CCP: What it does and how

Mohammed Imam Hossain | Monday, 9 December 2019

![]() Automation of the trading system in Bangladesh started in mid-1990s. The objective was to make the capital market more efficient by providing all participants with quicker and more effective means of exchanging information. New products and instruments have been made available, thanks to sophisticated information and communications technology (ICT).

Automation of the trading system in Bangladesh started in mid-1990s. The objective was to make the capital market more efficient by providing all participants with quicker and more effective means of exchanging information. New products and instruments have been made available, thanks to sophisticated information and communications technology (ICT).

As part of continuous modernisation and increment in capacity of Bangladesh's capital market, market authorities and stakeholders took different initiatives such as modernisation of stock exchanges, and establishment of Central Securities Depository. Bangladesh Securities and Exchange Commission promulgated Clearing & Settlement Rules, 2017 to form a Central Counterparty (CCP) in Bangladesh. Under the said rules, a company styled Central Counterparty Bangladesh Limited (CCBL) was formed in January 2019.

In the wake of the global financial crisis in 2008, the G20 leaders agreed at the 2009 Pittsburgh summit that all standardised derivatives contracts should be traded on the exchanges or electronic trading platforms and cleared through third party clearing system; thus the central counterparties (CCPs) were introduced in the capital market. In the United States, as part of former President Barak Obama's financial  regulatory reform plan of 2009, traders of derivatives such as credit default swaps (CDS) started in open exchange with a central clearing house and in March 2010, the Options Clearing Corporation (OCC) stated that it was moving forward in backing equity derivatives using CCP. The European Association of CCP Clearing Houses (EACH) represents the interests of Central Counterparties (CCPs) in Europe since 1992 and it came into force under European Market Infrastructure Regulation (EMIR) effective from 2012.

regulatory reform plan of 2009, traders of derivatives such as credit default swaps (CDS) started in open exchange with a central clearing house and in March 2010, the Options Clearing Corporation (OCC) stated that it was moving forward in backing equity derivatives using CCP. The European Association of CCP Clearing Houses (EACH) represents the interests of Central Counterparties (CCPs) in Europe since 1992 and it came into force under European Market Infrastructure Regulation (EMIR) effective from 2012.

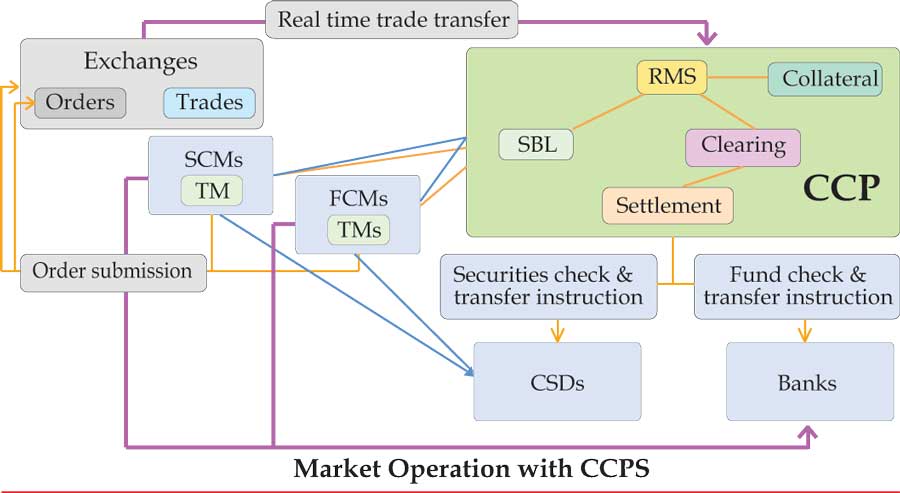

CCP, which stands for central counterparty, sometimes refers  also to as a central counterparty clearing house. A CCP plays a role in the area of risk management, settlement and clearing of securities and derivatives transactions, particularly those carried out on a trading venue. One key characteristic of these transactions is that the obligations are settled at a later time than that at which the actual trade took place. If, in the intervening

also to as a central counterparty clearing house. A CCP plays a role in the area of risk management, settlement and clearing of securities and derivatives transactions, particularly those carried out on a trading venue. One key characteristic of these transactions is that the obligations are settled at a later time than that at which the actual trade took place. If, in the intervening  period, either of the two parties is unable to meet its obligations, this could cause problems for the other party. To prevent this negative spiral, the CCP positions itself between buyer and seller as soon as transaction is executed. The CCP thus becomes the new counterparty of both the buyer and the seller. As a consequence, the relationship between the two original trading parties no longer exists legally. After becoming the new counterparty of both the buyer and the seller, the CCP proceeds to clear the transaction, this is called the novation.

