Bangladesh: a breakout economy or another LDC crash landing?

Zaved Akhtar | Wednesday, 5 June 2024

What Bangladesh achieved in the last five decades, more so over the last 30 years or so, has been more than impressive. We have been stepping up our gross domestic product (GDP) growth rates every decade consistently since the independence, culminating to 6-7 per cent pre-pandemic. If we take the first 50 years since independence, we have seen massive acceleration in the last 30 years with GDP doubling every 10 years, an unmatchable feat for any least developing country (LDC). During the period, Bangladesh has also seen strong acceleration of the Human Development Index (HDI), well ahead of India, Pakistan, and Nepal (albeit lower than Sri Lanka, Maldives & Bhutan) and is currently placed as Medium Human Development Category. In this connection, a quote from The World Bank Country Economic Memorandum, Change of Fabric, may be relevant. Regarding the reforms, it states: “In the mid-1980s, markets and public investment were strengthened, including for infrastructure. Further reforms in the early 1990s allowed for more private sector participation in trade, finance, and land ownership. These reforms were accompanied by complementary reforms in agriculture ((e.g., liberalization of agricultural input markets, seed sector reforms), and in social sectors (e.g., mandatory primary school, a female stipend program for secondary schools, and family planning programs). The rise of ready-made garments exports during that period evolved from a combination of private investment and public policy support. Structural improvements provided strong impetus to inclusive growth especially between the early 1990s and mid-2000s but major reforms have not been sustained since then. Bangladesh has yet to move to the next phase of economic transformation.”

DRIVING THE ECONOMY TO THE NEXT PHASE: Fundamental drivers for the economic growth for Bangladesh are readymade garments, remittance, and agriculture. These are facilitated by consumption on  the demand side while trade investments and government investments on the supply side of the economy. For us to unlock the economic growth potential we will need the current growth drivers to move up the value chain (diversification of RMG portfolio, move to more white-collar manpower exports, and agriculture-mix tilting to cash crop while improving yield). So we need to ensure that the private investment is encouraged and government spending is focused on investment behind health, education, and infrastructure, specifically in rural areas. Private spending also needs to focus on investing behind businesses that have ESG (Environment, Sustainability and Governance) at their core while secure investment behind SDG-investment sectors – notably in renewable energy, given the rising price of energy and greater need for energy security.

the demand side while trade investments and government investments on the supply side of the economy. For us to unlock the economic growth potential we will need the current growth drivers to move up the value chain (diversification of RMG portfolio, move to more white-collar manpower exports, and agriculture-mix tilting to cash crop while improving yield). So we need to ensure that the private investment is encouraged and government spending is focused on investment behind health, education, and infrastructure, specifically in rural areas. Private spending also needs to focus on investing behind businesses that have ESG (Environment, Sustainability and Governance) at their core while secure investment behind SDG-investment sectors – notably in renewable energy, given the rising price of energy and greater need for energy security.

However, amidst current economic headwinds, we will need to do more and will require some fundamental structural reforms especially given that higher GDP growth in the last decade has not translated to faster poverty reduction as in the preceding past two decades, indicating the current episode of high growth has not been as inclusive as before. We also need to remove protection as average tariff rate on intermediate goods in Bangladesh is 18.8 per cent, which is more than double the rate in China (7.4 per cent) and almost double the rate in Thailand and Vietnam (9.6 per cent). Average tariffs, or nominal protection rate, more than double (29 per cent) if para-tariffs are included, making Bangladesh an outlier among countries with a similar income level. MFN tariffs would need to be cut by almost 50 per cent (from 14.7 per cent to 9.6 per cent) and all other import taxes eliminated (14.1 per cent to zero) for Bangladesh to reach similar levels of taxation on intermediate goods as those prevalent in East Asian comparators.

CALL FOR THE BOLD AND DARING REFORMS: Time has come for us to bring in some bold and daring structural reforms. We owe it to the next generation as we have benefitted from the reforms done by our predecessors. Some of the reforms are already in flight as the currency is being adjusted to reflect the right value and moving to market-based interest rates while policy rates are being adjusted upwards. These moves will bring in some short-term challenges for businesses, especially cash starved Small and Medium Enterprises (SMEs), but it is a move in the right direction as it will help in stabilising the economy. While these three reforms are in flight, economic hardships will mean that three more critical challenges need to be fixed as we get into the next financial year. These are: (a) Stickiness of inflation, (b) fiscal deficit, and (c) stressed financial institutions due to non-performing and distressed loans. To address these, we need to continue: (a) the contractionary monetary policy; (b) reduce non-tariff barriers (NYTBs) and indirect taxes by putting more focus on direct taxation and reduction of effective corporate tax rate which has been driven up by inadmissibility of legitimate business expenditures; (c) simplify VAT and indirect taxation while building an integrated digital architecture for digitisation of customs, tax, and VAT; (d) reform the financial institutions and improve the capabilities by eradicating distressed and stressed assets. FOREIGN DIRECT INVESTMENT, A LEVER UNDERUTILISED: Another lever that has remained significantly under leveraged, is Foreign Direct Investment (FDI). We have been significantly below the fair share, whether we are comparing against global benchmarks or be it South Asia. We must ensure that we build Bangladesh as a preferred destination for investment.

