Wealth management in Bangladesh

An untapped opportunity

SM Samiuzzaman | Wednesday, 8 December 2021

Bangladesh has yet to launch any wealth- management company for individuals. The idea of wealth management lies with a one-stop solution for managing the personal finance of retail savers and investors. The idea is that one individual can reach a firm, and the firm can advise and eventually manage all the personal income and wealth of that person - such as buying insurance, arranging for a home loan, investing in the capital market etc.

Bangladesh has yet to launch any wealth- management company for individuals. The idea of wealth management lies with a one-stop solution for managing the personal finance of retail savers and investors. The idea is that one individual can reach a firm, and the firm can advise and eventually manage all the personal income and wealth of that person - such as buying insurance, arranging for a home loan, investing in the capital market etc.

While some leading banks and non-banking financial institutions offer customized wealth- management solutions for high-net-worth individuals, the industry is yet to launch any such service targeted to a broader set of clients.

The wealth-management industry in Bangladesh has yet to gain any momentum in managing money from individuals. However, the situation is gradually changing as more individuals are pondering on managing their wealth well. Naturally, personal wealth management is a relatively new concept in Bangladesh.

Amidst all the challenges, Bangladesh - as a country - has generated an unprecedented amount of wealth, particularly in the last decade. The GDP of Bangladesh is set to cross USD350 billion by the end of 2021 -- an impressive journey from the meagre USD6.0 billion in 1971, the inception of our country. With a 9.9-per cent growth target for the next decade as per government's Vision 2041, Bangladesh is set to generate even more wealth in this decade.

Furthermore, the distribution of wealth in this decade is likely to be fair. The world has been experiencing a historically high level of income- and wealth inequality since the global financial crisis of 2007, and Bangladesh has not been immune to this malady. Nonetheless, the middle-affluent population is expected to cross 45 million by 2030 from the current level of 27 million. The government of Bangladesh has set its target to bring the poverty level down to 0% from the current 20 per cent.

And finally, unsurprisingly, age is the biggest factor for personal wealth generation -- simply meaning the older one gets, the more wealth one accumulates. Given the median age is at 27.6, people of Bangladesh have on average 25 to 30 years to generate and accumulate wealth. The rise in middle-affluent-class population and falling poverty rates also indicate that the wealth is likely to be distributed among a larger number of people. Wealth-and income inequality will not go away in this decade but Bangladesh will continue moving in the right direction.

The idea of wealth management is closely related to investment decisions. People of Bangladesh have traditionally made most of their investments in real estate. The second- largest investment instrument is gold. More than 50 per cent of the Bangladesh population is still unbanked and yet to have access to financial assets such as FDR, deposit pension scheme, publicly listed equities, and mutual funds. One saving instrument that has been popular for the past decade is the national savings certificate.

Due to the low weighted average deposit rates, savers are more interested in investing in the high-return low-risk savings certificates issued by the government. In FY21, the government of Bangladesh sold Tk 419.50 billion worth of national savings certificates. However, the recent rate was cut by 50 bps to 10.5 per cent on savings certificates for an investment of more than BDT 1.5.0 million.

The unmatched level of wealth generated, coupled with a more even distribution, makes personal wealth management and ancillary services a crucial industry for the next ten years. Several meaningful traits will shape up the sector in this fresh decade and this article attempts to explain a handful of these traits in a meaningful way.

Rural inclusion will be the key driver to unlock the next wave in personal wealth management: Almost 65 per cent of deposits in Bangladesh are collected from Dhaka with another 15 per cent being collected from Chattogram - making the two metro cities the major deposit-collection points. The best financial institutions in Bangladesh, however, are striving to get more deposits, and targeting remote areas. A few factors have contributed and will continue to contribute in this case. First, several of the infrastructure projects, particularly megaprojects, are likely to be completed by 2024. Completion of these projects will boost the real economic activities in Bangladesh massively. New roads, bridges, and highways will connect the unconnected, and are likely to substantially increase their incomes. Furthermore, due to the density dividend in Bangladesh, the impact of the completion of such projects will be more prominent than that of other countries.

Second, the government of Bangladesh is focusing on decentralization so that the pressure on economic activities around Dhaka is mitigated. Spreading economic activities away from Dhaka with infrastructure projects will increase the income for people in marginal communities.

Wealth-management services have not been offered in Bangladesh because the market is not big enough. In this decade, with the rise in MAC population and the completion of infrastructure projects, both the breadth and scope of personal finance management will grow. New wealth-management firms can register or existing financial institutions can offer wealth management as a new service. Wealth-management firms can reach out to a larger group of customers in the next ten years.

