Global shocks: the economic impact

Hasnat Abdul Hye | Sunday, 19 April 2026

It has become customary to disaggregate the impact of economic shocks on the global and national or regional economies. Needless to say that in broad terms the conclusions are the same in broad terms pointing to the same direction viz decline. While the world economy is the composite of all regional and country-wide developments, individual economies try to cope with the shock using their capacity for resilience. In the event, the world economy can do little on its own to change the emergent economic trends and depend on the performance of individual economies to make economic updates. Multi-lateral institutions like the world Bank, the International Monetary Fund (IMF), the World Trade Organization (WTO) and regional institutions like Asian Development Bank (ADB), African Development Bank (AfDB), BRICS etc can step in to perk up the world economy and thereby help individual economies to recover from the adverse impact of the shocks. But if the economic shocks emanate from geopolitical developments, prompt and united decisions in multilateral institutions are most likely to bog down.

Five global shocks: In the 21st century five economic shocks have been generated, four of which are ‘man- made’ and one natural. The first is the financial crisis of 2006-07 that broke out in America and Europe due to undue exuberance in investment banking in America’s mortgage sector. It was not of global import and was managed by co-ordinated policy interventions by G- 7 countries. The second economic shock came with the Covid pandemic in 2020 and its impact was global, leaving no country untouched and immune from its fallout. It was both natural and man-made in so far as the dissemination of the virus was due to human negligence. It battered all the economies in varying degrees and subsequently adversely impacted on global economy by disrupting the supply chains and increasing costs of shipping. Many countries are still struggling to recover from the ravages of Covid pandemic, so deep and wide-spread has been its impact. Even before the recovery from Covid was complete the global economy was suddenly subjected to a man- made catastrophe, the Ukraine war. It immediately adversely impacted the supply of gas, oil, fertilizer, wheat and corn, increasing their prices. Individual economies are still reeling from the blows dealt out by the Covid and Ukraine war.

The fourth economic shock of this century is entirely man-made and done in a most arbitrary manner. By raising tariff sky-high across the board and slapping it on all countries almost overnight, the Trump administration made mincemeat of rule-based global trade and made economies of individual countries hostages to an ultra- nationalist policy of balancing trade accounts by neo-mercantilist America. The global economy and the individual economies are still in the process of adjustments (mostly in the form of concessions made to strong arm tactics of American demands) and is now faced with an economic catastrophe of most serious consequences, the preemptive war against Iran by America and Israel .

ImPact on GLOBAL ECONOMY: The six weeks war in Iran, now in the last phase of a tenuous ceasefire, can have more far reaching consequences than all previous shocks to which the global economy has been exposed. This is because the Gulf countries are sources of supply of liquefied natural gas (LNG) to both European and Asian countries. Damages to LNG sites in the Gulf reportedly are so severe that resumption of exports after the war ends will take up to one year. Longer the war wages greater will be the time lag between reconstruction of facilities and resumption of supplies. The Gulf countries also export fertiliser to Europe, Africa and Asian countries. It is estimated that up to 46 per cent of global traded urea fertiliser is linked to Gulf producers. The shortages of fertiliser caused by the war in Iran have already led to estimates that these may reduce food production by as much as 25 per cent this year. Apprehending this, food markets have already registered 5 per cent higher prices.

Iran has the third largest oil reserves in the world, next to Saudi Arabia and Venezuela. It exports 90 per cent of its oil to China which accounts for 11 per cent of latter’s total requirement. Disruptions in this supply will have some impact on China’s economic growth. Other importers of Iranian oil like India, Bangladesh and Myanmar will also face similar problem. Besides Iran, the Gulf countries supply about 20 per cent of global oil through the Strait of Hormuz. After the start of the Iran war this supply has stopped, compounding the crisis in the global energy market. Price per barrel of Brent crude oil shot to $ 120 in the first week of the war and is now hovering around $100. Volatility in energy markets has severely jolted all the economies of the world.

Increase in the price of oil has led to increases of prices of almost all commodities causing rise in cost of living. Inflation, brought under control in many countries through tight monetary policy over the past several years, has staged a comeback. This in turn has made it difficult for central banks to lower the policy rate, a situation that is not conducive for investment. Inflation and high interest rate has affected stock markets adversely with investors switching from stocks to treasury bills and bonds.

