Bangladesh scenario: Bubbles and busts

Mirza Azizul Islam | Thursday, 26 June 2014

Bangladesh stock market has a chequered history. Dhaka Stock Exchange (DSE) started its journey as an incorporated body in 1954. However, formal trading began in 1956. Trading remained suspended during the 1971-1976 period because of the liberation war and the socialist policy stance of the immediate post-liberation government and resumed in 1976 (Rayhan et al, 2011).

There was a big bubble in 1996 followed by a catastrophic crash. Dhaka Stock Exchange (DSE) index jumped from 957 on November 02, 1996 to a record high of 3649 on November 05, 1996. The index continued a downhill march thereafter with the lowest level record on at 463 on May 03, 1999. Since then the market remained in a state of doldrums. It started on a path of resurgence from 2003 (Islam, 2005).

The stock markets of Bangladesh witnessed another bout of wild crash in 2010. The general index of DSE stood at 4535 at the end of December 2009, nearly doubled in less than a year to 8912 on December 05, 2010, suffered drastic loss of more than 1200 points over a period of two days to dip to 6499 one day in January 2011 and then regained more than 500 points on the next day of the month to reach 7512 following some policy pronouncements by Securities and Exchange Commission (SEC) and the Bangladesh bank. The index was 7378 on January 17, 2011. The downward march continued thereafter. As of now, index seems to have reached unjustifiably low level equalizer at around 4500.

THE UNDERLYING CAUSES

There are certain inherent characteristics of the financial markets which expose them to wide volatility. Those include asymmetry of information, adverse selection, herd behavior by investors and moral hazard. These factors appear to have afflicted our stock markets with vengeance in recent times.

"Asymmetry of information" in the context of stock markets implies that the investors know much less about the inherent worth of the companies shares of which they are buying/selling compared to managers and sponsors of those companies. Investors' decisions, therefore, may not be based on rational considerations, perhaps even more importantly incapacity or unwillingness to process available information has contributed to large swings. The investors have not taken into consideration well-known criteria such as net asset value per share and/or price-earnings ratio in their decisions even though information regarding these criteria is readily available on the websites of stock exchanges. As a result, all share prices rose or fell more or less in unison irrespective of differences in fundamentals. This is also a reflection of "herd behaviour" in the sense that when some investors started buying/selling some shares, others joined in droves to follow suit without discriminating among shares on the basis of their intrinsic worth. The number of Beneficiary Owner (BO) account holders skyrocketed to 3.3 million, many of them have been allured into the stock market by brokers who opened many branches outside the major cities. Most of these new investors from outlying districts have hardly any knowledge about the basic principles that should guide decisions regarding investment in stock markets. It is regrettable that even institutional investors behaved in a herd-like manner. Both irrational exuberance and irrational pessimism became pervasive.

"Adverse selection" also came into play to cause instability. The banks as well as non-bank financial institutions generously provided credit to investors in stocks (which are inherently high-risk, but potentially high-yielding investments) who probably offered to pay higher interest, depriving investors in real sectors of the economy. In addition, the banks themselves invested in stocks and there was diversion of funds ostensibly borrowed for industrial term credit or working capital into the stock market. Subsequently sale pressure gathered momentum as the investors began to realise that the indices reached unsustainable levels. This scenario brought into question the effectiveness of monitoring and supervisory role of Bangladesh Bank.

"Moral hazard" implies that regulators would rescue the investors though their losses were the consequences of irrational investment decisions. This perception encourages assumption of high risk. In the context of our stock markets, moral hazard has been reflected in changes in policy stance by Bangladesh Bank with regard to exposure of banks to stock markets, frequent changes by the Securities and Exchange Commission (SEC) in respect of loan margin ratio and the methods of calculating the ratio. Moral hazard seems to have become entrenched especially because regulatory authorities have often relaxed their standards in response to destructive activities of a limited number of disgruntled investors.

In addition to the above factors, market manipulation has also been cited a cause of instability. This is an issue which was investigated by a probe committee headed by Mr Ibrahim Khaled. The report submitted by the committee in 2011 cited market manipulation.

THE STATE OF DEVELOPMENT

Apart from wild booms and busts followed by prolonged stagnation, the stock market of Bangladesh is characterised by a poor state of development. As noted before, among the criteria for assessing the state of development of a country's stock market are the number of companies listed, market capitalisation as proportion of GDP (gross domestic product), turnover ratio and market liquidity.

The number of companies listed in Bangladesh is similar to that of Nepal. But the size of Nepal's GDP is less than one-fifth of Bangladesh. Among the ten Asian countries as of 2012, Bangladesh had the lowest market capitalisation as proportion of GDP. However, it ranked second in terms of turnover ratio and fifth in terms of market liquidity.

