Challenges in global value chain

Mohammad Abu Yusuf and Mahmudul Hasan | Tuesday, 28 January 2014

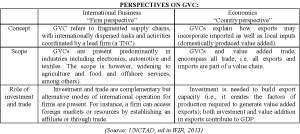

A value chain is the full range of activities that firms and workers do to bring a product or service from its conception to its end use and beyond. The activities that are included in a value chain are design, production, marketing, distribution and service/support to the end user. All the activities in a value chain can be done by a single firm or divided among a number of firms. They can be contained within a single geographical location or spread over wider geographic regions/countries. When the chain of interrelated activities to bring out a product or service from concept to complete production and delivery to final consumers is divided among multiple firms in different geographic locations, it is known as the Global Value Chain (GVC).

The fragmentation of production processes and the international dispersion of activities between affiliates and partners in the GVC have led to the emergence of borderless international production networks (IPNs). The service industry also participates in the GVC. Its involvement in the GVC mainly occurs through value addition incorporated in exported manufactured products. Countries participate in the GVCs at different levels of sophistication that range from resource-based exports to low-medium and high-tech manufacturing exports, to exports of knowledge-based services.

Low-cost locations are better able to integrate into the GVCs in selected labour-intensive industries. Bangladesh's significant participation in the GVCs in readymade garment (RMG) sector has been possible due to its low labour costs. The presence of human resources also influences the location of specific value addition in the entire value chain. For example, the availability of certain specialised skills and trained human resources has helped India to develop IT firms and China, Taiwan, Malaysia and Singapore to develop electronics firms there. The advent of new transportation, information and communication technologies has facilitated the spatial division of value chains by driving down the cost of accessing information and trading products and services.

Value chain could be 'producer-driven' and 'buyer-driven'. Producer-driven GVCs are found in high-tech capital-intensive industries such as automotive, pharmaceuticals or semi-conductor industry. Transnational manufacturers/industries are the main drivers in this value chain and they rely on technology and R&D for production. They control the design of products as well as most of the assembly which is usually fragmented in several countries. Buyer-driven value chain is common for labour-intensive industries such as the garment industry, where power/governance is exercised by retailers and marketers (e.g. Nike, Ralph Lauren). In such a chain, production can be totally outsourced, the focus being on marketing and sales. The GVCs with lower needs for capital and relying on fewer skilled workers are generally organised this way, as is seen in the apparel chain. This (buyer-driven value chain) strategy by transnational firms has coincided with the shift of developing countries from import-substituting industrialisation (ISI) to export-oriented industrialisation (EOI).

The global expansion of value chains has created new opportunities for many developing countries. In particular, firms, which are involved in electronics, food products, garments or horticulture business, participate more in global value chains. But still, many developing countries, and in particular LDCs, remain on the margins of global trade. To improve the situation, In the Fourth Global Review of Aid for Trade (held in July, 2013), the WTO analysed the data collected through the OECD-WTO monitoring survey in order to get a better understanding of the role of skills in enhancing the competitiveness of small and medium-sized enterprises (SMEs). It made it possible for them to successfully integrate and move up value chains. The analysis found labour force skills as a main constraint by about 45 per cent of developing country suppliers in tourism, textiles and apparel and ICT value chains and by 38 per cent of suppliers in the agro-food chain.

DOMESTIC VALUE ADDITION: The participation rate in the exports of goods indicates the extent to which a country's exports are integrated in international production networks. Large economies, such as the United States or Japan, tend to have significant domestic value addition and to rely less on foreign inputs. There are, however, exceptions such as China and Germany. Economic structure and export model also influence a country's share of domestic value addition in its export trade. For example, countries with significant shares of entrepôt trade, such as Singapore, Hong Kong (China) will have lower shares of domestic value addition in trade and higher shares of foreign value addition (UNCTAD,2013). Access to significant share of mineral and other natural resources such as oil or other commodities determines the share of their domestic value addition vis-à-vis foreign value addition. Furthermore, such access determines the sector with which their value chain relates. For example, Saudi Arabia and Russia have relatively higher domestic value addition in their exports of oil/mineral resources. Similarly, 70 per cent of African countries' value chains are related to agricultural products, mineral resources and other natural resources as they are endowed with these primary resources.

Bangladesh's export structure does not depend on entrepôt trade/re-export and it has significant level of participation in the GVC, especially in knit garments. In the initial stage of industrialisation, Bangladesh had to import a significant quantity of input materials. Over the last two decades, Bangladesh has been able to build a strong backward linkage in the production of yarn and knit fabrics. Moreover, previously most accessories such as cartons, hangers and zippers had to be imported by Bangladesh's RMG sector. But most of these items are now produced locally by SMEs. The relaxation of the EU's RoO requirement from three stages to two stages (yarn to fabrics, fabrics to apparels) in 2004 stimulated the private sector investment in backward linkage activity. Development of such backward linkage industries has reduced the dependency on input material and thus increased the share of domestic value addition in exports of knit garments.

