BD explores ways to boost revenue

Sunday, 3 November 2024

Bangladesh has significant potential for mobilising revenue collection, as highlighted by a recent official assessment of revenue buoyancy, a measure reflecting how tax revenues respond to economic growth, reports UNB.

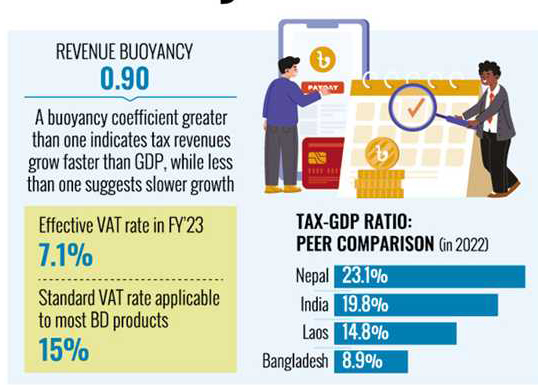

Revenue buoyancy, the responsiveness of revenues to gross domestic product (GDP), is a critical metric for gauging the performance of a revenue system and the revenue growth forecast. A buoyancy coefficient greater than one indicates tax revenues grow faster than GDP, while less than one suggests slower growth.

Using real GDP and real revenue growth rates from FY12 to FY23, the analysis found an average revenue buoyancy of 0.90, which is below one. This lower score highlights the scope for enhancing revenue mobilisation in Bangladesh, as per the finance ministry document.

The official assessment also noted that the effective tax rate can serve as another measure of revenue performance. For example, the effective rate of VAT can be derived by comparing it with consumption data from the real sector.

An analysis shows that the effective VAT rate has risen in recent years, reaching 7.1 per cent in FY23. However, this remains well below the standard of the 15 per cent VAT rate applicable to most products in Bangladesh.

Bangladesh's revenue collection still lags behind comparable economies. In 2022, the general government revenue-GDP ratio was 23.1 per cent in Nepal, 19.8 per cent in India, and 14.8 per cent in Laos, while it was only 8.9 per cent in Bangladesh.

There is broad consensus that a positive correlation exists between economic development levels and revenue collection. To achieve the country's development objectives, the finance ministry has called for major reforms to enhance the effectiveness, efficiency, transparency, and fairness of the tax administration system.

The document also emphasises revisiting tax exemptions to ensure that these benefits support the broader economy and do not disproportionately favour wealthier individuals at the expense of low-income groups, thus undermining the redistributive aims of the fiscal policy.

There is also significant room for improvement in tax return submissions. In FY22, only 33.3 per cent of TIN holders filed tax returns, a figure that is markedly higher in similar countries.

The ministry has outlined several modern reform strategies to strengthen revenue mobilisation. These include expanding the tax base, adopting a modern property tax system, introducing green and carbon taxes, simplifying tax collection, fully automating tax filing and payment processes, and minimising direct interactions between tax collectors and taxpayers.

Other strategies include making audits more selective, productive, and criteria-based, as well as separating tax policymaking from tax collection.

The government has made progress in this direction, with an increased share of income tax and VAT in total revenue. However, there is still a need to reduce dependency on indirect taxes and focus more on direct taxes.

The actual share of direct taxes in total revenue was 32.3 per cent in FY21, which increased slightly to 32.7 per cent in FY23. To sustain revenue growth, the government will continue efforts to broaden the tax base, shift reliance from trade taxes to direct taxes, and further accelerate the growth of direct taxes in the coming years.