period, either of the two parties is unable to meet its obligations, this could cause problems for the other party. To prevent this negative spiral, the CCP positions itself between buyer and seller as soon as transaction is executed. The CCP thus becomes the new counterparty of both the buyer and the seller. As a consequence, the relationship between the two original trading parties no longer exists legally. After becoming the new counterparty of both the buyer and the seller, the CCP proceeds to clear the transaction, this is called the novation.

The CCP clearing activity consists of administering, risk-taking, netting and guaranteeing. The parties that trade in securities and/or derivatives often conclude a large number of transactions in a single day, while the same party can act both as buyer and seller of the same security or derivative. The CCP records all these transactions in its administration, so that it knows exactly who has entered into which obligation. At the end of the trading day, the CCP nets all the transactions that a specific party has carried out in the same security or derivative, thus creating an open position.

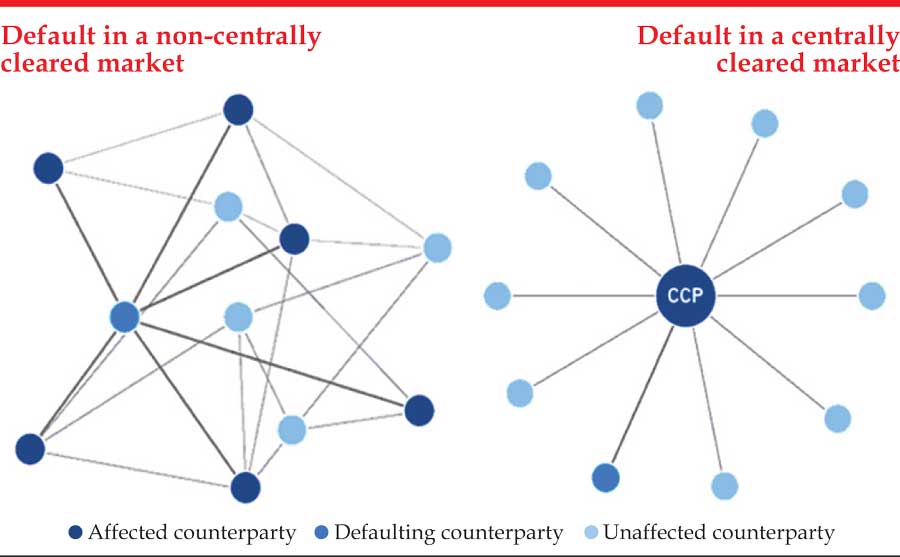

The netting process under CCP greatly reduces the number of transactions and the total value to be settled step by step which is called multilateral netting. The CCP guarantees the settlement of the netted positions using settlement guarantee fund (SGF). This means that the settlement of transactions can proceed even if one of the original parties runs into problems and is no longer able to meet its obligations, thus CCP needs available contributory fund under SGF framework. This concept breaks the chain defaulting in conventional bilateral settlement.

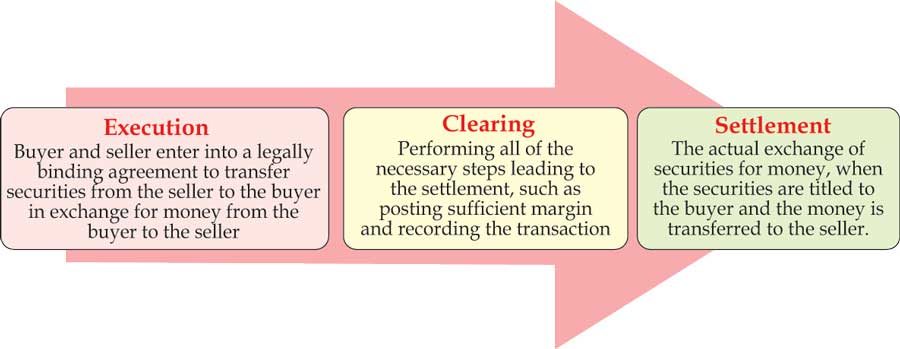

In standard process, we may divide a transaction life into three (03) periods:

* Execution or trading;

* Clearing; and

* Settlement.

