An agenda to expedite human development

M. Fazlur Rahman | Thursday, 19 December 2013

System of credit and repayment of loan with interest was known in ancient times. Experts trace earliest concepts of support and protection, interest and premium from sources like Kautilya's Arthoshastro, Yajngavalkya's Dharmoshastro and Manu's Smriti - from the perspectives of a sub-continental discourse. Indeed some ideas of insurance may be traced to antiquity, in code of Hamurabi of Babylonian civilisation and from around the Mediterranean and in Abrahamic religious traditions, from Moses (A) to Muhammad (SA). Prophet Yusuf (A) dreamt drought and hunger would prevail for seven years. Then food minister of the Pharaoh, he built large storage of grains to feed the Egyptians during continuous drought of seven years which actually followed. He thus took adequate preparation to meet future risks beyond horizon and prevented deaths from hunger.

However much one may dig deep into layers of time, one finds only traces. We have known the science of probabilistic behavior of human life and the mathematics of chances from western scholarship. Ages have passed; and since European Renaissance, ideas have been relocated, reformed, redefined so much so that the human mind with genesis narrative often cracks open to accommodate new ideas and concepts. It is therefore useful to gather old signs and signatures in pleats of time and keep them in store for reference only.

The focus of this write-up is on Bangladesh and mostly on life insurance. In the formal sector, insurance was introduced by the colonial administration. The first insurance company was launched in 1818 in Calcutta. The first Act (Indian Life Assurance Companies Act) came in 1912 and the comprehensive modern law was enacted in 1938 which forms a rock basis of insurance industry.

Regulatory framework in Bangladesh

Following 1938 Act, one major policy change came through 1958 Insurance Rules. After independence, major highlights were: Bangladesh Insurance (Nationalisation) Order 1972, Insurance Corporation Act 1973, Insurance (Amendment) Ordinances 1984, Insurance Act 2010, and Insurance Development and Regulatory Act 2010. Prior to enactment of these modern laws, long time was wasted by series of committees from 1995 reports by Watson and Jenet to 2003 World Bank report of Craig Thorbon on proposed reforms of insurance industry. The Insurance Act 2005, the Insurance Regulatory Authority Act 2005, the Takaful Act, 2005 remained as drafts, till 2010. The Takaful Act is still pending as draft.

On policy framework, large scale centralisation was aimed at through P.O 95. This, however, did not register success. Afterwards decentralisation began in 1985, by amending the 1973 Act. The new Acts of 2010 are more up to date; these favour growth of private sector as well as facilitate harmonisation between private and public sectors. As the Insurance Development and Regulatory Authority (IDRA) gets functional, interests of policy holders are being served better; ethical norms are seen across the industry.

Fortunately our policy makers recognised the role of insurance for eradicating peoples' misery, minimising risk of business and mobilising internal resources. They noted the weak, outdated and underdeveloped state of insurance industry and took bold corrective steps to set right the ills and posit insurance on a solid growth path. Beside the Act of 2010, Rules and Regulations were framed and IDRA (Insurance Development and Regulatory Authority) was launched in 2011. As many as eleven more Rules and the Takaful Act are still in the pipeline.

Bangladesh economy

The World Development Report 2013 observes: "Some countries have done well in human development indicators and others have done well in economic growth but Bangladesh belongs to a rather small group of countries that have done well on both fronts."

In spite of severe impediments (like high interest rates, increased fuel and electricity prices poor infrastructure, volatile capital market and political turbulence) economists have noted our progress in several areas of MDGs as 'almost unbelievable'. GDP growth rate of 6 per cent over several years, in spite of the global economic downturn, Bangladesh has all the prospects to register higher growth figures; it may reach 8 per cent if political turbulence is minimised and the people get a respite.

Private sector non-life insurance has observed that productivity of Bangladeshi workers matches well with Chinese workers, in well managed firms, with five times lower wages. With a large population of young age group and population momentum continuing, Bangladesh will remain competitive in business and industry for a longer while. Thus insurance industry in Bangladesh has a big potential of growth. We are far below in reaching our full potential. We need to remove our constraints of low level of public awareness, lack of qualified professionals in the industry, centralisation of insurance industry in big cities while large periphery remain unserved.

Penetration and density

The two parameters, namely, insurance penetration and insurance density, are standard measures of insurance potential and performance. Insurance penetration is defined as the ratio of premium underwritten in a given year to Gross Domestic Product (GDP). Insurance density is defined as the ratio of premium underwritten in a given year divided by total population.

Globally, Bangladesh ranks at 86, Pakistan at 73, India at 19, China and South Korea at 5 and 9 position respectively. The United States, Germany, Japan and France are massively ahead. They are the four toppers. Bangladesh with a country total premium of 255 m USD carries 0.2 mark as insurance penetration (premium as per cent GDP) and insurance density of 2 (premium/per capita) USD.

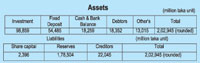

A look at the balance sheet of the JBC and 17 other life insurance companies for the year 2011 collected by the Bangladesh Insurance Association reveals the following:

It appears from these and details of revenue accounts that, for a number of small sized companies, the management expenses and agency commission outweigh net claims. On the other hand net premiums are quite hefty. On the whole, the management expenses are on the high side. While the figures definitely present a holistic picture for the professionals and experts, these leave out some vital information. Data from 1st SAARC Insurance Regulators Conference of April 2013 present prominently this opaqueness. Only Indian industry data, say it all. The Indian data show number of policies, number of employees, insurance penetration, insurance density and ranking in the world in terms of premium. Data of other countries do not show these vital figures. Bangladeshi data shows 0.2 per cent of GDP as insurance penetration, but does not speak of density.

