Exchange-rate depreciation and higher real interest rates have significantly contributed to the rise in non-performing loans (NPLs) in the banking sector, which stood at 32.26 per cent at the end of March, according to a study conducted by a local think-tank.

Stronger economic growth is believed to reduce default risks, according to the empirical study covering the period from 2015 to 2025 and conducted by the Centre for Policy Dialogue (CPD).

The study, titled "Effect of Macroeconomic Conditions on NPL: Findings of an Empirical Model", used quarterly data on Bangladesh's banking sector and applied Quantile Regression analysis developed by Koenker and Bassett (1982) to examine the relationship between key macroeconomic indicators and NPLs.

The study, titled "Effect of Macroeconomic Conditions on NPL: Findings of an Empirical Model", used quarterly data on Bangladesh's banking sector and applied Quantile Regression analysis developed by Koenker and Bassett (1982) to examine the relationship between key macroeconomic indicators and NPLs.

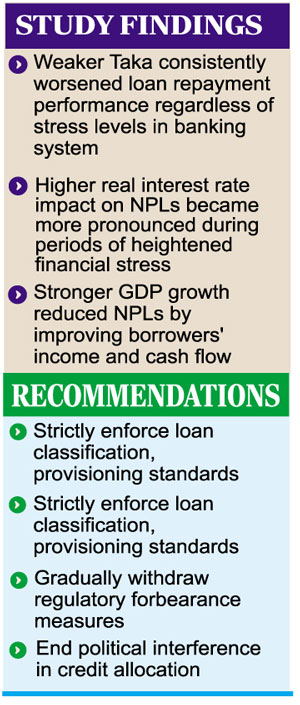

The findings showed that depreciation of the exchange rate increased NPLs across all quantiles, indicating that a weaker local Taka consistently worsened loan repayment performance regardless of stress levels in the banking system.

Higher real interest rates were also found to raise NPLs, with the impact becoming more pronounced during periods of heightened financial stress.

The CPD said increased borrowing costs weakened the repayment capacity of businesses and households, leading to a greater incidence of loan defaults.

In contrast, stronger GDP growth reduced NPLs by improving borrowers' income and cash flow, thereby supporting repayment capacity and enhancing overall credit quality.

The findings reinforce concerns over the vulnerability of the country's banking sector to adverse macroeconomic shocks and underscore the need for policy measures aimed at strengthening financial stability.

The CPD recommended a series of short- to long-term reforms to address the NPL problem and improve banking sector governance.

Among its recommendations, it called for the strict enforcement of loan classification and provisioning standards, the gradual withdrawal of regulatory forbearance measures, and an end to political interference in credit allocation.

To mitigate risks arising from external shocks, the think tank urged policymakers to maintain exchange rate stability and strengthen foreign exchange reserve management to safeguard borrowers' repayment capacity.

The CPD also stressed the importance of transparency, recommending the disclosure of actual NPL levels, including rescheduled and restructured loans, and improvements in the timeliness and quality of banking sector data to support evidence-based policymaking.

On prudential regulation, it proposed limiting repeated loan restructuring to curb moral hazard, reassessing relaxed single-borrower exposure limits, and strengthening oversight of large borrower concentration risks.

The organisation further called for the continuation of banking sector reforms, including enhanced supervisory oversight of non-compliant banks in line with Basel III standards, integrating non-bank financial institutions (NBFIs) into the broader financial resolution framework, and safeguarding the operational independence of the Bangladesh Bank.

The CPD mentioned that the consistently high NPLs reflected structural weaknesses rather than cyclical pressures.

It also mentioned that rescheduling, restructuring, and write-offs had masked the true extent of banking sector stress, adding that actual classified loans were higher than reported figures.

jasimhasroon@yahoo.com

© 2026 - All Rights with The Financial Express