Steering murky course in banking after rate rises

Banks plan long-term deposit mobilisaiton, short lending

JUBAIR HASAN | Tuesday, 28 November 2023

Continuously rising cost of deposit under changing interest regime worsens banks' liquidity stress and prompts them to opt for short-term lending and long-term fundraising to avert squeeze on their net interest margin (NIM).

Bankers say that, following policy-rate rises, they are weighing the steering of a murky interim course because of unpredictability of the scenarios that may be unfolding on the financial front.

The latest policy-rate hike by Bangladesh Bank (BB) is set to further increase the deposit rate, and the gradual changes in the rates as part of the central bank's ongoing inflation-combat moves keep changing the market dynamics too fast. And this quandary makes it difficult for the bankers to predict the future market scenarios, according to them.

Simultaneously, the existing liquidity stress coupled with the possible election-related instability and sagging private-sector credit demand prompted the banks to go for adopting 'lending short and procuring long-term deposit' policy, they said.

Talking to the FE, managing director and chief executive officer of Modhumoti Bank Ltd Shafiul Azam said the latest 50 basis-point hike in the policy rate by the central bank would help enhance the rates on deposits and lending.

"But banks cannot increase the lending rate apace with the deposit rate as lending rate cannot be readjusted in six months once it is fixed," he said.

"So, now the policy is lending short-and procuring long-term deposit," the senior banker said about the short and long of banking after rate rises.

Managing director and chief executive officer of Mutual Trust Bank Limited (MTB) Syed Mahbubur Rahman thinks it will certainly put pressure on the banks' NIM as the policy-rate adjustment will immediately push up the deposit rate while the lending rate cannot be increased immediately--and there's a lag effect of 6 months.

And long-term investment is not suitable in the current context of the money market where working capital continues turning into term loan as borrowers face difficulties in repayment because of multiple factors, he said.

"So we need to be very cautious now in terms of giving loans," the experienced banker says about their strategy of steering an interim course of balancing.

Seeking anonymity, the treasury head of a private commercial bank said predicting future market scenarios becomes extremely difficult in the current market situation as the dynamics change too fast in the higher-yield regime.

On the other hand, the senior treasury official said, liquidity in banks, both in the form of surplus and cash, keeps falling fast. "So, the latest policy-rate increase would mount pressure further on the banks facing liquidity crunch. And they have to be very careful even in giving short-term loans."

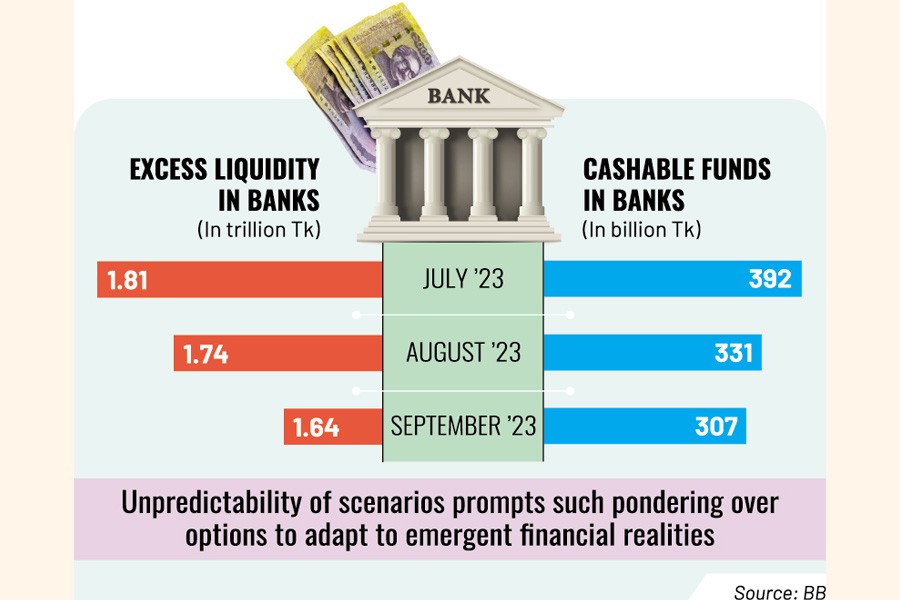

According to BB statistics, the excess liquidity in commercial banks dropped to Tk 1.64 trillion in September from August count of Tk 1.74 trillion. In July 2023, the volume of surplus credits was recorded at Tk 1.81 trillion.

Excess liquidity includes various cash and cash- equivalent assets, including treasury bills and bonds, along with cash reserves other than liquid assets.

The cashable funds available in the banks' vaults have also been falling fast, having reached Tk 307 billion at the end of September 2023. The volumes of cash money were recorded at 331 billion and Tk 392 billion in August and July respectively.

jubairfe1980@gmail.com