Cutting interest rate to reduce interest spread: Is it reasonable?

Md Jamal Hossain | Thursday, 13 February 2014

The Dhaka Chamber of Commerce & Industry (DCCI) in a statement issued on January 28, 2014 said: "Bangladesh Bank should take effective steps in achieving target of private sector credit growth through reducing the spread of interest rate of the commercial banks". To rephrase the statement, the prescription is about to reduce the interest rate to reduce interest rate spread. This prescription is not viable not only from theoretical side but also from empirical side as well. The Bangladesh Bank (BB) should not take such an initiative to reduce interest rate spread. Such quantitative slashing of interest rate will not reduce the interest rate spread in the end; rather it will give rise to more interest rate spread in the future.

SPREAD OF INTEREST RATE: To assess the above suggestion of the DCCI, we need to determine why interest rate spread is high in our country. Higher risk and higher interest policy do not work well for banks and such policy is not a return maximising policy. Such reasoning implies that interest rate spread can't be reduced by undertaking quantitative slashing method of interest rate. What will happen is that a cut in the interest rate will cut the total interest rate while keeping the spread still in the same place. This will create a deep trouble increasing risks more for banks and, in the end, banks will be forced to raise the interest rate not to the same extent they reduced but more just to compensate the interim loss they will incur. Therefore, to reduce the interest rate spread, we need qualitative slashing not the quantitative slashing.

QUALITATIVE VS. QUANTITATIVE SLASHING OF INTEREST RATE: To clarify our point, by quantitative slashing we mean a direct cut in the interest rate and by qualitative slashing we mean not the direct cut in the interest rate but a direct cut in interest rate spread while keeping stable the return maximising rate. Now it seems clear which method is more desirable for banks. While theoretically it seems plausible that a direct cut in the interest rate can reduce the interest rate spread, practically it will not work well for banks since the factors that cause interest rate spread remains totally undisturbed by the direct cut. What we need to reduce the interest rate spread is to devise a method that can mitigate the impact of those factors that cause interest rate spread such as default risk. Since, banks charge high rate of interest to compensate the default risk, it would be more desirable for banks if they can practise some banking rules that can take care of such risk while giving them enough room to make interest rate spread as small as possible.

One of the devices that banks can use is the credit rationing rule to reduce interest spread. Credit rationing rule implies that banks would not respond to higher risk and higher interest rate policy, rather they will fix the interest at some point and will not lend below this rate and also above this rate. In following such a method, banks will rigorously judge the credit worthiness of borrowers and will be able to get rid of default risk trap since in most of the cases bad borrowers bid the higher rate and once they get the loan sanction, they are likely to forget what they promised and start playing with banks. Such qualitative measure will help banks to reduce risks without raising interest rate or substituting higher risk for higher interest rate. That directly indicates that interest rate spread will be reduced by this measure too. This point can be illustrated giving a stylised example of lending. Let's say X bank has Tk 1.0 and wants to lend it. Also assume that it can lend the money either following rationing technique as specified above or following the higher risk and higher premium rule. Moreover, it can be risk-averse lender or risk-neutral lender. Now the question how the bank can reach a point of combination of lending at which it finds the maximum return from lending of Tk 01. This point is illustrated in the following figure:

In the above figure expected return (ER) from lending at the rationed rate of interest (rc) is measured on the vertical axis and the expected return from the lending at the higher risk and higher premium rule based rate (r) is measured on the horizontal axis. The curve AJ depicts the risk averse behavior of the bank and the AC depicts the risk neutral behavior of bank. If he is risk-neutral he will be indifferent among any combination chosen on the AC line. That means if he chooses to lend Tk 01 in any combination, his return will be maximised at every combination. But on the AJ line, he is not risk-neutral and any combination on this line is not return maximising. There exist one combination on this curve that will render the maximum return and the rest will not. Let's say out of Tk 01, he lends major fraction following rationing rule and at the rationed rate. Then, he might find by trial and error the best combination which is pointed in the figure as the low interest spread zone. This is point at which its profit must be the maximum. To check, one can confirm such result just checking the slope of AC and AJ. It seems clear that at the low interest spread zone slope of AC and AJ are equal. Therefore, the maximum return from lending of one Tk. X is [OF+OG].

Now, assume that he lends major fraction charging an interest rate based on higher risk and higher rate. In this instance, the combination chosen is pointed as the high spread zone and also the return achieved is less than [OF+OG]>[OH+OJ]. The lesson is that such qualitative slashing cuts only the unnecessary spread that springs from the risk-offsetting mechanism and since such risk are minimised through the qualitative slashing, interest spread must be minimum in such qualitative slashing regime than in the quantitative regime.

