Getting startup valuation right

Kamrul Arefin | Tuesday, 10 November 2020

![]() Startup valuation is such a thing that often has no objective method or rational criteria, especially if it is a pre-revenue startup. If you try to think about startup valuation techniques by the linear logic of market peer group comparison or any fixed valuation method like DCF (Discounted Cash Flow) you will feel an apparent lack of rhythm from different startup to startup. Here is a simple example why:

Startup valuation is such a thing that often has no objective method or rational criteria, especially if it is a pre-revenue startup. If you try to think about startup valuation techniques by the linear logic of market peer group comparison or any fixed valuation method like DCF (Discounted Cash Flow) you will feel an apparent lack of rhythm from different startup to startup. Here is a simple example why:

Startup 1: Startup 1 has no traction, no minimum viable product and no revenue. They raise money on a Tk100 million (10 crore) pre-money valuation.

Startup 2: Startup 2 has minimum viable product traction and strong founder's background. They raise money on a Tk20 million pre-money valuation.

What could possibly be the reason? It is because the startup world is full of surprises, secrets and opportunities. This universe stands on opportunities and secrets that are perceived differently from person to person. And these opportunities are hard to measure quantitatively until the series A stage. The only people, who get the opportunities are the founders, the employees and the investors who trust them.

So first of all, what the valuation methods are out there by which we can value a company. Here's a graph from the Corporate Finance Institute:

But most of the time we cannot value a pre-revenue startup company by these traditional valuation approaches like we do for established companies with track record or exchange listed companies. This is because: 1. At the initial stage, there is no cash flow or revenue or profit track record. It is difficult and sometimes vague to project the future cash flow or profitability to find the inherent value of a startup.

1. At the initial stage, there is no cash flow or revenue or profit track record. It is difficult and sometimes vague to project the future cash flow or profitability to find the inherent value of a startup.

2. Often it is difficult to find comparable companies, because most of the time if a startup is going to raise funds and VC agrees to give a cheque is because it has a unique value proposition or distinct point of difference.

3. Often tech startups have no tangible asset rather they create value by their team qualification and opportunity inherent in the idea. So the cost approach of tangible assets is totally misleading. So, the valuation for a startup is an intuitive thing.Here are some methods that help value startups even from the idea stage, but remember neither of them are foolproof methods.

So, the valuation for a startup is an intuitive thing.Here are some methods that help value startups even from the idea stage, but remember neither of them are foolproof methods.

Scorecard Method

This method is popular between angel investors.

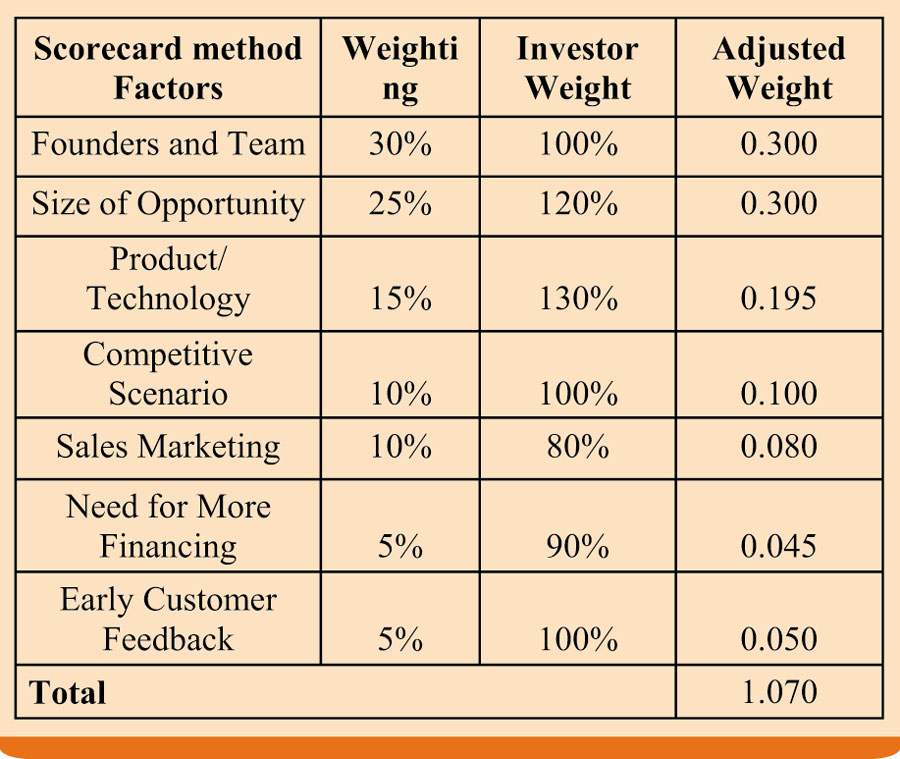

The first step is to look for average pre-money valuation of pre-revenue startups at a similar stage in the similar industry in the similar region. Then look at the factors of a new business idea in a valuation scorecard. The factors can be industry attractiveness, market size, quality of the management team, etc. The main parameters, or criteria, of the Scorecard Method, in order of importance, along with their respective weights, are: entrepreneur, team, board (30 per cent), size of opportunity (25 per cent), product/technology (15 per cent), sales/marketing (10 per cent), need for more financing (5.0 per cent) and other (5.0 per cent). Angel investors can change these weighting or can also add or deduct parameters based on their own preference and insight.

Now an angel investor can arrive at a pre-money valuation of the targeted startup by multiplying the total adjusted weight (1.07) with the average pre-money valuation of similar pre-revenue startups.

