Financial inclusion of womenfolk

Emerging challenges that need redress

DOULOT AKTER MALA | Saturday, 8 March 2025

Nowadays, it has become common for all who get online to receive WhatsApp messages claiming that an individual is in distress and seeking monetary help through mobile financial services (MFS). Using technology, frauds offer people jobs or ways of additional income staying at home. Both educated and uneducated professionals fall victim to such digital scams, leading to significant financial losses.

Nowadays, it has become common for all who get online to receive WhatsApp messages claiming that an individual is in distress and seeking monetary help through mobile financial services (MFS). Using technology, frauds offer people jobs or ways of additional income staying at home. Both educated and uneducated professionals fall victim to such digital scams, leading to significant financial losses.

Such deep-fakes affect people across all demographics, regardless of gender. Con-tricks such as identity theft and phishing scams usually discourage women more than men from using digital financial services.

Uncontrolled financial fraud appears to be a blow to women-centric financial inclusion. Moreover, women cannot take full advantage of a rapid growth in the MFS sector due to lower digital and financial literacy and limited access to finance compared to males.

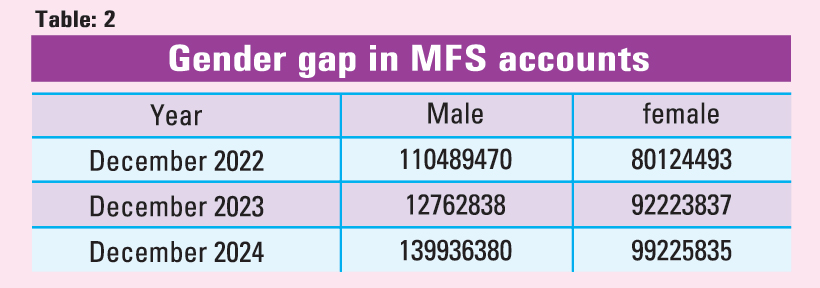

The spectacular rise in digital financial services fueled by mobile technology is supposed to break down the access barriers for women in Bangladesh. But the reality speaks something different. Despite a sharp growth in the number of MFS accounts in the last five years, the proportion of women having MFS accounts has been on the decline.

Bangladesh Bank data show women's account ownership fell by 6.45 percentage points in that period. Women held 48.28 per cent of total MFS accounts in December 2019, but that number fell to 41.83 per cent in December 2023, according to the central bank reckonings.

Bangladesh Bank data show women's account ownership fell by 6.45 percentage points in that period. Women held 48.28 per cent of total MFS accounts in December 2019, but that number fell to 41.83 per cent in December 2023, according to the central bank reckonings.

Thanks to widespread adoption of MFS services, the number of MFS accounts stood over 220 million (22.04 crore) as of December 2023, up 152 per cent from 8.74 crore five years ago, with females holding 9.22 crore accounts.

Women's Financial Inclusion Data (WFID) dashboard, launched by the central bank on March 6, 2024, in collaboration with ConsumerCentriX, Financial Alliance for Women, shows comprehensive data representation on the landscape of women's financial inclusion in Bangladesh.

