Dynamics of insurance sector

Getting ready for post-LDC era

Md Khaled Mamun | Tuesday, 1 March 2022

Bangladesh as a nation state has long been cherishing its graduation from the 'least developed country (LDC)' status. 2026 is going to be that milestone year in our history. The UN put Bangladesh in the least developed country (LDC) group in 1975, with the poverty rate at 83 per cent. The percentage of the populace living in poverty decreased significantly over the decades and now it stood at 20.5% in the fiscal year 2019-20. After 45 years at its 76th session (40th Meeting of 24th of November 2021), the General Assembly of the United Nations has passed the resolution for allowing Bangladesh to graduate to a developing country, with a five-year preparatory period leading to this graduation by 2026, which would, beyond doubt, be the momentous event for each and every Bangladeshi.

After 45 years at its 76th session (40th Meeting of 24th of November 2021), the General Assembly of the United Nations has passed the resolution for allowing Bangladesh to graduate to a developing country, with a five-year preparatory period leading to this graduation by 2026, which would, beyond doubt, be the momentous event for each and every Bangladeshi.

Optimistically enough, this graduation will directly upgrade "sovereign credit rating," an indicator of creditworthiness as an international financial player in the domains of banking, insurance and reinsurance.

In the post-graduation period the country will have to entice foreign direct investment (FDI) for shifting of the industry composition from light to heavy, and simultaneously to diversify the total exports based on the knowledge economy, an economic ecosystem, in which the production of goods and services hinge on knowledge-intensive activities that contribute to advances in technological innovation.

In this regard the insurance sector being central for all socio-economic development has to be ready for the changes as well as challenges ahead. In this essay we will delve deep into the dynamics of our insurance sector for preparing it for the post-LDC graduation scenario:  PROMULGATION OF ANNUAL ACTION PLAN ON THE NATIONAL INSURANCE DAY:

PROMULGATION OF ANNUAL ACTION PLAN ON THE NATIONAL INSURANCE DAY:

From the 1st of March of 2020, Government of Bangladesh celebrates National Insurance Day. Bangabandhu Sheikh Mujibur Rahman, the Father of the Nation, joined Alpha Insurance of the then East Pakistan on March 1, 1960. The government declared March 1 as National Insurance Day to commemorate the advent of Bangabandhu in the insurance industry.

This day was created to honour the contributions of insurance professionals and to promote the industry as a whole. The goal of National Insurance Day is to educate the public about the important role that insurance plays in our society, and also to provide an opportunity for insurance companies and professionals to network with each other. On the occasion, all parties concerned should promulgate the annual action plan (quarterly target oriented) for development of the sector. Only then this celebration would bear the desired fruits.

NO CORRELATION BETWEEN GDP GROWTH AND INSURANCE:

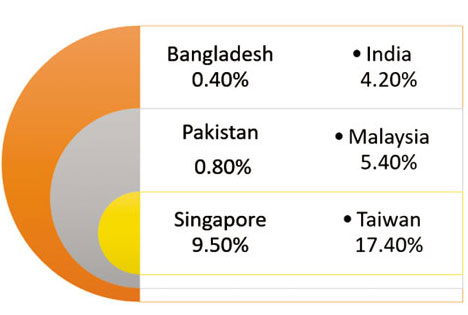

According to the 'World Economic Forum', by 2030 Bangladesh will be the 24th largest economy in the world, for which it is high time for all of us to prepare, and in this regard our insurance sector has much to do on the premises, as the insurance sector's share in the GDP in 2020 was very nominal--0.29% by Life, and 0.11% by Non-life, totalling 0.40% (defined as Premiums / Gross Domestic Product).

We stand in the 69th position in the world market in terms of premium volume for the year 2020, since our insurance market has not been growing at a rate that is, at least, close to steady GDP growth rate in the last decade.

INCORPORATING SUCCESSION PLANNING AND KNOWLEDGE MANAGEMENT

Knowledge management department is to focus on succession planning and documentation of institutional knowledge reaching out to the retired employees. This practice will ensure the dissemination of the company's core knowledge to the newly-appointed employees. All the retiring experts need to be engaged in classroom teaching, instructional approach, learning, gamification, peer-to-peer learning and mentoring. So, the culture of succession planning should be embedded in the corporate culture of our insurance companies.

ESTABLISHING CHARTERED BODY FOR CREATING PROFESSIONALS

In Bangladesh, the Institute of Chartered Accountants of Bangladesh (ICAB), Institute of Cost and Management Accountants of Bangladesh (ICMAB), Institute of Chartered Secretaries of Bangladesh (ICSB) create professionals like Chartered Accountants (CA), Cost & Management Accountants (CMA), Chartered Secretaries (CS) for the financial services industry of the country.

Contrary to the common understanding, no such professional body has been set up in the country for creating 'Chartered Insurer (CI)'. Therefore; IDRA needs to initiate the establishment of a chartered body for the insurance practitioners. Bangladesh Insurance Academy can be upgraded to an institute of international standard.

It is fortunate for all insurance professionals in the sector that the Financial Institutions Division of the Finance Ministry formed a five-member committee in November 2021 in order for setting-up 'Bangabandhu Insurance Institute' (BII), which is going to be the premier insurance education institute in the country.

