SYFUL ISLAM and JASIM UDDIN HAROON | December 26, 2024 00:00:00

Billions worth of money in unsettled insurance claims has accumulated with the companies in flagrant default that invites government instructions for the regulator to heighten efforts to save people from deception, officials said.

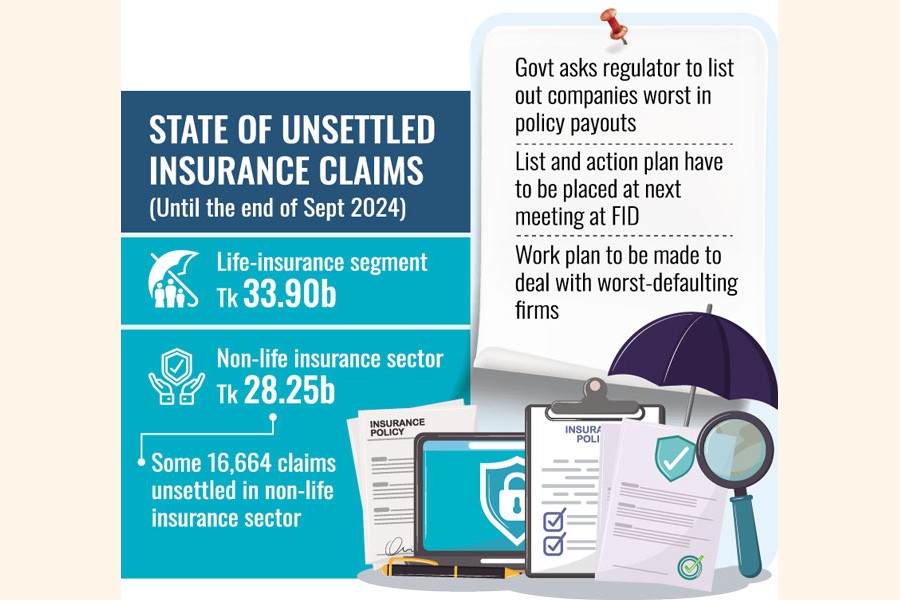

A total of Tk 62.15 billion has piled up in payment backlog over life-and non-life insurance claims with the insurers, as of end-September, which is seen as a testament to irregularities in the sector.

Now that straightening the financial sector started amid massive reforms kicked off by the post-uprising interim government, the Financial Institutions Division (FID) under the Ministry of Finance has also asked the Insurance Development and Regulatory Authority (IDRA) to inform it about what effective measures have been taken for expediting the settlement of piled-up insurance claims.

Moreover, the regulator has been asked to submit the numbers of insurance policies and of claim settlement at the next monthly meeting of the FID.

Officials said the IDRA has also been told to make a list of companies lagging behind in settling insurance claims and what work plan the regulator has to deal with those defaulting firms.

The list and the action plan, too, have to be submitted at the next meeting at the FID.

Data available with the IDRA show that at the end of September quarter, some Tk 33.90 billion worth of policyholders' claims remained on the backburner in life-insurance sector while non-life payout backlog came to Tk 28.25 billion.

In the non-life insurance sector, some 16,664 claims remained unsettled, according to the data.

Amid troublesome state of insurance-claim settlement, the insurance regulator last year had recommended for the government to take steps for liquidation of some insurance companies which have lost their financial abilities owing to massive irregularities and embezzlement of money.

These insurance companies even did not make further effort for improving their financial health, the regulator had said.

The IDRA had also suggested merger of some insurance companies to protect them from liquidation as their financial health continuously deteriorated, officials said.

The report had pointed out that the failure in payment of insurance claims by some companies cost the entire sector a lack of confidence of potential clients.

The government, however, did not go for liquidation or mergers of the said insurance companies though their finance health had not improved since then.

A senior official at the FID told the FE that the government did not go for their mergers or liquidation since hard-earned money of millions of the insured and also the job of thousands of people are involved with the companies.

"Liquidation or merger of a company is a complicated process and has involvement of huge amount of claim settlement," he said.

"We are trying to bring the companies under strict regulations so that the insured people get their money back and, at the same time, the companies can get back in good health," said the official about measured remedies.

Life-insurance business in Bangladesh experienced slower growth in its life fund during the last calendar year although there was a contraction in 2022.

According to Bangladesh Insurance Association (BIA), the life fund grew by 1.73 per cent in 2023 to Tk 321.53 billion, compared to a 3.6-percent contraction in 2022 when it stood at Tk 315.95 billion. In 2021, the life fund was Tk 327.48 billion.

An insurance company's life fund comprises a portfolio of investments funded by premiums collected from insurance policies.

This portfolio is used to pay out claims and typically includes government securities, bonds, cash, and other assets. The policyholders' benefits are directly linked to the performance of these investments.

Life funds generally grow sharply when investment returns are high.

Industry-insiders attribute the slower growth in 2023 to multiple factors, including higher claim settlement, lower premium earnings, and reduced investment returns.

Nasir Uddin Ahmed, President of the Bangladesh Insurance Association, a body representing private-sector insurance companies, explains: "The main reasons are poor growth in premiums, including renewal earnings, which have been struggling due to high inflation."

He adds that yields from investments in government securities increased in 2024, which will be reflected in next year's financial statements.

Life- insurance companies are required to invest 30 per cent of their earnings in government treasury bonds, considered risk-free instruments.

Describing the current period as challenging for the insurance industry, Mr. Ahmed says: "We hope the life fund will expand significantly as fixed-deposit receipt (FDR) and treasury yields are higher in 2024."

The industry people also highlighted that slower investment in areas such as real estate and the stock market contributed to the subdued growth of the life fund.

Under the existing regulations issued in 2019, life-insurance firms must invest at least 30 per cent of their funds in government securities.

Of the remaining 70 per cent, 10 per cent can be deposited with non-bank financial institutions (NBFIs), while up to 60 per cent of total assets can be invested as fixed deposits with scheduled banks.

Life insurers are allowed to invest 20 per cent of their assets in undisputed immovable properties located within city corporations and municipalities.

Despite the slow-paced growth in the life fund, total investments by private-sector life insurers increased to Tk 368.54 billion at the end of December 2023.

syful-islam@outlook.com, Jasimharoon@yahoo.com

© 2026 - All Rights with The Financial Express