Banks' non-performing loans soar to Tk 1.46t

Annual official count for 2023 shows rise

JUBAIR HASAN | Tuesday, 13 February 2024

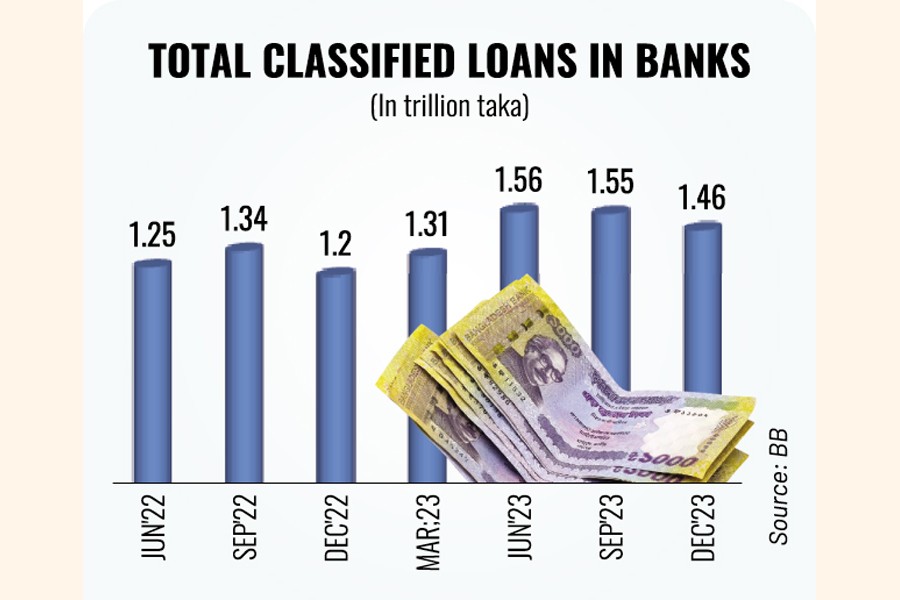

Classified loans in the banking sector showed an annual bulge by around 21 per cent to Tk 1.46 trillion in 2023, until a downturn towards the yearend under regulatory push.

The percentage of bad loans in banks stood up at 9.0 per cent against total outstanding credits worth Tk 16.18 trillion, as of last December.

A year ago, the share of the classified loans was 8.16 per cent, according to official data. At the end of 2022, the figure of non-performing loans (NPLs) in banks was recorded Tk 1.21 trillion.

That means the burden of bad loans in the banking industry surged by over Tk 250 billion throughout the immediate-past calendar year.

But in terms of quarterly analysis for July-September to October-December period, the amount of NPLs dropped by Tk 97.65 billion in three months till December 2023, according to the latest NPL-related statistics collated by Bangladesh Bank (BB).

In comparison with the NPLs-related data of its previous quarter (July-September), the volume of bad loans had dropped by 93 basis points as the overall volume of NPLs was recorded Tk 1.55 trillion, as on September 30, 2023.

The latest data show that state-owned commercial banks (SCBs) hold the biggest share of the classified loans (21 per cent or Tk 658 billion of their outstanding loans) followed by specialized banks (13.87 per cent or Tk 56.70 billion), private commercial banks (5.93 per cent or Tk 710 billion) and foreign commercial banks (4.82 per cent or Tk 32 billion).

The category-wise shares of NPLs at the end of 2022 were 20.28 per cent or Tk 565 billion in SCBs, 12.80 per cent or Tk 47.09 billion in specialised banks, 5.13 per cent or Tk 564 billion in PCBs and 4.91 per cent or Tk 30.48 billion in FCBs.

Seeking anonymity, a BB official says the volume of NPLs in banks annually surged significantly in 2023, which is not a good sign.

"But the good part is that it is declining gradually if we see the statistics of very recent quarters," the official says.

The central banker mentions that the regulator has already taken a roadmap with 17-point initiatives to cut down NPLs in the banking industry below 8.0 per cent by June 2026 by way of ensuring corporate governance through completely stopping the tendency of disbursing limit-crossing loans, releasing loans through forgery and borrowing under pseudonyms.

"So, people will see more cuts in NPLs in coming months," the BB official says.

Managing director and CEO of Mutual Trust Bank (MTB) Syed Mahbubur Rahman says the volume of NPLs increased by Tk 250 billion in a year in 2023, which is "very alarming".

"The commercial banks need to take drastic actions to get rid of the burden of NPLs that has further intensified the liquidity stress in the banks," he adds.

The experienced banker welcomes the regulator's recent NPL-reducing roadmap as part of government's financial-sector reform initiatives. "We need to see its proper implementation."

Mr Rahman suggests that the judicial infrastructure and process ought to be further improved in dealing with huge backlog of cases as the number of willful defaulters keeps growing.

However, a senior banker, preferring not to be quoted by name, says the banks normally concentrate more on rescheduling affairs to maintain a relatively better balance sheet at the end of a year.

"If we see the rescheduling statistics in the last quarter of the immediate-past calendar year, we will probably get better understanding of the NPLs situation," he told the FE writer about the window-dressing.

The last quarter's rescheduling-related data are not available with the BB. Banks rescheduled over Tk188 billion of their default loans in the January-September period of last year, which increased by 63 per cent or Tk 73.0 billion on a year-on-year basis.

Talking to the FE, former lead economist of World Bank's Dhaka office Dr Zahid Hussain said although not unexpected, the news is not good as the stock of NPLs end of December 2023 was 20.8-percent higher than the stock at the end of December 2022.

"Equally, if not more worrying, is the 75.1-percent increase in provisioning shortfall," he said.

The eminent economist notes that the central bank has rolled out a roadmap for NPL reduction. "This is welcome. However, other than reducing the period for writing off bad loans, there are no concrete steps yet."

Adds the economist: "We need to target reducing the amount of distressed assets, not just the NPLs. Banks with extremely high distressed assets need to be brought under the Prompt Corrective Action (PCA) framework sooner than waiting till March next year."

jubairfe1980@gmail.com