Berkus Method: This is another intuitive method for exclusively pre-revenue startups. Berkus method takes startup as a basket. An investor will value a startup based on the contents in the basket when it's at the pre-revenue stage. The contents are: A. Sound Idea (Basic Value) B. Prototype (Technology) C. Quality Management Team (Execution) D. Strategic Relationships (go-to-market) E. Product Roll Out (Sales)

Now investors will give different values to each of these contents and will reach a final value of the basket by summing values of all contents. The amount of value an investor puts depends on his personal judgment, industry, location and ecosystem the startup is operating in.

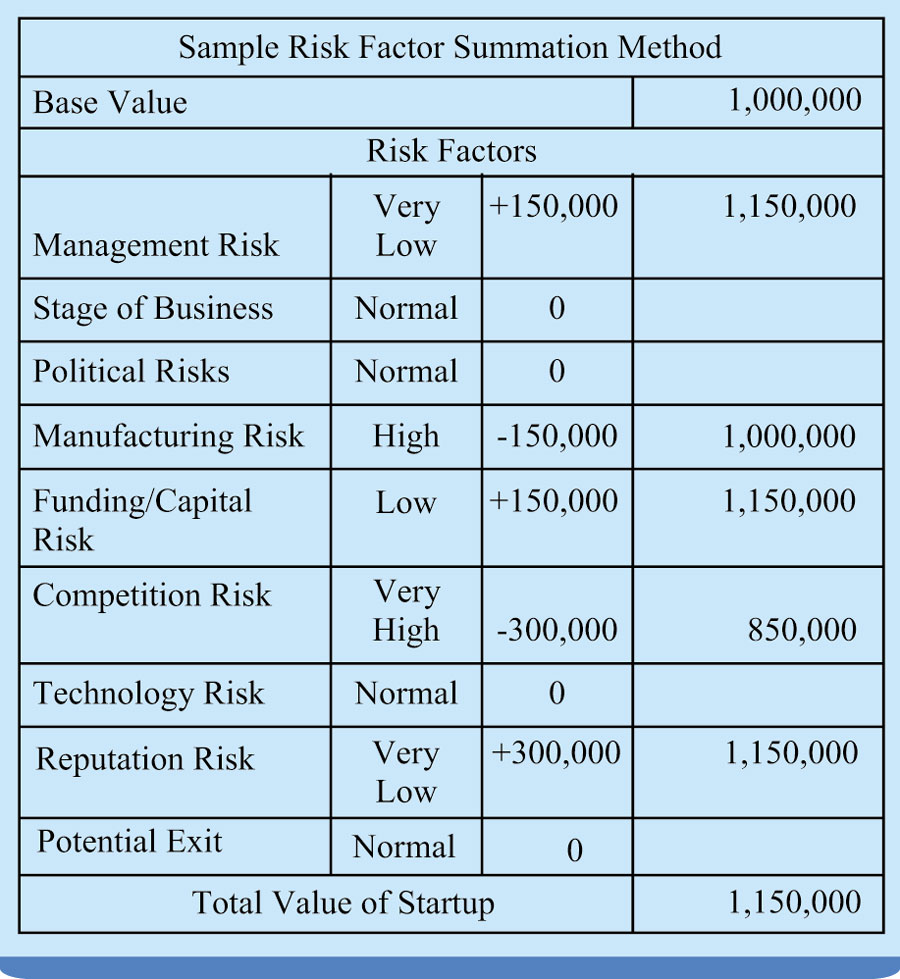

Risk factor summation method:

This is another pre-revenue startup valuation method, but a more evolved version than the Berkus Method. Based on assumption of base value of startup, adjusted value is calculated based on several risk factors. The base value is determined based on the average value of similar startups in the area, which is often very difficult to determine. The risk factors are tagged from very low to very high.

VC method

This method is mostly used by venture capitals and can be used for both pre-revenue startups and post-revenue startups. It is one of the most popular methods for establishing pre-money valuation of companies.

Exit value is the anticipated selling price of the company at some point down the road. It can be determined by multiplying company projected earnings by industry average PE multiple, projected revenue by peer group revenue multiple or multiplying company projected EBITDA by industry average EV/EBITDA multiple. Return on Investment (ROI) is calculated by hurdle rate that is calculated by adjusting required rate of return by VC's subjective judgment on probability of success.

ROI= (1+hurdle Rate)^t

(1+hurdle rate)^t = (1+required rate of return)/probability of success

Exit Value = ROI* Post Money Valuation

Now if exit value is divided by ROI we can reach a post-money valuation of the company.

Post money valuation= exit value/ROI

DCF method

DCF method is basically not recommended for a pre-revenue startup for the reasons already explained. There are a lot of uncertainties for a pre-revenue startup due to their high probability of failure and unique model. Also, there is no track record of revenue or earnings to project the free cash flows for DCF estimation. If someone uses the DCF method for valuing a pre-revenue startup then it is highly recommended to use it by calculating different scenarios. For instance, estimate different probability of success for the startup - very high, very low and normal.

A startup valuation is difficult to measure by the traditional valuation matrices. For an example of the formulas and methods, we use for the valuation of public companies listed on stock exchanges.

So which method is the best? The answer is neither. Valuation is most of the time an estimate based on probability of an opportunity to become successful. In short it's a guessing game.

Basically, the correct valuation is something that supplies funds to an entrepreneur to reach milestones, which both the investor and entrepreneur agree within a specific timeframe and the dilution is limited to a level, where the fund raised is more benefitting to the company than it is demotivating to the entrepreneur due to dilution.

................................................

The author is Co-Founder & CEO, SVP Limited.

arefinjobs@gmail.com