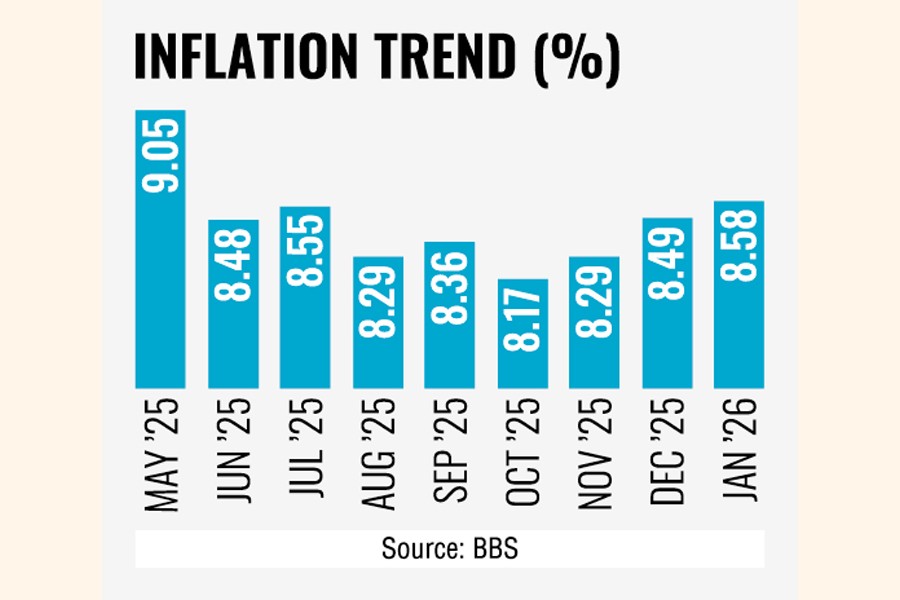

A daunting challenge left to the new government is stubborn inflation as its month-on-month rate has been on upturn over the last three months in defiance of the contractionary monetary-policy antidote, analysts say.

Despite applying a more-than-a year-long tight monetary policy under the immediate-past interim government, point-to-point inflation started swelling in November last after a small fall in October to 8.19 per cent.

Economists say curbing inflation would be one of the biggest challenges for the newly formed BNP-led government as the essential-commodity market stays heated-and offer effective remedies they think fit.

They think supply-chain management is one of the best options for the Tarique Rahman administration to contain the consumer price index (CPI) in a bid to give a relief to the people.

According to the official data, the point-to-point inflation has hovered around 8.5 to 9.5 per cent over the last one and a half years of the interim government, which has never slipped below 8.0-percent mark.

Despite a series of aggressive policy-rate hikes inherited from the interim period, the "8.0-percent club" remains a persistent reality, casting a shadow over the current administration's first 180-day recipe.

The latest data from Bangladesh Bureau of Statistics (BBS) reveal a worrying trend with non-food inflation showing a marginal decline to 8.81 per cent, the cost of living for the average citizen being driven upward by a sharp spike in food inflation, which rose to 8.29 per cent in January from 7.71 per cent.

Following the July 2024 uprising and the subsequent change in government, the Bangladesh Bank implemented its first policy-rate hike on August 26, 2024, raising the repo rate by 50 basis points to 9.00 per cent from 8.50 per cent to combat high inflation.

This was the first of several aggressive hikes, with subsequent increases raising the rate to 9.5 per cent in September and 10 per cent in October 2024.

The new cabinet, featuring Finance and Planning Minister Amir Khasru Mahmud Chowdhury and State Minister Zonayed Saki on the economic front, faces a "daunting landscape" of stagnant investment and shrinking fiscal capacity.

Economists warn that the transition of power has not yet cooled the market heat.

The central bank has maintained a contractionary monetary stance in a belt-tightening measure, holding the policy rate at 10 per cent.

Bangladesh Bank Governor Dr Ahsan H. Mansur stated that the tight grip would remain until inflation dips below 7.0-percent threshold.

On the ground, the reality is even harsher. In markets like Karwan Bazar commodity hub, prices of essentials like green chillies (Tk 240/kg), lemon (Tk25/piece) and broiler chickens (Tk 200/kg) continue to erode the purchasing power of low-income households.

The crisis is highlighted by the recovery of neighbouring peers. While Sri Lanka and Pakistan have managed to bring inflation down to low single digits, Bangladesh remains a regional outlier with the highest inflation in South Asia excepting its another South Asian peer, Pakistan.

Pakistan experiences high inflation of 9.64 per cent while India inflation has stabilised to a lower level, around 2.7 per cent to 3.65 per cent.

Sri Lanka writes an exquisite success story following an uprising-powered political changeover -the island nation knocked inflation down to 1.5 per cent in late 2025 from over 50 per cent in 2022 through policy tightening.

The Maldives and Bhutan are maintaining lower inflation rates at roughly 1.4 per cent and 2.04 per cent respectively.

According to the Centre for Policy Dialogue (CPD) and other analysts, the government is battling a multi-headed hydra of economic pressures. Persistent market manipulation by wholesale "syndicates" keeps prices high despite global commodity cooling.

Though the taka has stabilized near market-based rates, the "pass-through" effect of previous depreciations continues to inflate the cost of imported raw materials.

While the central bank is tightening money supply, the government's heavy reliance on bank borrowing to cover the budget deficit is creating a "crowding-out" effect, starving the private sector of credits.

Economists Masrur Reaz thinks actually the tight monitory policy does not work as the central bank has injected billions of takas in high-powered money into the market, which holds back taming down the inflation.

"On the one hand, the central bank has boosted the policy rate. On the other hand, it is injecting high-powered money. Then, how it's s a tight monitory policy?" he questions.

© 2026 - All Rights with The Financial Express