The cost of funds in non-bank financial institutions (NBFIs) continues to grow, dealing a severe blow to their profit earnings, according to officials and market insiders.

These rising expenses in managing credits have made it difficult for NBFIs to make an immediate turnaround from the stress they have been experiencing since July of last year when deposit and lending ceilings were imposed.

As the cost of managing funds gradually increases, the profitability or NIM (net income margin) of the financial institutions continues to shrink to a level that industry players deem “not sustainable”.

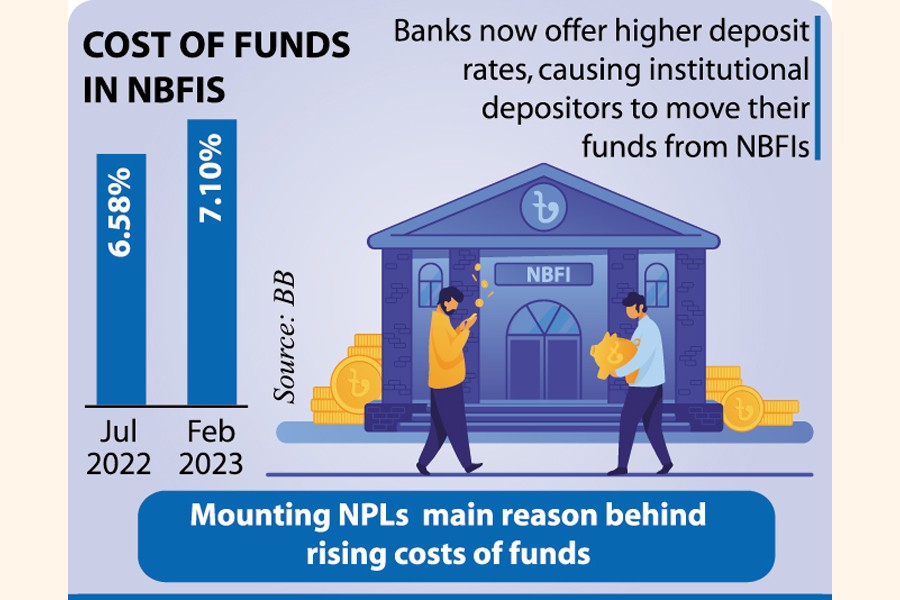

According to the Cost of Funds Index (CoFI) released by the Bangladesh Bank (BB), the weighted average cost of funds in July 2022 was 6.58 per cent, and it continued to rise, reaching 7.10 per cent in February 2023.

At the same time, the adjusted cost of credit also continued to grow, crossing 8.10 per cent in February 2023 from 7.55 per cent recorded in July last year.

Speaking on condition of anonymity, a Bangladesh Bank official said that the rate of profitability in NBFIs continues to decline due to the increasing expense in managing funds in recent months.

The official also noted that the cost of funds in NBFIs is rising mainly due to the mounting NPL (non-performing loan) buildups that have left them in their current state.

The official further said that there has been over a threefold rise in the aggregate volume of NPLs in nonbanks in less than seven years. The volume of classified loans or leases was 7.3 per cent in 2016, but it had edged up to 22.99 per cent until June 2022 when Tk 159.36 billion out of the total loans amounting to Tk 693.32 billion of the sector was classified as bad loans.

Market players said NBFIs normally offer higher deposit rates than banks, which generally encourages both institutional and individual depositors to choose financial institutions for their investments.

However, this situation has changed as banks are now offering higher rates following the withdrawal of the deposit floor rate several months ago. But for NBFIs, there is a deposit rate cap of 7.0 per cent imposed by the central bank since July last year.

Speaking on condition of anonymity, a top executive of an NBFI said that banks are now offering deposit rates as high as 8.0 per cent, which has caused many institutional depositors to withdraw their funds and move to banks for higher gains.

To remain in business under the current context, many NBFIs have started offering higher rates than the ceiling, which has raised their costs, he said.

“But there is a maximum lending cap of 11.0 per cent imposed by the BB from July 2022. So, the spread keeps shrinking, which is a matter of serious concern for the sector,” the executive added.

In light of these circumstances, he said, the NBFIs’ plan of action for an immediate turnaround from the current stress remains uncertain.

Irteza Ahmed Khan, managing director and CEO or Chief Operating Officer of Strategic Finance & Investments Limited (SFIL), said that the sector has been going through a tough time in recent months due to the existing caps.

He said the ceiling for both deposit and lending has put immense pressure on the survival of the sector, which has played a significant role in the country’s socioeconomic development over the years by ensuring easy access to formal credit.

“Look at the spread data in early last year, which was over 3.0 per cent, but now it has dropped to just over 1.0 per cent. Then how can we be sustainable?” he asked in a frustrated tone.

Mr Khan suggested that the existing caps need to be uncapped like the banks to give some breathing space for the NBFIs.

According to BB data, the spread was 3.04 per cent in January 2022. It dropped to 1.83 per cent when the deposit and lending caps were put into place. The spread has continued to drop and reached as low as 1.11 per cent in March last year.

jubairfe1980@gmail.com

© 2026 - All Rights with The Financial Express