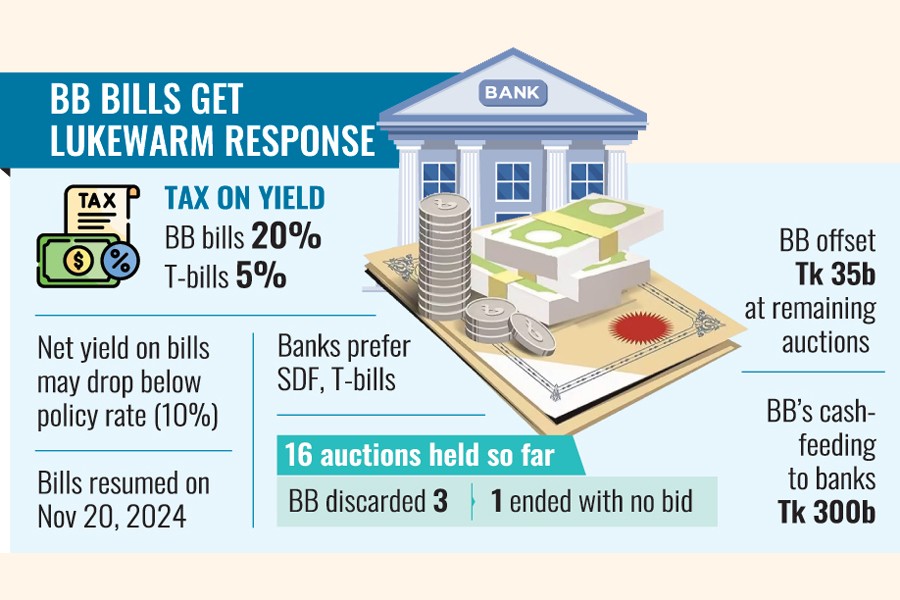

In fact, the banking regulator allows the cut-off yield on BB bills around that on 91-day treasury bills, which dropped substantially in recent weeks to reach 10.35 per cent after the latest auctions held on February 23.

As the BB bills are subject to much higher tax on yield compared to the short-term treasury bills, the net yield from investing in the former is likely to drop below the policy rate, discouraging banks to participate in the auctions for the instrument, according to market players.

BB sources said BB bills' last auction held on February 26 ended without a single bid by any commercial bank.

After a lapse of three years, the regulator restarted the operations of BB bills on November 20, 2024 in a bid to offset the cascading effects of high-powered money, which it recently injected to salvage some of the liquidity crisis-ridden commercial banks.

Such a splurge of printed money fuels inflation in the first place, creating consumer woes with price spirals, money market analysts said.

Since the resumption of BB bills, 16 auctions have taken place so far. Of those, BB discarded three because banks offered much higher yields while another one ended with no bid from any quarter.

In the remaining auctions, the central bank could only manage to offset liquidity amounting to around Tk 35 billion against its direct cash feeding, amounting to around Tk 300 billion, into some nine struggling banks over the last four months.

Central bankers, however, think the BB resumed the operations of such bills to offset inflation-fuelling high-powered money for three months.

It will take some time to mop up the fresh money as the overall liquidity situation of the money market is under stress.

Seeking anonymity, a BB official mentioned two major factors behind the slow response from banks regarding their participation in bill auctions. One is tax burden, and the difference between the cut-off yields in the auctions of 91-day government treasury and 30-day BB bills is not much.

The BB bills are a central bank instrument where banks will have to bear over 20 per cent tax on yield, while a treasury bill is a government instrument where the tax rate is only 5.0 per cent, according to the official.

"The tax differential is probably discouraging banks from participating in the bills," the central banker said.

On the other hand, the BB official said, banks need to surrender their funds for 30 days under the BB bills, although there is an existing overnight money-depositing option called standing deposit facility (SDF).

"So, instead of BB bills, banks are more interested in depositing their money in SDF. As SDF is an overnight instrument, banks can easily meet their credit urgency, if that arises," the official said.

Seeking anonymity, the treasury head of a public commercial bank termed the huge tax difference a major reason behind banks' lower participation in such auctions.

Under the existing liquidity tightness, he said, it would be tough for many banks to keep their surplus funds blocked for as long as 30 days.

"Instead of using BB bills, banks feel comfortable choosing other options like SDF and treasury bills. Commercial lenders can avail funds by keeping their treasury bill receipts as collateral."

Speaking on condition of not disclosing his identity, the treasury head of a private commercial bank said most banks used to invest in government securities and BB bills through their borrowed credit from the BB at policy rate. As the yield on BB bills now dropped to reach just over the policy rate in accordance with the gradual fall in 91-day treasury bills, the instrument is no longer lucrative for participants considering the market situation, he said.

"If BB really wants to make it lucrative for bidders, it needs to allow for expanding the cut-off yield on BB bills a little bit," he added.

jubairfe1980@gmail.com

© 2026 - All Rights with The Financial Express