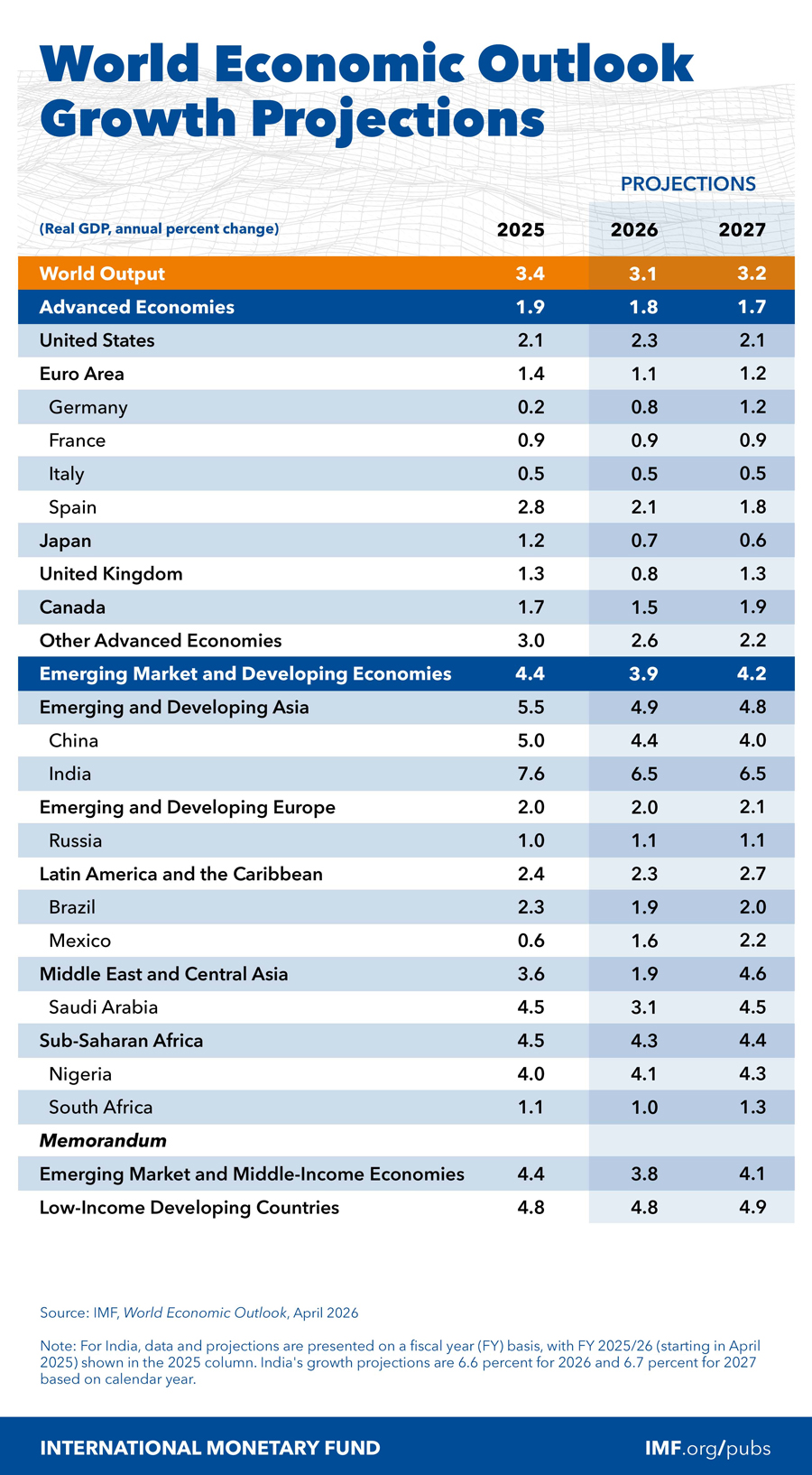

The cumulative effect of all the above has been reflected in a downgraded growth forecast for the world economy. For the current calendar year, the IMF has brought down the estimate for global growth from 4.0 per cent to 3.1 per cent. This is on the basis of the current state of the Iran war. If it prolongs and spreads out geographically, the growth prospect will worsen, requiring the rate to be further downgraded.

All global shocks do not affect every country to the same degree. Particularly vulnerable are the developing countries. While industrially developed countries have deep pockets or can borrow, developing countries can borrow only at the cost of inflation. Providing them with budgetary support in the form of soft loan can go a long way in helping them to cope with the economic shocks. The World Bank, the IMF and other multilateral institutions can play important roles in times of Economic crisis. This role becomes incumbent upon them once they update the economic outlook and downgrade growth estimates of individual countries..