BANGLADESH IN GVC: Bangladesh has been able to participate in the GVC of the textile sector by manufacturing yarn, accessories and textiles and more prominently in a value chain by manufacturing garments. Bangladeshi manufacturers are mostly involved in original equipment manufacturing (OEM). Over the last few decades of involvement in the industry, the Bangladeshi entrepreneurs learnt from experience. They also secured technical and financial support from international buyers (garments being a buyer-driven GVC). Such a support by and pressure from international buyers eventually helped the RMG sector to increase its productivity and compliance culture. Their entrepreneurial zeal to be more competitive, increased focus on more value added activities and exposure to foreign markets/technology appear to have motivated them to gradually update production techniques. Such upgrade of production techniques has allowed the sector to move up from the early stage of production (assembly) to the OEM. Bangladesh's OEM garment sector produces garments to be affixed with the brands of other companies.

Apart from garments and textiles, Bangladeshi firms are participating in the GVCs by exporting raw jute, sesame seed (used in manufacture of medicine and oil), carpet backing cloth (CBC), copper scraps (used in manufacturing electric wire), rice-bran oil, parts of cycle (tyre tube), and waste clothes generated in garments industry. In FY 2010-11, Bangladesh had exported 1240 tonnes of CBC worth Tk 130 million to Australia and New Zealand.

BANGLADESH EXPERIENCE IN GVC: Fragmentation of the global production system results in production of different parts/components of the same product in different places. About 60 per cent of global trade today (more than $20 trillion) consists of trade in intermediate goods and services. These intermediate goods/services are incorporated at various stages in the production process of goods and services for final consumption. Twenty years ago, the import content of exports was 20 per cent. Now (in 2012) it is around 40 per cent. In order to create jobs, diversify exports and attract FDI (foreign direct investment). Bangladesh may initially try to excel in making special parts and components of merchandises, export them to other countries and then to build a full-fledged industry to be an important partner in the global value chain.

INITIATIVES REQUIRED: The Bangladeshi garment firms have been upgrading their production activities effectively. Now it seems necessary for them to undertake steps for functional upgrading from FOB-1 (where local producers take the responsibility of sourcing intermediate materials and production) to the highest value added production arrangement of FOB-2. FOB-2 is characterised by complete production process including sourcing of materials, designing (the highest value added activity in garments production) and all levels of production.

A good infrastructure is a necessity to support involvement in GVCs. So necessary infrastructure needs to be built to support value-chain development and participate in global trade. Tripartite partnership (owners, workers and government) and regular interaction between stakeholders seems important to reduce labour unrest and increase productivity.

Trade facilitation (through expedited imports and exports) can help trade especially in time sensitive GVCs.

Through duty/tax incentives and rationalising tariffs/ and non-tariff barriers, domestic firms/SMEs need to be given access to world class goods and services. This is because the protective trade policy is most likely to backfire in the case of the GVCs where imports are crucial for exports. In a similar vein, non-tariff barriers on imports adversely affect export competitiveness. As such, all sorts of barriers need to be minimised.

Bangladesh has potential to export camera parts, tyre tubes for cycle, and golf shape in Japan/some other countries. It, however, needs quality improvement and linkage development. Mitsubishi invests in China and Thailand to produce high-tech motor parts (automatic parts) for its own use, but they do not do it in Bangladesh due to lack of expertise and skills in the country to meet their quality standards.

Technical assistance in the area of education and training can provide SMEs in developing countries with access to the right skills. This will enhance their chances to enter or move up global and regional value chains.

CHALLENGES: In case of manufacturing value chains, major challenges are shortages of skilled manpower, lack of technology spillover, poor working condition, inconsistent quality and unfavourable tariff structure. Cost of business start-up, although it came down, is still considered to be very high for small and medium-scale suppliers. Complex and lengthy customs procedures have also constrained the LDCs (least developed countries) in participating more extensively in the GVCs. Poor logistics - for both internal and external trade - is a major bottleneck in the development of value chains in LDCs. Political instability, blockades and interruptions in normal economic activities affect LDC/developing countries (which have to endure such difficulty) total manufacturing activities and supply chain. For shortage of transport during blockades, businesses face difficulty in transporting imported raw materials and capital machinery in Bangladesh. They also face severe hurdles in sending consignments to ports and airports for export. Such interruptions add costs to business and make it difficult especially for small and medium-sized businesses (SMEs) to participate in the GVC. Moreover, difficulty in starting a new business (including company registration), lack of an electronic single window for foreign trade and inadequate taxation advice also hamper participation in the GVC. These two are also part of infrastructure (known as 'beyond basic infrastructure').

Bangladesh can enhance its participation in the GVC as well as increase domestic value addition by developing its domestic productive capacity for exports, diversification, establishment of more contract manufacturing links (Non-equity modes i.e. NEM relationships) with MNCs/global buyers, capacity enhancement to move to high-tech manufacturing. Knowledge-based service delivery in the FDI and technology transfer can act as a catalyst for domestic productive capacity building.

Dr. Mohammad Abu Yusuf is a Senior fellow and Mahmudul Hasan is a Research Associate at Bangladesh Foreign Trade Institute (BFTI).

ma_yusuf@hotmail.com