* Execution is the trading in a specific period whereby the seller agrees to sell and the buyer agrees to buy a security in a legally enforceable transaction.

* Clearing is the process to identify the obligations to be settled. This process also comprises the arrangement of transfer of money and securities. There are two types of clearing:

* bilateral clearing (OTC)

* central clearing (On exchange clearing house)

* Settlement is the actual exchange of money and securities against each obligation on the settlement day following any of three settlement models of BIS (Bank for International Settlements).

A CCP enables a safer and more efficient settlement of securities and derivatives transactions. By netting and guaranteeing transactions, the CCP reduces the risk for buyers and sellers. This makes the market more attractive to investors. The more investors a market attracts, the more liquid it will be; and this liquidity, in turn, attracts even more investors. Despite this obvious advantage, there are still securities markets that operate without a CCP. This is because of the costs attached to the services of a CCP. As soon as a party can no longer meet its obligations, the CCP takes over these obligations. In order to play this role, the CCP requests the transacting parties to deposit collateral. This collateral may be a combination of cash, cash equivalent and non-cash financial instruments.

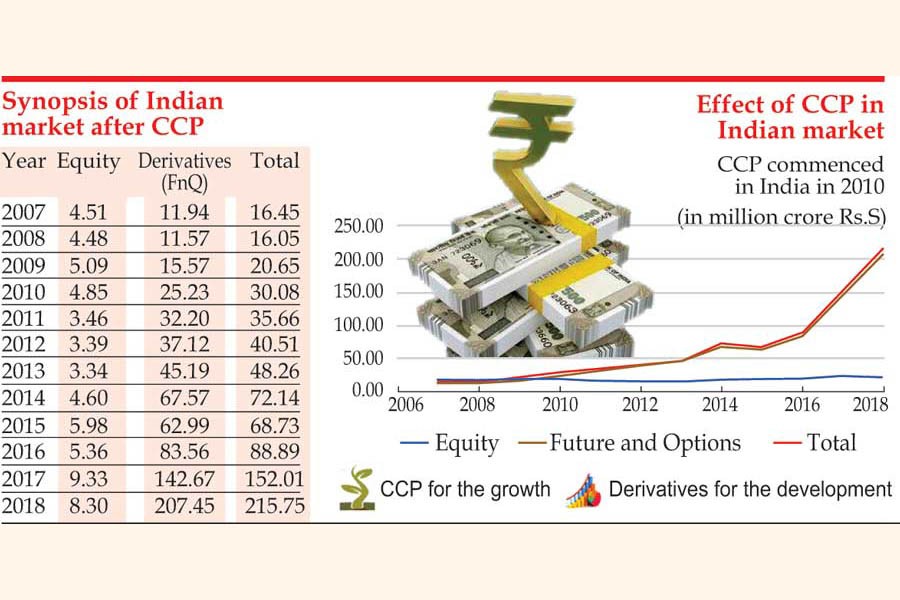

Nowadays, the WFE is giving emphasis on CCP and Derivatives as two most influential complementary components for growth and development of the capital market worldwide. If we compare the status of capital market in India before and after incorporation of CCP, most of the growth and development took place after starting CCP-based post trade operation.

In addition, the CCP requires an extensive and robust risk monitoring system. The parties that make use of a CCP's services pay for implementation and maintenance of this system. These payments can essentially be seen as a kind of risk premium, settlement charge and so on.

The upshot is that a securities market will only start using a CCP if it benefits from increased number of transactions, trading of derivatives as a result of safer and more efficient securities and derivatives transactions are greater than the collateral and risk premium costs.

Mohammed Imam Hossain is Team Leader at CCP Project & DGM at DSE

imam.hossain@dse.com.bd