Impact on regions: (A) The economic impact of the war launched by America and Israel been has been immediate and most extensive in Iran. Not only numerous military targets, including armament industries, have been destroyed by bombing, even civilian infrastructures like schools, hospitals, universities, scientific research facilities, bridges and rail tracks have not been spared. Donald Trump has publicly threatened to bomb Iran back to the stone age, a declaration unheard of from the head of a state before. According to Iran Revolutionary Guard Corps (IRGC) the country has already suffered a loss $22O billion as a result of bombings by America and Israel. In terms of loss of exports of oil, the estimated amount is about $276 million per day while total economic loss, including petrochemicals and knock-on effects is estimated to be $435 million dollars per day. If the war stops now it will take 10 years for Iran to complete reconstruction, costing between $300 to $400 billion, according to one estimate.

The oil and gas assets of Gulf countries and Saudi Arabia have been inflicted heavy damages by bombings by Iran as part of its asymmetric strategy. It is estimated that GDP of United Arab Emirate (UAE) and Saudi Arabia may decline by 3 and 5 per cent respectively. Kuwait and Qatar, on the other hand, will see greater decline in their GDP, by 14 per cent according to one estimate. Many of the Gulf countries are already facing economic recession as their tourism industry has collapsed after the war broke out. The investment climate in these countries has darkened as investors are retreating due to lack of trust and confidence. The greatest and long lasting damage suffered by the countries in the region, including Iran, will be environmental. As a result of bombings of oil refineries and gas fields toxic gas has already polluted air while chemicals (greenhouse gas amounting to 2000 million tons) used by American bombers have polluted surface water. It is suspected that uranium hexafluoride from Natanz nuclear enrichment facility may have polluted soil after bombing by America, making agriculture highly risky.

(B) The Asian Development Bank (ADB) has predicted the war in Iran is likely to drag on Asia’s economies over this year and next. It estimated the region’s growth at 5.1 per cent during this period. Growth predictions could fall to as low as 4.7 per cent for 2026 should the US-Israeli war with Iran drag on into the third quarter. ‘Most economies in developing Asia and Pacific will see their growth outlook worsen this year and in 2027’ has been the Bank’s stark assessment. The region’s status as a net energy importer left it particularly vulnerable to the wars’ fallout, said the ADB chief economist recently. Even after energy prices normalise, supply- chain disruptions, higher producer price and tighter financial conditions would prolong stagflationary pressures, he added. A more drawn-out conflict in the Middle-East could also see prices spike by as much as 5.6 per cent, the ADB report observed. Completed in March, the, Bank’s report had predicted price rise of 3.6 per cent in 2026 and 3.4 per cent in 2027 under what it described as ‘early stabilisation scenario’. The report noted that Iran’s squeeze on shipping route in the Strait of Hormuz, had ripple effects far beyond the gas pumps, including regional food security.

Bangladesh case: The World Bank has drawn a conservative economic outlook in its Bangladesh Economic Update released in the first week of April. it shows the country can grow at 3.9 per cent in the current fiscal for the compounding effects of the of the on-going Middle-East conflict and persistent domestic macroeconomic fragilities. But the ADB in its Asian Development Outlook (ADO) raises hopes that the on-going financial sector reforms aimed at enhancing stability, transparency and efficiency should support economic expansion. ADB’s ADO for April, 2026 says that following a period of recovery phase, GDP growth is expected to rise over the next two fiscal years. According to the ADO for April 2026, the country’s GDP is to grow 4.0 per cent in FY2026 and further accelerate to 4.7 per cent in FY2027, up from a sluggish 3.5 in FY2025. The ADB projection is too optimistic and does not chime with results of previous reform measures and growth performance. The World Bank estimate is more realistic, given our past experience.

According to newspaper report, the present government plans a big budget worth Tk 9.30 trillion for the next fiscal year for augmented funding of critically important sectors. In order to finance the substantially raised annual spending plan, the government has set a target to collect Tk 7.95 trillion as revenue in fiscal 2026-2027. (Financial Express, 13 April, 2026). Given the past record of public resource mobilisation one can safely conclude the government will have to resort to bank borrowing making the target of bringing down inflation to 7.9 per cent unrealistic. What is most glaring in these pre-budget deliberations is the absence of factoring in the Iran war in the sectors concerned and delineation of a plan action for each. The energy crisis created by the war is not only a problem of expanding subsidy to cushion the effects on consumers but also calls for support to producers, ranging from farmers to industrialists. A holistic study analysing the ramifications of the energy crisis is urgently called for. The next budget should focus on energy crisis and its ramifications in the economy.

hasnat.hye5@gmail.com