Financial inclusion demands a holistic approach

Sunil Sachdev | Tuesday, 22 December 2015

In today's business world, it seems you are either being disrupted or causing the disrupting. The role of the disruptor and news about their activities are being discussed, tweeted, reported, documented and shared daily, even if not clearly understood. Some of those reports, like the role of MNO-led financial service models as the disruptive agent to the traditional banking model (and a universal answer to financial exclusion and immobility) have been greatly exaggerated. This is mostly due to those looking to frame the conversation in disruptive tones instead of trying to understand the fundamentals of financial exclusion and immobility.

Significant press on the penetration of mobile devices (eclipsing the number of bank accounts) and the growth of mobile financial services (MFS) over the last few years has quickly led one to conclude that mobile network operators MNOs (mobile network operators) would play a leading role in accelerating the success of financial inclusion programmes. On the surface, the argument is pretty convincing. If people with incredibly limited resources are already buying billions of minutes through their phones at mobile agents, which outnumber bank branches, then we should be able to use the same underlying infrastructure to move money and make other transactions. Since MNOs have already reached the so-called "last mile", it makes sense that they could also bring financial inclusion to every home in every corner of the world.

The MNOs are happy to play the role of disruptor as it allows them to expand their business model into financial services which help mitigate declining rates for voice and data plans globally. The Telco industry and their surrogates have rallied around implementations of M-Pesa and bKash as proven points as to why regulators should evolve existing know your customer (KYC) policies to create a tiered account structure and a new banking licence category called "payment banks".

A closer look at M-Pesa, bKash and similar MNO-led MFS programmes around the world reveals that the results do not support the rhetoric. All MNO-led MFS success stories mask the fact that the money being moved on their platforms is primarily for top-ups and domestic remittances. In the countries where MFS providers have had success, like Kenya and Bangladesh, the markets are still largely cash-based, the platforms have not been able to scale and customers with mobile money or other tiered accounts are not graduating to true bank accounts. It is also evident that as much as MNOs claim they can access the last mile, they have no line of sight as to who is delivering the service on their behalf. Most MNO agents are not company owned and therefore over the counter cash (OTC) transactions at these agents become very difficult to monitor. Last, it appears that Telcos do not want to be banks anymore than the banks want to be Telcos.

These observations reveal the fundamental problem. The MNO-led solutions require MNOs and their agents to enable access to banking products and services that are beyond the scope of their core business. Continuing to position MNOs as the antidote to banks has made it very difficult to nurture the collaboration needed to deliver scale solutions that will truly solve the problem of financial exclusion and immobility.

Financial exclusion is a "square the circle" problem that can only be truly addressed by creating an ecosystem of banks, MNOs, corporations and individuals. Within this ecosystem, efficacy and scale is delivered by allowing each entity to operate within its own core competence, never outside. The sum of the whole is a sustainable symbiotic model. Banks continue to be the regulated entities trusted to provide relevant financial services, infrastructure and money movement. MNOs leverage their agent footprint for customer acquisition, literacy and servicing. Corporations develop merchant modernisation programmes for customer acquisition, literacy and servicing to create more efficient supply chains. Individuals are incentivised to help with customer acquisition and literacy in their own personal communities.

FIRST THINGS FIRST: DEFINE FINANCIAL INCLUSION: If we agree that the goal is financial inclusion, then we must also agree on what financial inclusion is and why it matters. For purposes of this article-and this is not an isolated point of view-we define financial inclusion as having access to savings, credit, insurance and payments. This definition has been widely linked to poverty reduction, women's economic empowerment and economic growth, so there is little wonder it sits high on the agenda of regulators in many countries.

MNO-LED MFS HAVE FALLEN SHORT OF FINANCIAL INCLUSION: Mobile money is a critical innovation, both in the adoption of mobile technology among low-income people and as a revenue stream for MNOs. However, the success of mobile money cannot be used as a rationale for financial inclusion policies led by MNOs for the following reasons:

n MNO-led MFS success stories cannot be defined as financial inclusion. The vast majority of MFS transactions are payment services - remittances and top-ups. Even within the most heavily adopted programmes, peoples' daily lives are still largely cash-based. Take a look at Kenya's M-PESA, widely touted as the gold standard for mobile money. Nearly seven in 10 adults in Kenya have access to M-PESA. Mobile money accounts for 66.56 per cent of the country's payments throughout volume and the amount sent through M-PESA is equal to 43 per cent of GDP (Gross Domestic Product). And yet, 98.2 per cent of Kenya's transaction volume is in cash and less than 1.0 per cent of low-income households' transactions are electronic. What is more, an enormous share (86 per cent) of the transactions carried out electronically are airtime top-ups.

n There is virtually no evidence that MNO-led financial services lead to financial inclusion. As already stated, payment services and financial inclusion are two very different things. People simply have not graduated from mobile money to more formal banking services.

n If MNOs were to provide the product and service lines necessary to achieve financial inclusion, they would need to be banks. Behaving like a bank means being regulated like a bank and it is naïve to think that MNOs would welcome that. There is always an argument to be made for relaxed guidelines. However, if prudent regulations are so arbitrary that they should not apply to MNOs, then governments should probably be looking at their policies for more reasons than financial inclusion.