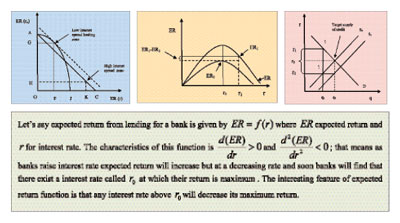

QUANTITATIVE SLASHING AND INTEREST SPREAD: Now, we need to show why quantitative slashing of interest or direct cut of interest rate will not help to reduce interest rate spread in our country. For this purpose, we can analyse expected return function of a bank and analyse what kind of consequences follow from such function. To say precisely:

If we graph the expected return function of the bank, then we will find a concave-shaped curve which is depicted in the following graph:

In the graph above, expected return from lending is measured on the vertical axis and interest rate on the horizontal axis. The concave-shaped curve shows that there exists an interest rate at which bank's return is maximised and we have pointed such interest rate as r0. Above this interest rate, return doesn't increase rather decreases. Let's say that the bank currently charges r1 rate of interest this is greater than r0. Charging of r1 directly implies that the bank follow the higher risk and higher rule. But the ER curve is drawn in such way that as if the bank was exercising the rationing rule. Since it doesn't, its expected return curve will get shrunk inside of the ER curve and will yield lower return for every rate of interest charged. Now, if a direct cut in the interest rate reduces the interest rate from r1 to r0, what will happen to the expected return of the bank expected will reduce at the reduced interest rate for banks unless it exercises rationing rule which is not true in this instance. The graph shows that at r0 expected return is ER2 and at r1 ER1 where ER1>ER2. This happens due to direct slashing of interest rate that takes away the interest spread that is, in fact, necessary for banks operating following the higher risk and higher premium. Since, ER1-ER2>0, such direct cut will induce more interest rate spread in the future and banks will not able to bear such direct cut for long. Sooner or later, central bank will be forced to raise the interest rate if it implements such ominous direct interest cut or quantitative slashing of interest.

QUALITATIVE SLASHING AND TARGET CREDIT SUPPLY: The suggestion for direct cut or quantitative slashing of interest was proposed to increase the supply of credit to reach the targeted level as argued by the DCCI. We argue that we don't need the direct slashing of interest rate to achieve the target supply of credit; rather qualitative slashing can also achieve the target without causing any direct cut. This point

illustrated with the help of the following graphical view:

In the above figure, interest rate is measured on the vertical axis and supply and demand for credit are on the horizontal axis. Now, if banks use qualitative slashing method to reduce interest spread, then it will fix the interest rate at r2 and will supply q1amount of credit or loan. As a result, interest will be reduced by (r1-r2) and this decrease of interest rate is a pure decrease in the interest rate spread. Since qualitative slashing is a profit or return maximising strategy, banks will be able to increase the supply of credit using such qualitative slashing. The reason is that by such qualitative slashing banks will achieve significant progress in risks management in lending and will achieve maximum return.

From the graph we can give a confirmative answer. It can be seen that by direct cut interest spread will be reduced by (r1-r3) and by qualitative slashing spread is reduced by (r1-r2) which is greater than (r1-r3). At the reduced rate r3, the target supply of credit q0is achieved. But this direct cut will hardly be able to achieve such result as we have seen in the above analysis since such direct cut will create conflict with banks return maximizing aim. Therefore, such direct cut is not practically feasible. But we can achieve the target credit supply q0 at the interest rate r2 as this is a profit maximising rate. So, banks supply curve for lending(S) will make a right shift and will become S1 assuring target credit supply q0. Therefore, we don't need the direct cut in the interest rate to achieve the target credit supply. Contradictorily, such direct cut will hinder the achievement of target credit supply. To achieve the target credit supply, we need the qualitative slashing of interest rate.

CONCLUSION: The major conclusions of the above analysis can be summarised as follows. First, direct cut in the interest rate is not desirable from the perspective of our country and such direct cut will rather create more trouble for banks. Second, such direct cut in the interest rate will give rise to more interest spread in the future if implemented. Finally, the Bangladesh Bank shouldn't implement such direct or quantitative slashing of interest rate to reduce interest spread. Such direct cut will eventually prove futile and create troubles for commercial banks. Rather it is more practical and feasible to encourage commercial banks to use qualitative slashing method to reduce interest spread. By such method, commercial banks will benefit themselves by paving the way for profit maximisation along with reducing interest spread.

Md Jamal Hossain writes from the

University of Denver, USA.

jheco.du@gmail.com