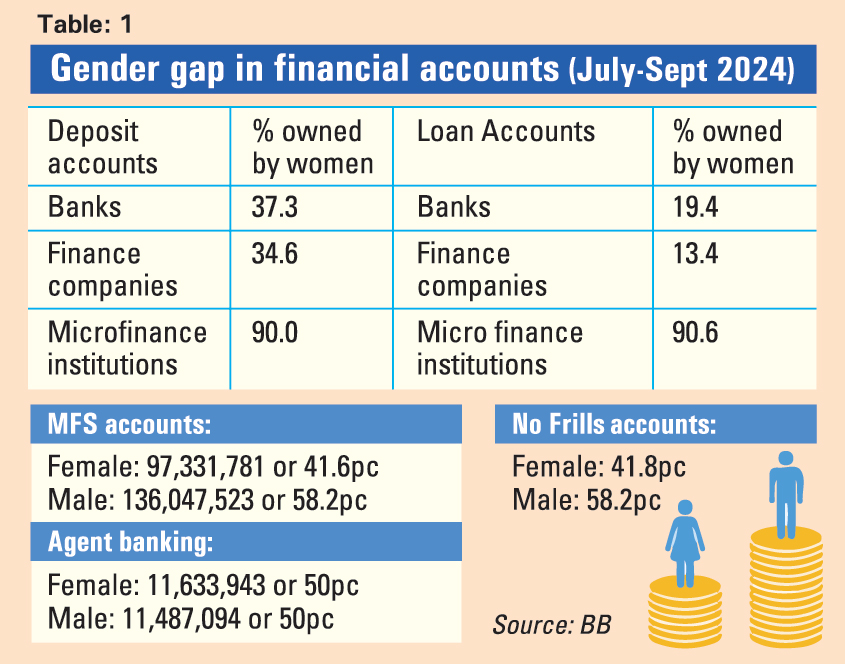

Apart from MFS services, the wide gender gap in bank deposits accounts and loan accounts remains visible. (table: 1) However, microfinance institutions' account-holders constitute 90.9-percent women while agent-banking accounts reached a gender-balanced stage in the July-August period of 2024. Also, 41.8 per cent of the No-frill account-holders are women.

However, microfinance institutions' account-holders constitute 90.9-percent women while agent-banking accounts reached a gender-balanced stage in the July-August period of 2024. Also, 41.8 per cent of the No-frill account-holders are women.

Although a number of financial institutions have women-centric financial products, such as BRAC Bank's Tara schemes, Dutch-Bangla Bank's women -entrepreneur financing, City Bank's City Alo, Trust Bank's Ekota, IDLC's Purnota, Eastern Bank's Smart Savings Account, Industrial and Infrastructure Development Finance Company Limited's Women Entrepreneur Loan, large gender gaps in the financial -account ownership do exist.

World Bank's Global Findex Database 2021 placed Bangladesh among the top seven countries having a large number of unbanked population. About 30 million people do not have an account in banks, NBFI or MFS.

There is no denying, however, that Bangladesh has made progress in financial inclusion riding on reach-all techs, namely Mobile Financial Services and agent banking, but there is still a large segment of the population left out of financial services.

Among adults, 43.46 per cent of females are availing formal financial services, while 62.86 per cent of males have the access to formal financial services, according to Bangladesh Bank's financial inclusion report 2023. This manifests a prevailing gender gap in the financial-services sector of Bangladesh.

In 2023, some 32 per cent of men and 24.3 per cent of women took financial services from banks and financial entities, up from 30.9 per cent and 21.6 per cent respectively in 2022. It shows three-fourths of the population of this age group still remaining to be banked.

Upholding confidence of depositors is necessary to achieve the goal of financial inclusion and bring the unbanked population--especially the female segment--under formal channels of banking. The overall banking sector has also been plagued by scams during the past regime of Awami League, further eroding public trust in financial security.

Such a surge in such fraudulent practices triggering the erosion of confidence underscores the need for safeguarding users in the digital financial ecosystem. It may appear as a challenge in financial inclusion in Bangladesh.

Financial inclusion here remains heavily reliant on mobile wallets. Most of those online frauds use Mobile Financial Services (MFS) as an easy means to cheat. Women MFS account -holders are specially the targets of such fraudulence. Many unbanked females in the workforce would shy away from getting in the formal channel if such threats continue.

Entrenched cultural norms, patriarchal structures, and gender stereotypes, poor access to digital devices, high internet cost, insufficient network services kept many women unbanked. In many cases, family members stand as barriers, preventing women from owning financial accounts.

Thus, women continue to lag behind, despite making up nearly half of the population, with its adverse consequences. Long-term financial security of women is often compromised for a lack of financial accounts.