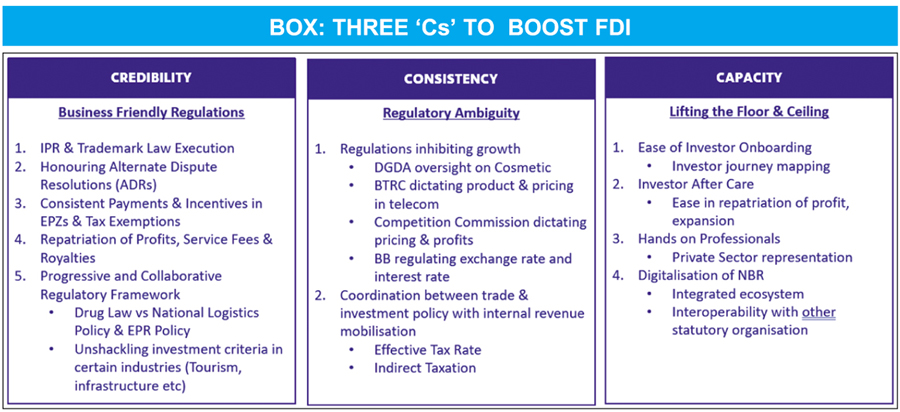

From FICCI’s perspective we need to see these from a lens of 3-Cs: (a) Credibility, i.e., seen as a trustworthy partner for investment; (b) Consistency, ensuring that policies are steadfast, and no sudden changes are being made; and (c) Capacity where we need to lift the floor and ceiling of our human capital. Specific actions for each of the pillars are illustrated above (BOX).

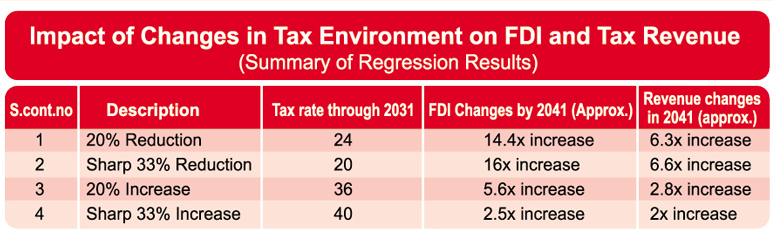

TAX REFORMS, FIRST PORT OF CALL: Predictability and planning of future tax rates are fundamental components of any long-term business planning, especially for the foreign investment. To improve tax predictability and facilitate effective tax planning, it is essential to implement tax rates on a forward-looking basis. This approach ensures that taxpayers are informed in advance about the tax rates applicable for the current fiscal year and beyond. Such clarity provides individuals and businesses with the assurance and stability needed to make well-informed financial decisions. It removes the unpredictability linked to a sudden or retroactive tax rate changes. A forward-looking tax system upholds principles of fairness, allowing taxpayers to organise their financial affairs appropriately. It also promotes compliance, as taxpayers are more likely to fulfil their obligations when they can accurately anticipate their tax responsibilities.

Moreover, few provisions in the current tax regime are creating unfair tax burden on business. Such rules are adversely impacting the growth of investment and FDI in Bangladesh. This can be best illustrated how treating disregarded expenses under Section 55 as separate taxable income, imposes an unjust additional tax liability on businesses, thereby raising their operational costs.

The issue at hand involves Section 56 of the ITA 2023, which classifies disregarded expenses under Section 55 as taxable income at standard rates. This practice creates an additional tax burden for businesses, deemed unfair and unreasonable, as it significantly increases the cost of doing business in Bangladesh. This is particularly problematic because it undermines efforts to cultivate a business-friendly environment. Under Section 56, even businesses operating at a loss must pay tax on disregarded expenses, which exacerbates their financial difficulties, especially during tough economic times. Moreover, the taxes considered as deducted/collected and minimum tax under Section 163 cannot be carried forward or refunded, further complicating the tax framework. Reforming such unfavourable rules is crucial to lessen the financial burden on businesses, which will in turn stimulate investment, and foster a more supportive business climate in Bangladesh.

CONCLUSION: There is more to what meets the eyes. Time is of essence, and we need to act fast to make a positive intervention to set the course right through reforms. We must make sure that we don’t get myopic by the immediate headwinds as this doesn’t do justice to the long-term potential of Bangladesh and its economy. We need to take bold actions, face the short-term consequence for the long-term sustenance of Bangladesh. Should we get some of these reforms going, we are likely to bend the curve and make this a 1$Trillion economy in no time.

Zaved Akhtar is President, Foreign Investors’ Chamber of Commerce and Industry (FICCI); ed@ficci.org.bd. He is also Chairman & Managing Director, Unilever Bangladesh.