A shift in how people think about money in Bangladesh is happening at this moment: Bangladesh is a country with low financial literacy. Several regulatory bodies in Bangladesh, particularly the Bangladesh Securities and Exchange Commission (BSEC), have taken several initiatives to increase financial literacy. Furthermore, access to the internet helps the Bangladesh populace to educate themselves on personal finance, and also on their investment decisions. A number of edutech and fintech startups are also working in this field, and these companies need to educate the people on their finances to grow the company business. The combined support from both the public and private sectors will make people more aware of their personal finance decisions. People will make educated decisions about managing their money and will seek assistance and advice from professionals. A more financially literate client base will create business opportunities for wealth-management firms in Bangladesh.

Another factor is that the household debt-to- GDP ratio in Bangladesh is one of the lowest in the world. People in Bangladesh are generally risk-averse and do not fully appreciate the idea of credit. While mortgage and consumer loans are gaining popularity in Bangladesh, the portfolio is still much lower than that in the neighboring countries. People in Bangladesh typically build up equity to make a large investment, such as buying their first house. However, this situation is likely to change. Young people in Bangladesh are more prone to consumption compared to the earlier generation. The young workforce will appreciate the role of credit in their life and take personal loans to avail themselves of a better lifestyle. One can make the case that Bangladesh is very conservative about credit at all levels, evident by the country's lowest debt- GDP ratio among its South Asian peers. A better appreciation for credit as well as improved financial literacy will create a demand for personal wealth-management services in Bangladesh.

Mobile financial services and digital banking channels will support customers in accessing wealth-management services: Bangladesh has more mobile sim connections than bank accounts. With the government vision of Digital Bangladesh, the people have embraced digital services and adapted to a digital lifestyle. Especially in the case of mobile financial services, users had whole-heartedly adopted these services for a lack of proper finance infrastructure. With 41.1 million active MFS users (as of July 2021), Bangladesh is the fastest-growing MFS market in the world. The MFS sector in Bangladesh will be growing rapidly, and both foreign and local companies are investing heavily to grab a slice of the market cake.

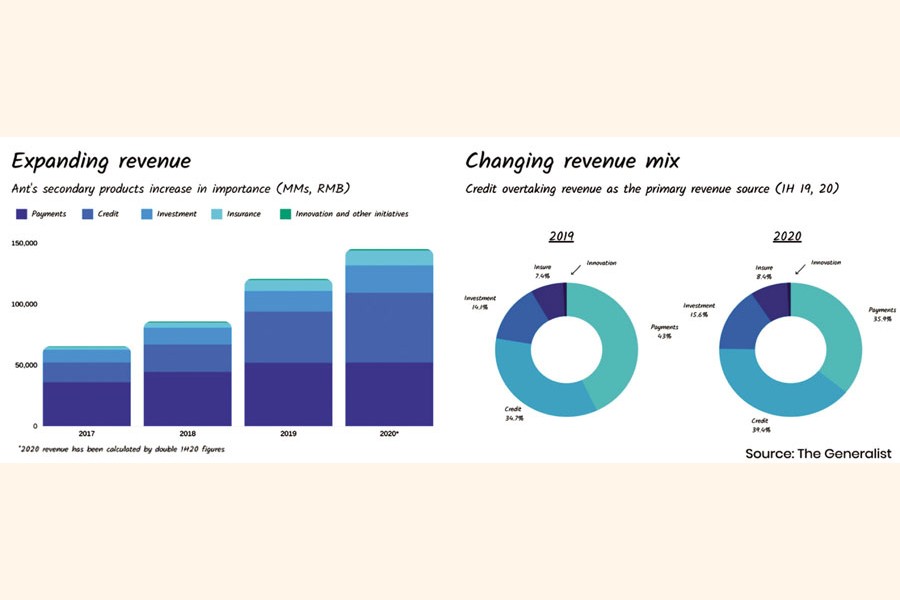

In case we follow the MFS industry in other countries, almost all the MFS companies offer wealth-management-and investment- management services. Wealth management and investment revenue for Alipay, one of the two leading MFS providers in China, was more than 15 per cent in the first half of 2020. The MFS industry in Bangladesh will inevitably follow a similar path. All the MFS players are looking forward to launching new products and wealth management is uncharted territory. Distribution is a key issue in launching wealth- management services but that value-chain issue can be easily resolved with technology. MFS providers will play a key role in launching and popularizing wealth-management services in Bangladesh.

The mass populace in Bangladesh has yet to think about their income and wealth in an educated way. The very few people who did think about managing their money did not have any professional help. Wealth management, as an industry, is ready to be launched in Bangladesh. The financial institutions in Bangladesh with the best brand values will launch wealth-management services, and the industry will also welcome a few new players solely focused on wealth management. Personal wealth and investment management should be one of the highest priorities for any individual, and it is high time the people in Bangladesh received some professional help here.

The author is working as a Portfolio Manager at UCB Asset Management Limited. He can be reached at Sm.samiuzzaman@ucb.com.bd