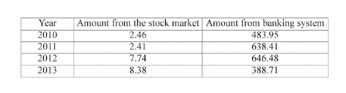

The stock market of Bangladesh has also been very ineffective in playing the role of intermediary between savers and investors in the real sector. This is reflected in the fact that the fund raised from the initial public offers on the capital market is insignificant compared to the fund raised through loans and advances. The relevant numbers are presented in Table 5.

In the light of above analysis, it is obvious that the stock market of Bangladesh remains in a state of underdevelopment. In the wake of dramatic crash of December 2010, SEC announced a market rejuvenation package. Some of the measures contained in the package have been implemented. Notable among these are the installation of surveillance software in SEC, demutualisation of exchanges and establishment of an investment fund to give relief to small investors who suffered heavily in consequence of the crash. Nonetheless, as noted earlier, the market has not turned around on a sustainable basis.

THE PATH TO BETTER FUTURE

Many analysts have suggested a variety of measures that need to be implemented to reinvigorate the stock makets of Bangladesh. The suggestions that are considered to be of seminal importance are highlighted below.

Increase in the number of scrips: There was an explosion of market capitalisation on the basis of price inflation of existing scrips. There were not many new issues of Initial Public Offering (IPO) of significant size over the last few years from the private sector with the notable exception of Grameen Phone. The promised off-loading of shares of 26 state-owned enterprises has not materialised. A large number of shares issued by companies from different sectors would help bring about better balance between demand and supply and enable investors to pick and choose on the basis of fundamentals rather than zooming on a limited number of existing shares, thus excessively inflating their prices and creating conditions for eventual downslide. Furthermore, adverse impact of manipulation by any errant market actor with respect to a few shares would be minimised. In order to ensure stability in the future, depth of the market needs to be increased by bringing in more IPOs.

Coordinated role of regulators: Bangladesh Bank and SEC should regularly exchange notes and adopt policies with due regard to interactions between money market and capital market. Policies, once adopted on the basis of mutual consolations between the two regulatory authorities as well as between them and other stakeholders, should be implemented rigorously without being subservient to extraneous influences and should not be changed frequently.

Investor's education: The coverage of existing investor's education programmes conducted by the stock exchanges and SEC is limited. These programmes need to be expanded. Cooperation of both print and electronic media should be sought to educate investors about the considerations that should guide investment decisions. It should also be made abundantly clear to them that they have to bear the losses of wrong decisions themselves and should not expect regulators to undertake salvage operations. They should be made aware that stock prices cannot go on rising till eternity.

Strengthening monitoring and surveillance: Both stock exchanges and SEC should strengthen their monitoring and surveillance over all direct and indirect market actors. Those include banks, non-bank financial institutions, merchant banks, mutual funds, brokers, the stock exchanges, issuer companies, auditors etc. Appropriate actions should be taken against violators of relevant laws, rules and regulations.

Demutualisation: Stock exchange authorities are the front-line soldiers for ensuring market stability. A situation of conflict of interest arises when the brokers exclusively serve as members of the Board of Directors of Stock exchange and assume the role of primary regulators. Many exchanges around the world have been demutualised to resolve such conflict of interest. Bangladesh has recently followed suit and demutualised both exchanges (Dhaka and Chittagong). In order to derive the potential benefits of demutualisation it is essential that the Boards of Directors operate independently and fairly. They also have to ensure that their regulatory responsibility is not subordinated to profit motive.

Improvement of corporate accounts: In Bangladesh questions are often raised about the truthfulness, completeness and transparency of audited statements of corporate accounts. This is a vital prerequisite for stock investors to be able to make informed decisions. The establishment of the proposed Financial Reporting Council to exercise oversight over the auditors remains in a state of limbo. The relevant law which has remained in a draft form for a long time needs to be enacted soon.

Strengthening SEC: Despite some increase in manpower in recent times, SEC probably remains understaffed. Perhaps even more importantly, SEC should be allowed to offer competitive wages so that competent staff can be hired. Moreover, the chairman and members of the commission must not be selected on the basis of political affiliation. The criteria should be competences integrity and capacity to exercise legally vested authority fairly and independently.

Concerted and speedy enforcement action: A perennial problem in Bangladesh is that wrong-doers in the capital market either go unpunished or there are long delays in disposal of cases. It is important that there is close coordination among relevant agencies to ensure speedy legal action against manipulators. Otherwise, it will be hard to restore investors' confidence in the market.

This article is adapted from a presentation made by Mirza Azizul Islam, former finance adviser to the last caretaker government and also a former chairman of the Securities and Exchange Commission, at the

conference of Bangladesh Economists' Forum held in

Dhaka on June 21 & 22, 2014.