Female account-ownership in Bangladesh is 43 per cent, compared to the South Asian average of 66 per cent. A large portion of the female workforce, particularly in the informal sectors, still relies on Mohajon or local moneylender to borrow and deposit money. These intermediaries often exploit women, trapping them in cycles of debt.

The country's economic potential will remain constrained unless the government could safeguard financial products and introduce new ones such as SME-focused loans, and a dedicated regulatory and fiscal-policy framework etc.

Experts have long been calling for proper digital infrastructure and an interoperable financial systems for sustainable growth. Interoperability has led to significant financial- inclusion progress in neighbouring India. Similarly, integrating MFS into a proper regulatory framework could ensure transparency and consumer protection.

According to the Global Findex 2021, Bangladesh is lagging behind growth in account ownership, as of 2017-2021, than that of India. Account ownership grew from 31 per cent to 53 per cent in Bangladesh in 2017 -2021 period while in India it more than doubled from 35 per cent to 78 per cent.

However, several measures initiated by the central bank have now started paying off. Bangladesh Bank's Know Your Customer (KYC) framework and initiatives supported by institutions such as PRI and the Bill & Melinda Gates Foundation aim to enhance financial inclusion.

The National Financial Inclusion Strategy was formulated for 2021-2026, but it didn't effectively transform the financial landscape. Implementation phase of the NFIS is scheduled to end on June 30, 2026. The strategy defines financial inclusion as national definition for Bangladesh as: "Access of individuals and businesses including unserved and underserved to the full range of financial services facilitated with technology provided at affordable cost with quality, ease of access and scope of risk mitigation in responsible and sustainable manner through a regulated, transparent, efficient and competitive financial marketplace."

The first objective of the NFIS is to increase the level of financial inclusion (having at least one regulated financial service account) of all adults to 100 per cent by 2025 to be measured by a nationally authenticated evaluation framework with a view to moving towards 'cash-less society'. Other objectives include ensuring availability of a wide range of financial products and services capable of serving in different segments of the financial market and creating digital infrastructure including DFP, and fintech.

Reviewing and revising the strategy is imperative to ensure its implementation within a realistic timeline. Stakeholder consultations are crucial to identifying policy gaps and implementing key reforms.

Growing financial hardship has triggered rising income inequality, as reflected in ongoing protests and economic grievances before and after the mass uprising in July 2024. Women are always the worst victim to inequality and any disaster. Strengthening financial inclusion by integrating the underprivileged into formal financial channels can ensure equitable economic participation and reduce the size of the informal economy.

One of the key reasons for Bangladesh's low tax-to-GDP ratio is a vast informal economy. Investing in digital infrastructure and ensuring functional interoperability can facilitate the formalization of remittance transfers, a critical pillar of Bangladesh's economy.

Recommendations for strengthening financial inclusion: Enhancing digital security comes first. Strengthening cyber- security measures is to protect consumers from fraud and financial scams.

Gender-inclusive financial services is another must-do. It calls for developing financial products tailored to women, particularly in rural areas and among urban poor population.

Youth-centric financial products are needed for expanding financial services targeting young individuals entering the workforce.

Promoting financial literacy is no less important for the breakthroughs. Financial literacy programmes must be prioritized, as academic literacy alone does not ensure responsible financial behaviour. Corporate Social Responsibility (CSR) funds should be invested in financial-literacy initiatives.

Transparent and unified regulatory framework: Recent controversies surrounding Nagad have eroded public confidence in MFS. A transparent and standardized regulatory system is crucial for restoring trust in financial- service providers.

Encouraging competition in MFS: Currently, only 13 banks provide MFS services out of 62 licensed banks. Encouraging competition and ensuring women-centric financial services are essential for improving financial inclusion.

Ensuring financial inclusion will not only reduce the grey economy but also help the government mobilise higher domestic revenues. A well-regulated and inclusive financial ecosystem is crucial for Bangladesh's long-term economic stability and growth.

Last but not the least, a healthy and discrimination- free financial system can be an effective and efficient tool for women's economic empowerment which is a key driver to a country's economic growth.

doulotakter11@gmail.com