Auditors flag financial breaches at non-life insurers

FE REPORT | Wednesday, 3 June 2026

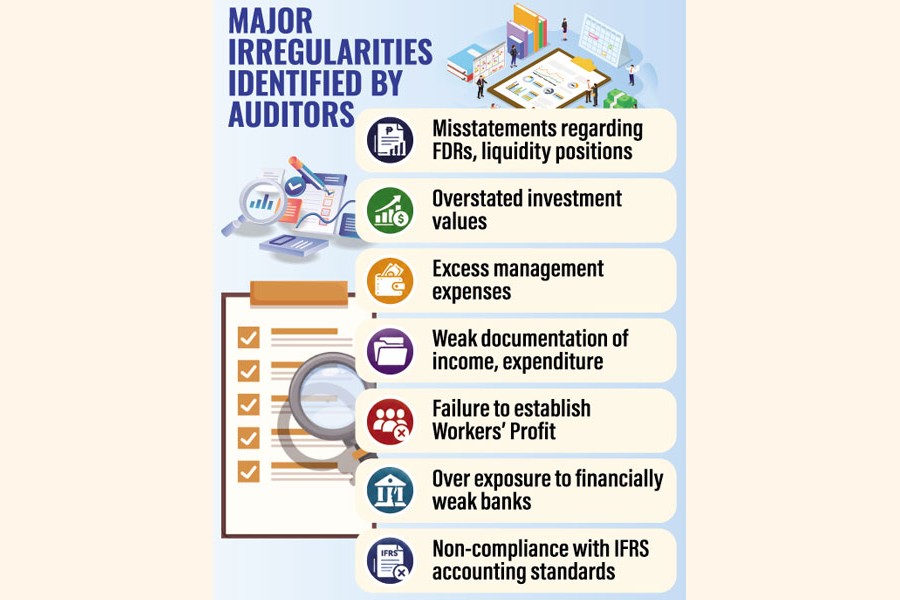

Auditors have exposed a series of financial reporting irregularities, regulatory breaches, and governance weaknesses at several listed general insurers, raising fresh concerns over transparency and compliance standards in the country's insurance sector.

They revealed issues ranging from potentially impaired bank deposits and overstated investment values to excessive management expenses, unverified balances, and non-compliance with international accounting standards.

The audit observations, involving at least 18 listed insurance companies and their 2025 financial statements, were published on Tuesday.

The audit reports cover non-life insurers, including Eastern Insurance, Bangladesh General Insurance, Central Insurance, Phoenix Insurance, Dhaka Insurance, Union Insurance, and Standard Insurance.

One of the most critical issues identified across multiple audit reports is the inability to independently verify significant portions of cash and fixed deposit receipts (FDRs) held by insurers.

Auditors also raised concerns over exposure to financially stressed or weak banks without adequate impairment provisions, suggesting a potential overstatement of asset values and an underestimation of credit risk.

For example, Eastern Insurance received a qualified audit opinion, under which its auditor could not independently verify fixed deposits worth Tk 1.20 billion held in 46 banks, representing 98 per cent of the company's cash and cash equivalents and nearly half of its total assets.

The auditor also identified investments amounting to Tk 263.94 million in five financially distressed banks and noted that no impairment provisions had been made despite uncertainty regarding recoverability. In addition, the company recognised Tk 15.85 million in interest income from those banks, even though collection of the amount appeared uncertain.

Eastern Insurance was also accused of improperly accounting for an unrealised stock market loss of Tk 98.94 million and maintaining significant discrepancies in its investment records. Auditors further reported an inability to verify claim liabilities, premium income figures, gratuity obligations, and several major asset balances due to insufficient documentation.

Bangladesh General Insurance, another major insurer, also received a qualified opinion. Its auditors found that management expenses exceeded regulatory limits by Tk 70.71 million.

The insurer spent Tk 356.02 million, whereas the Non-life Insurance Rules, 2018, set the maximum management expense at Tk 285.31 million, equivalent to 35 per cent of gross premium income.

Auditors reported that receivables worth Tk 444.56 million and payables amounting to Tk 6.65 million could not be independently confirmed.

Concerns were also raised regarding unrecognised gratuity liabilities, the absence of an actuarial valuation, failure to establish a Workers' Profit Participation Fund (WPPF), and potential impairment risks relating to deposits held with financially stressed institutions.

Islami Commercial Insurance-another insurer-escaped a modified audit opinion but faced extensive scrutiny through emphasis-of-matter and other-matter paragraphs.

The auditor found that the insurer overstated the value of its quoted share investments by Tk 98.16 million by carrying securities at cost rather than fair market value, contrary to IFRS 9 requirements.

Islami Commercial Insurance's management expenses also exceeded the regulatory ceiling by Tk 225.11 million, while receivables from other insurers totalling Tk 311.98 million remained unverified.

The audit report also questioned the treatment of tax provisions and advance tax balances exceeding Tk 225 million and noted that the company has yet to implement IFRS 17, the latest global accounting standard for insurance contracts.

The auditor of Asia Pacific General Insurance issued a qualified opinion on the company's 2025 financial statements, citing non-compliance with international accounting standards for lease arrangements.

The audit report also disclosed that the company's management expenses reached Tk 312.51 million in 2025, exceeding the regulatory ceiling by Tk 39.22 million. However, management is reportedly in the process of providing explanations and necessary clarifications regarding the excess expenditure.

A common theme across the audit reports was the difficulty auditors faced in obtaining independent confirmations for bank deposits, insurance receivables, and other material account balances.

The findings come at a time when regulators are seeking to strengthen governance, risk management, and financial reporting practices across the insurance sector.

In the 2024 financial statements, auditors of some 27 listed insurers also raised concerns over transparency and compliance standards in the insurance sector.

Market analysts say the repeated audit observations suggest weaknesses in internal controls and compliance culture among some insurers, potentially exposing shareholders to heightened financial and operational risks.

They noted that while audit qualifications and emphasis-of-matter paragraphs do not necessarily imply fraud or immediate financial distress, the issues highlighted warrant close attention from regulators, investors, and company boards.

Abul Kalam, spokesperson for the Bangladesh Securities and Exchange Commission (BSEC), said the commission will formally request the Insurance Development and Regulatory Authority to take regulatory measures against the identified companies in accordance with applicable laws and regulations.

Currently, 82 insurance companies operate in Bangladesh. Of them, 58 insurers, both life and non-life, are listed on the stock market.

babulfexpress@gmail.com