Fraudsters gobble up Tk 926m in 2025

They are still active though BFIU, CID working to tackle financial crimes: BB official

SAJIBUR RAHMAN | Tuesday, 16 June 2026

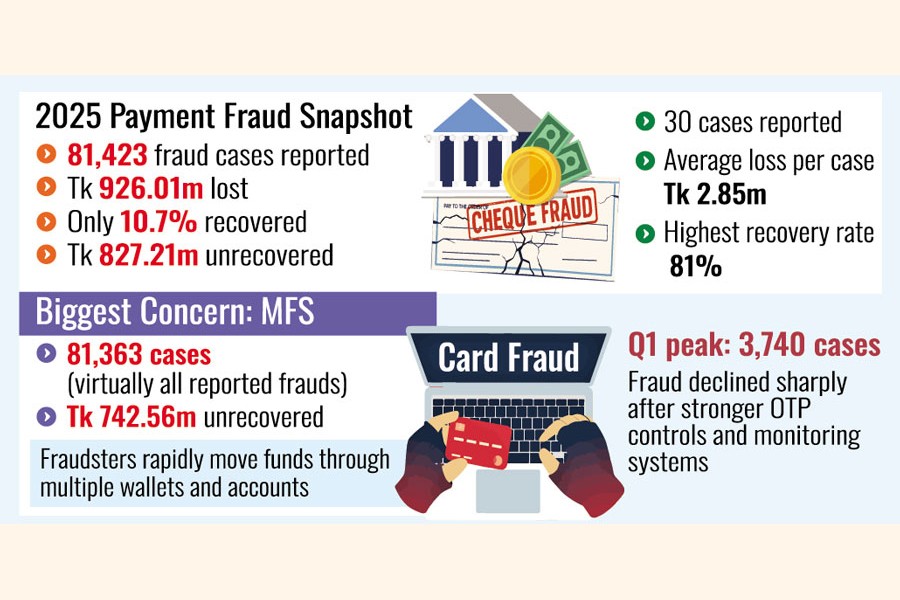

Bangladesh's payment ecosystem suffered losses amounting to Tk 926.01 million due to fraudulent practices in 2025, with mobile financial services (MFS) accounting for the major part of it.

Such a significant volume of fraud-related losses highlights the persistent vulnerabilities in the country's fast-growing digital finance sector, according to insiders.

According to Bangladesh Bank (BB) data, a total of 81,423 fraud cases were reported across mobile financial services (MFS), cheque-based instruments and card transactions during the year.

Of the total fraud amount, Tk 827.21 million remained unrecovered, leaving an overall recovery rate of only 10.7 per cent.

The central bank data show stark variances in fraud patterns across payment channels.

While MFS fraud was widespread and difficult to recover, cheque fraud occurred infrequently but involved large amounts per incident. Card fraud, meanwhile, remained comparatively contained and showed signs of improvement during the year.

MFS emerged as the most vulnerable segment, accounting for about 88 per cent of the total fraud value recorded in the payment ecosystem.

The sector experienced fraud worth Tk 813.26 million in 2025, of which Tk 742.56 million remained unrecovered. The recovery rate stood at only 8.7 per cent, According to available data.

The number of fraud cases rose from 16,230 in the January-March quarter to a peak of 18,623 in April-June before gradually declining toward the end of the year. Fraud values followed a similar trend, reaching Tk 219.87 million in the second quarter.

Industry observers said the low recovery rate reflects the speed with fraudsters moving stolen funds through multiple accounts and intermediary wallets before victims or service providers can take action.

Although cheque-related fraud represented only a small share of total cases, it remained a significant source of financial risk because of the high value involved in each incident.

A total of 30 cheque fraud cases involving Tk 85.53 million were reported during 2025.

The average loss per incident amounted to nearly Tk 2.85 million, underscoring the high-value nature of cheque-related fraud.

Unlike MFS fraud, cheque frauds demonstrated strong recovery outcomes with financial institutions managing to recover about 81 per cent of the affected funds, making it the most recoverable fraud category among the three payment channels.

The first quarter recorded the highest cheque frauds valued at Tk 36.59 million, largely due to a handful of major corporate cheque misuse incidents.

Banking officials attribute most of the cheque fraud cases to forged instruments, documentation irregularities and weaknesses in internal control mechanisms.

Although cheque fraud does not currently pose a systemic threat, people familiar with the development warn that it would require continued monitoring because a small number of incidents can generate substantial financial losses.

They recommend strengthening branch-level verification processes, introducing image-based cheque analytics and reinforcing dual-control mechanisms to reduce operational and insider risks.

On the other hand, card fraud followed a markedly different trend during the year as the segment witnessed its highest level of fraud in the first quarter, when 3,740 cases involving Tk 26.5 million were reported.

Both the number and value of fraud incidents then fell sharply in subsequent quarters.

Fraud cases dropped to 1,717 in the following quarter, while losses fell to less than Tk 0.7 million. Although fraud activity increased modestly later in the year, it remained far below the levels recorded at the beginning of 2025.

Such a sharp decline suggests that stronger fraud-monitoring systems, stricter one-time-password (OTP) enforcement and improved merchant controls have helped curb fraudulent activities.

Card fraud achieved a recovery rate of about 47 per cent, significantly higher than that of MFS but lower than cheque fraud.

While card fraud remains operationally manageable, experts believe continued vigilance is necessary, particularly as e-commerce and cross-border digital transactions continue to expand.

Arif Hossain Khan, Executive Director of Bangladesh Bank, acknowledged the rise in payment-related fraud but said the central bank is intensifying its oversight efforts.

"Our Payment Systems Supervision Department remains actively engaged in monitoring the sector and conducts regular sample-based inspections," he said.

He warned that Mobile Financial Services (MFS) providers stand to suffer the most if they fail to curb such fraud.

"If MFS operators cannot reduce fraud incidents, they will be the biggest losers because their reputation and customer trust will be severely affected," he said.

Khan said relevant agencies, including the Bangladesh Financial Intelligence Unit (BFIU) and the Criminal Investigation Department (CID), are also working closely to tackle financial crimes.

"We are making every effort, but some criminals still remain active in society," Mr Khan said.

He also emphasised that fraud cases remain relatively low compared to the overall volume of digital transactions.

Fahim Mashroor, the founder of BDJobs, recently raised serious concerns over the security and growing vulnerabilities in the financial sector.

Mentioning that there has been a massive influx of fake Mobile Financial Services (MFS) accounts and fake SIM cards in the market, he warned that the recent withdrawal of taxes on SIM cards would compound the issue.

He criticised the central bank for its failure to penalise non-compliant MFS providers and banks.

Local financial institutions currently operate without any fear of accountability, he noted.

Mashroor emphasised that both MFS providers and banks need to adopt state-of-the-art technology to check financial fraud.

sajibur@gmail.com