Basel III: Challenges for the banking sector

Jafrin Sultana | Wednesday, 12 February 2014

Bangladesh has started preparations to implement the Basel-III framework for bank companies from 2014 in line with the global standard. The banking regulation on capital requirements known as Basel III will have a big effect on the world's financial systems and economies. On the positive side, fortified capital and liquidity requirements should make Bangladesh's banking sector safer. On the other side, enhanced safety will come at a cost, since it is expensive for banks to hold extra capital and to be more liquid. Loans and other banking services will be more expensive and harder to obtain which will result in slower economic growth due to higher credit costs and reduced credit availability. Now it needs to address the challenges of implementing the Basel III framework, especially in areas such as augmentation of capital resources, growth versus financial stability, challenges for enhanced profitability, deposit pricing, cost of credit, maintenance of liquidity standards and strengthening the risk architecture.

Bangladesh Bank (BB) Executive Director SK Sur Chowdhury said: "We've started the ground work to implement the Basel-III for bank companies by 2014." The most significant challenge the banking sector of Bangladesh will be facing while implementing Basel III is the need to balance the interests of the businesses against the needs of the regulator.

The Basel III introduces a lot of modifications in terms of stringent capital requirements and leverage ratios. The Basel III proposed an increase in the minimum common equity requirement from 2.0 per cent to 4.5 per cent. In addition, banks are required to hold a capital conservation buffer of 2.5 per cent to withstand any future stress bringing the total common equity requirements to 7.0 per cent. The Basel-III strengthens bank capital requirements and introduces new regulatory requirements on bank liquidity and bank leverage. In addition to the level of risk management, the Basel-III has stipulated that in calculating capital adequacy a bank should consider its size (leverage ratio), Liquidity Coverage Ratio (LCR) and countercyclical position. The liquidity coverage ratio (LCR) and the net stable funding ratio (NSFR) are pros and cons of the Basel-III framework. By consolidating all these, the Basel Committee on Banking Supervision (BCBS) released the Basel III framework entitled "Basel III: A Global Regulatory Framework for more Resilient Banks and Banking systems" in December 2010 (revised in June 2011).

According to the BCBS, the Basel III proposals have two main objectives. The first one is to strengthen global capital and liquidity regulations with the goal of promoting a more resilient banking sector. The second one is to improve the banking sector's ability to absorb shocks arising from financial and economic stress.

The essence of the Basel III revolves around compliance regarding capital and liquidity. While good quality of capital will ensure a stable long-term provision, compliance with liquidity covers will increase ability to withstand short-term economic and financial stress.

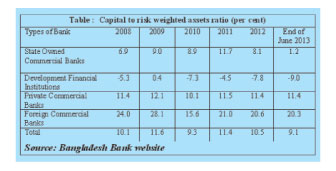

CAPITAL ADEQUACY NORMS: IMPACT ON BANKS: (Capital Adequacy Ratio (CAR) = Total Regulatory Capital (Tier I + Tier II + Tier III)/Risk weighted Assets (Credit risk + Market risk+ Operational risk.) Under the Basel-III, banks in Bangladesh are instructed to maintain the minimum capital requirement (MCR) at 10.0 per cent of the risk weighted assets (RWA) or Taka 4.0 billion as capital, whichever is higher, with effect from the July-September 2011 quarter. In the fourth quarter of 2010 banks were required to maintain the MCR at 9.0 per cent of the RWA or Taka 2.0 billion, whichever was higher.

As of 2012, the SCBs, DFIs, PCBs and FCBs maintained the CAR of 8.1, -7.7, 11.4 and 20.6 per cent respectively. Two SCBs, two DFIs and four PCBs could not maintain the minimum required CAR. The CAR of the banking industry was 10.5 per cent in 2012 and 9.1 per cent in 2013 up to end of June. All foreign banks maintained the minimum required capital. The industry's CAR stood at 9.1. The financial health of Bangladesh's banking system has improved significantly in terms of the capital adequacy ratio.

KEY ISSUES CONCERNING BANGLADESH'S BANKING SECTOR: In order to meet the new capital requirements, banks can issue new equity and increase retained earnings by reducing dividend payments, increasing operating efficiency, reducing compensation and other costs, raising average margins between borrowing and lending rates and increasing non-interest (fee) income. On the other hand, the banks can reduce risk-weighted assets by lowering the size of loan portfolios, tightening loan agreements, reducing loan maturities and reducing or selling non-loan assets.

CHALLENGES FOR BASEL III IMPLEMENTATION:

Implementing the countercyclical capital buffer: A critical component of the Basel III package is implementation of a countercyclical capital buffer, which mandates a bank to build a higher level of capital when in a good position, consistent with safety and soundness considerations. Here the foremost challenge to the Bangladesh Bank is to identify the inflexion point in an economic cycle which should trigger the release of buffers. It also requires a long series of data on economic cycles. In Bangladesh, what macroeconomic data is needed? What are the options before the Ministry of Finance and the BB?

Risk management: In recent years many banks strengthened their risk management systems which are adequate to meet the standardised approaches under the Basel II. A few banks are making efforts towards implementation of advanced approaches. The larger banks need to migrate to the advanced approaches, especially as they expand their overseas presence. The adoption of advanced approaches to risk management will enable banks to manage their capital more efficiently and improve their profitability. Banks also need to strengthen their risk management and control system so as to allocate risk capital efficiently and improve profitability and shareholder's return. The important issues here are: What aspects of risk management should the banks focus on? How do they improve the risk architecture for SCBs? How can banks strengthen risk management capacities so as to generate adequate and qualitative data?

Systemic risk: While any bank-specific risk is relatively easy to identify, a systemic risk is much more difficult. For this purpose the following parameters need to be considered for market study which includes trend of the credit/GDP ratio, market volatility, NPA/GDP ratio, inflation and banks' exposure to any sensitive sector. To identify the systemic risk there is a need for developing a large historical macroeconomic database for the above parameters.

Data quality: Ultimately, how much risk a bank wants to take at what rate of return must be clearly defined. Conceptually, the following metrics and accompanying indicators can assist in articulating the bank's risk appetite: earnings volatility, profitability metrics such as ROE, RAROC, RORAC, EVA, target capital ratios, target risk profile and zero tolerance on risks. Risk appetite should not exceed an entity's risk capacity, and in fact appetite should be well below the capacity.

Under the Basel III the capitalisation ratio is arrived at by dividing equity capital by the risk weighted assets. How can banks minimise the risk weighted assets? Another point for consideration is mandatory requirement of investment in SLR (statutory liquidity ratio) securities. The Basel committee has not accepted the argument of considering SLR securities as part of the liquid funds. Bankers' view is that as the BB is the lender as the last resort, investment in the cash reserve ratio (CRR) and SLR can be used to get liquidity support from the regulator in the event of any need and hence the same may be considered as part of liquid assets to maintain the Liquidity Coverage Ratio (LCR) and the Net Stability Funding Ratio (NSFR) as required by the Basel III. The BB too is of the opinion that a certain portion of the SLR investment may be allowed as part of the liquid asset. If this is not allowed, then there will be additional costs for the banks to maintain liquid assets above the requirements as set out in the SLR and CRR. In order to meet the Basel III compliance, banks have to ensure that risk and finance teams have quick access to centralised, clean and consistent data.

The writer is Assistant Professor, Department of Business Administration, Dhaka City College. jafrin77@gmail.com