THE SOLUTION: ALIGNING INCENTIVES OF KEY ECOSYSTEM PARTICIPANTS: Banks have the relevant products, experience with cash management and are regulated, while MNOs have the network to reach people in cost-effective ways.

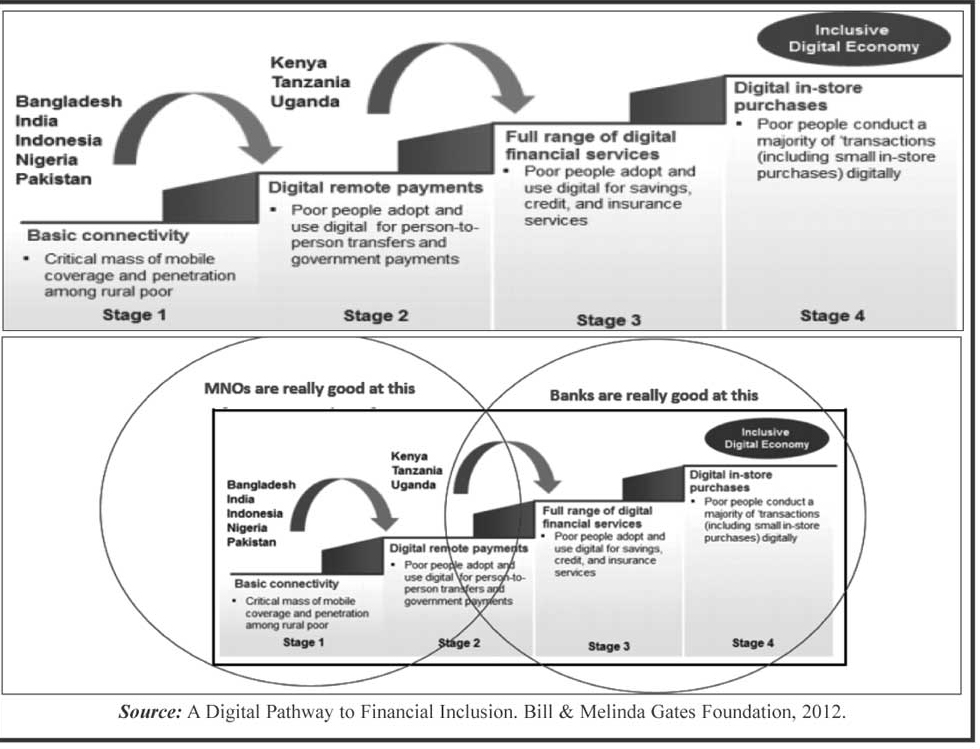

In its position paper "A Digital Pathway to Financial Inclusion," the Bill & Melinda Gates Foundation lays out a four-step process to digitally enabled financial inclusion. Stage 1 is mobile connectivity and stage 2 involves people adopting digital person-to-person payments. MNOs have shown they can do both of those things really well. This is not a surprise. Stage 1 is their core business and stage 2 is the monetisation of that connectivity-usage, top ups, bill pay. MNOs must perfect these stages just to stay in business.

Complications set in as we move toward more formal financial services. Stage 3 involves savings, credit and insurance services and stage 4 envisions a cashless payments infrastructure. This is not what MNOs do, and it is highly unlikely that they can achieve this themselves even if they want to.

From this perspective, it is easy to understand why banks and MNOs have not been able to deliver scalable solutions on their own. It seems more sensible simply to align incentives between banks and MNOs. Better yet, if we open up the ecosystem to other private-sector players and payment companies, could not we get to the inclusive digital economy with everyone earning more from a smaller share, given the scale benefits? There is plenty of opportunity for all ecosystem participants to benefit as long as everyone remembers that the best solution without scale will not get us any closer to the goal of solving financial exclusion and immobility for billions of people around the world.

THE LARGER ECOSYSTEM OF INCENTIVES: Much is written of banks facing pressure to deliver on financial inclusion targets. Often forgotten is the fact that banks, like MNOs, need to be profitable, and they will open new accounts when it is commercially viable for them. Likewise, MNOs want more people using smartphones for all their transactions, and the more utility in those handsets, the greater the voice and data revenue (as well as adjacent revenue opportunities). In other words, the right incentives will drive behaviour and will help ecosystem participants overcome many of the hurdles associated with scaling financial inclusion programs in the past.

IN BANGLADESH, BANK-LED MODELS CAN SCALE: The appetite for mobile financial services already exists in Bangladesh - mobile banking agents' number over 538,000 covering all regions, and serving a reported 28 million customers.

MNOs have established trust in communities related to basic mobile money services, but the kind of banking services demanded by financial inclusion do not belong to MNOs' core business. That is, and always will be, the preserve of the banks.

Bangladesh's current draft Regulatory Guidelines for Mobile Financial Services continue to be bank-led. We believe this is the right approach. Banks must lead the development of the system because the end-game involves products and services that banks are uniquely positioned and regulated to provide.

MNOs can reach the last mile, but can not deliver financial inclusion. Banks can deliver relevant banking products, but never had any incentive to reach the last mile. To have a real impact, all participants need to become part of a larger community that can help create benefits for everyone. We believe that is the only way to reach the scale needed to deliver meaningful results.

The writer is the Chief Sales Officer of GlobeOne.

ssachdev@globeone.com