It is anticipated that the BII will produce 'Chartered Insurer' designation holders, who will meet the skill demand of the local insurance market and also will work aboard in the international insurance and reinsurance companies. Moreover; the BII will definitely impose 'Code of Conduct' guide for the member professionals.

DIGITAL MARKETING FOR BETTER INSURANCE PENETRATION:

Digital marketing in insurance is the process of engaging with the prospects to create awareness and drive action. It is a fluid and ever-changing field as new technologies continue to emerge, so it is important for those in the insurance industry to stay up-to-date on how consumers are responding to these changes.

The focus on the digital technologies is no more an option for our insurers, it's a survival issue. For achieving an enhanced insurance penetration rate in Bangladesh, insurers should put their best efforts in making proper use of digital blessing and proudly contribute to the making of 'Digital Bangladesh'.

The provision 19.7.21 of Insurance Core Principles (ICP) also allows insurance operators to serve the clients using digital platforms. The section reads "In conducting insurance business through digital channels, insurers and intermediaries should take into account the specificities of the medium used, and use appropriate tools to ensure that customers receive timely, clear and adequate information that helps their understanding of the terms on which the business is conducted".

FINANCIAL SERVICES COMPENSATION SCHEME (UK):

The Financial Services Compensation System (FSCS) in the UK exists to protect clients of failed financial institutions in case of the clients going to be deprived of the valid insurance claims. If the company encounters financial trouble and isn't able to meet customers' financial obligations, then FSCS, being fully funded by the financial services industry, steps in to provide a financial reimbursement to the claimant, of course within a specified threshold of compensation amounts. As a would-be developing nation, the similar arrangement may be introduced in Bangladesh's insurance sector in order for consumers' trust building. This compensation scheme needs to be introduced, led and supervised by the regulatory body.

NECESSITY OF COMPULSORY AUTOMOBILE INSURANCE:

In all countries across the world, it is required by law to have automobile insurance if you own and operate a vehicle. Since 2019, this is not the case in Bangladesh, for example, it is not a requirement to have automobile insurance. The purpose of having automobile insurance is to protect yourself and your vehicle if it were to be stolen or damaged in an accident. Auto insurance provides financial protection for the owner of a vehicle in case of an accident or theft. This is especially true for Bangladesh, which has a high rate of automobile accidents and thefts. According to the World Health Organization, Bangladesh had the second-highest rate of traffic accidents among all countries in Asia. So, the regulatory body should take necessary steps to reintroduce compulsory motor insurance. Unfortunately, in the absence of motor insurance, even an innocent passer-by facing a motor car accident is no more protected in our country since the abolition of compulsory motor insurance back in 2019.

SETTING UP OF AN INSURANCE INFORMATION DATABANK:

There is the dearth of market information relating to life insurance and non-life insurance, which impedes a small-scale research. As a result; conducting insurance research activities is almost impossible here in Bangladesh. For instance; here we cannot find the updated mortality and morbidity tables which is vital for determination of pricing structures for life insurance.

Thus, it is high time to set up an insurance information bank, that will for sure help people make educated decisions, manage risk, and appreciate the essential value of insurance. It is known to all that the underlying principles of life insurance underwriting is the demographic assumption, which is de facto reliant upon the mortality table of the country.

An updated mortality table helps insurers determine the cash flow with precise accuracy. In the past 10 years the government adopted successful measures for improvement of life expectancy. Such achievement has not been duly reflected in our mortality table.

ROLE OF RESPONSIBLE INSURANCE NEWSPAPER FOR MARKET DEVELOPMENT:

Insurance newspapers are one of the most important sources of information for the general public. They play a vital role in informing the public about important events happening in the insurance world and in their own country. Insurance newspapers also provide a forum for public debate and discussion on important issues. In addition, insurance newspapers can be used to promote positive social changes and benefit the community. It is a very useful tool for research, communication and education. In our market there is hardly any dedicated insurance media to cover the insurance market in the positive manner.

CONCLUDING REMARKS:

There is no denying the fact that all of 17 goals of the 2030 UN Agenda for Sustainable Development have relevance to insurance products and services. So, we have no other alternative but to endeavour to develop our insurance sector paying due attention to creating a prudential regulatory framework, product diversification, and human capital investment.

For bringing the desired level of changes to the insurance sector, in association with World Bank, the Government of Bangladesh has devised a project costing USD 76 million for development of the country's insurance sector. The main developmental objectives of the World Bank's project include a. strengthening the institutional capacity of the regulatory body; b. strengthening the institutional capacity of 02 (two) state-owned insurance corporations (JBC & SBC); and c. creating awareness about insurance products and services among the people.

On the top of the above initiatives, the private insurers being the majority stakeholders need to devise their respective strategy, as a part of nation-building activities, in the light of 'National Insurance Policy 2104' for advancement of the insurance sector as a whole with a view to confronting the challenges to be posed by graduation from the LDC club by 2026. This preparedness will resultantly lead us to stay tuned with the government's Vision 2041 as well.

Md Khaled Mamun, FCII (UK) is the Chief Executive Officer of Reliance Insurance Limited, and an associate member of Bangladesh Insurance Academy, and also a fellow member of the Chartered Insurance Institute of the United Kingdom.