After taking this journey through the insurance scenario one feels convinced that the industry has great potential for growth in Bangladesh. But unfortunately Bangladesh is not there yet. The legal reforms of last few years beginning in 2010 have generated good industry confidence to forge ahead. The country has now 17 life insurance companies in the private sector besides Jiban Bima Corporation (JBC) in the public sector. Together with life and non life, there are now 47 insurance companies. The business volume is miniscule compared with business volume of India. It is small even compared with that of Pakistan.

An opportunity frontier is now presented which may create scope to expand rapidly the life insurance industry in Bangladesh. This innovative modality is called Bancassuarance. It is defined as below:

"Bancassuarance is an agreement between a bank and an insurance company to sell life and general insurance products through bank's distribution channels. The key areas of sales, marketing, policy administration, claim management, customer service and renewals are as important in Bancassurance as they are in other insurance distribution models".

Briefly this is banc + assurance, where banks are selling insurance products. This term originated in 1980 in France and Spain. This is thus an alternative to "stand alone" insurance products bringing in concept of "add-ons to bank products."

In Asia emergence of Bancassurance is of recent origin. China opened this channel in 2000, Japan and Singapore followed in 2001; then came India and Korea in 2003. The ASEAN group is booming with Bancassurance. Even India of SAARC region is registering good progress. Unfortunately Bangladesh is not a player of Bancassurance yet. Mike Goodall, Regional VP of MetLife, Asia Pacific based in HK observed in the 1st SAARC Regulators Conference in Dhaka (April 2013), that this mode of insurance has rapidly expanded and by 2010, "the Bancassurance's share of new business premium ranged from around 35-70 per cent across Asia". On the supply side banks look for increase in their fee income; while those insurers lacking large agency force look for established distribution channels which banks may offer. On the demand side consumers have accepted banks as a credible channel of buying insurance products in the countries mentioned above.

Scope in Bangladesh

We have now 48 banks having more than 6700 branches covering whole of Bangladesh. Insurance companies, both life and non life, may enter into agreements with one bank or the other, to utilise the vast network of branches and offer their insurance products.

A similar, but not same, situation has yielded good results in the IT sector, where fiber optic line of Bangladesh Railway have provided connectivity to mobile phone companies to rapidly cover the whole country. In Bangladesh, banks sell tickets of cricket matches of World Cup. Can they not sell insurance policies?

Management costs of insurance will be dramatically reduced, and banks can increase their fee income. It is seen that major portion of non life insurance emanates from banking channels. Say, an LC is being negotiated either for import of machinery or for export of a finished product. Both the banking service and attendant insurance may be done from one platform or two side by side platforms.

There will be significant cost cutting for the entrepreneur by combining the services. Experts have opined that engaging banks as corporate agents for selling non life insurance product will be very attractive.

Programme in life insurance may be even more spectacular. We may consider the case of stipend programmes for both primary and secondary education. If 10 per cent of stipend money is given as premium of an educational insurance of a student and his/her parents are encouraged to make a matching contribution, (as a voluntary effort) then millions of insurance policies will be created.

A good number of companies will be needed to meet this expanded demand. Life insurance companies may be assigned to districts, as banks are assigned area wise to distribute stipend money. After graduating SSC/HSC level, when the policy matures, the student will have good amount of money at his/her disposal. This will be helpful to the student for admission to college/university. This suggested scheme will be a DPS + risk cover in cases of accident, needs of medicare and the like. Such a programme can be tested in a district or an upazila as an experiment. If successful, then companies will seek out their compatible partners and a development concert is likely to start off. A big synergistic action may thus be in waiting. For madrasa students 'Takaful' (Islamic insurance) mechanism to address similar insurance may be possible.

Youth movements like scouts, guides, young Red Crescent, Khelaghar and Kochikancha may be encouraged to enlist in such insurance programme. In the Philippines, Scout movement is so organised as to have for each scout an insurance policy on first admission. When s/he grows in to an adult, s/he gets the deposited money. Throughout the working of the policy s/he remains insured against unforeseen risks. Youth movements have mentionable strengths - Kochikancha (4,40,000), young Red Crescent (4,05,000), Kendriya Khelaghar (60,000), Scout (9,40,000); besides there is a good number of Girl Guides. Together, it is more than 2 million. Besides the stipend programme, there is an opportunity to work with youth movements mentioned above.

There are thus good grounds to be optimistic. A life insurance campaign as outlined above, can enthuse young people to engage in thrifty savings; can create massive awareness in the good values of insurance per se. Classical economics tell us, and this is yet to be refuted, that as savings grow, there will be an investment worthy surplus; when surplus grows, industrialisation gets a momentum.

CPD Research Director has observed that Bangladesh is facing 5 year cycle of political turbulence and this negates many of our stellar growth prospects. She has emphasised on investment. At present FDI flow is shy due to political turbulence. Local bank deposits often are eaten away by powerful and corrupt people. Hall Mark is an example.

A partnership between banks and insurance companies-Bancassurance might yield a win-win situation through proactive disciplined business practices. Medical insurance is another area which can bring in large benefits to the people. Thus through education and health insurances human development may be greatly expedited. Perhaps, a good insurance campaign may inculcate continuous practice of savings by bits from young age and can create and sustain attendant positive values.

We might experience better service, good discipline, good monitoring and strong auditing through expanded market of Bancassurance. These in effect will lessen economic crimes by degrees. We may visualise engagements which will be both creative and dynamic, between banks and insurance agencies. Will life insurance companies and banks now talk to each other?

The writer is a former secretary to the government of Bangladesh. He can be reached at rahman_mfazlur@yahoo.com