Into the new NBR oversight regime

Doulot Akter Mala | Sunday, 22 November 2015

Bangladesh has introduced a new oversight regime this year to scrutinise all the cross-border financial transactions. The enforcement of the Transfer Pricing law under the income tax ordinance would enable taxmen to monitor the international transactions by the multinational companies from Bangladesh.

The National Board of Revenue (NBR) started compiling all the statements on international transaction (SIT) for the first time. It is collecting the data from field-level tax offices across the country.

According to the Income Tax Ordinance 1984, section 107 EE, and Income Tax Rules 1984, rules 75A, taxpayers having international transactions have to submit SIT to respective tax offices.

The country will be able to know how many and how much volume of cross-border transactions was conducted in FY 2014-15. Currently, there is no such data available to the tax department of the government.

There is a cell for TP that will maintain the data and proceed with the information for further scrutiny. The cell will profile and conduct audit on the basis of the data that would be collected by the field-level tax offices.

The journey of transfer-pricing cell started this year although the law came into effect in July 2014. However, the TP law was passed by Parliament through the Finance Bill 2012.

The income-tax wing of the NBR has sent a prescribed format for furnishing SIT data to the field offices. Name of taxpayers, taxpayer's identification number (TIN), tax zone and circle, date of income-tax-return submission and date of SIT submission will be in the SIT.

MNCs have to submit their SIT they conducted in Fiscal Year (FY) 2014-15. The TP cell would scrutinise income-tax returns, to be submitted in 2015-16, containing cross-border financial transactions. According to the tax officials, the TP cell will initially adopt a go-slow policy and start full sewing operation in next two-three years.

A watchdog team of the NBR, comprising seven skilled tax officials, is working in the TP cell to check transfer mispricing by the corporate taxpayers.

According to the initial data, there are some 175 MNCs operating in Bangladesh and they would come under TPC scanner.

The NBR has issued a TP rule that has given detailed guidelines for maintenance of accounts and records of the MNCs. Particulars of international transactions, tangible property of revenue and capital nature of transaction should be furnished in a prescribed form.

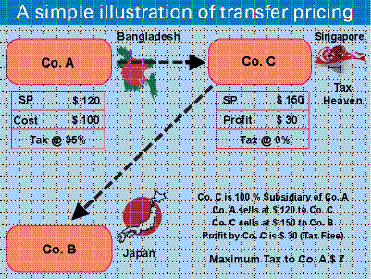

Cross-border financial transaction conducted by the multinational companies is a major global concern in recent times. In Bangladesh, high rate of corporate tax drives away profit of the MNCs to other countries having comparativly lower tax rates.

Many companies are discouraged from showing their actual profit as they have to pay corporate tax at a higher rate. Inflated prices of products and raw materials, consultancy charges and other means have been shown for transfer mispricing.

The highest corporate tax rate is 45 per cent in Bangladesh. Experts said the actual tax incidence is much higher on taxpayers as taxmen disallow many of the claimed expenditures of the taxpayer.

Taxmen in the TP cell are working for determining the prices. They will send report to the field-level tax offices to complete assessment on the basis of decision.

Transfer pricing is a major tool used for corporate-tax avoidance that could be checked by scrutinising cross-border transactions by the MNCs.

Meanwhile, many of the associations and organisations of professionals came up with initiatives to train up Chief Financial Officers (CFOs) of different MNCs on transfer mispricing.

The Institute of Chartered Accountants of Bangladesh (ICAB), KPMG, and Hoda Vasi Chowdhury and Co (HVC) have organised some workshops for the MNCs to build awareness on transfer pricing.

Recently, Pricewaterhousecoopers (pwc), Bangladesh and HVC arranged a seminar to discuss pros and cons of transfer pricing, the law and its implications.

The pwc will offer transfer-pricing services to the multinational companies operating in Bangladesh.

"We are the preferred partner at all stages from advisory and implementation assistance to TP documentation and audit defence," the pwc said.

The pwc offers advisory services, TP documentation, litigation support and other specialized offerings to help the MNCs adopt and comply with the TP law.

A United Nations Development Programme (UNDP) report in 2011 placed Bangladesh on top of the list of developing countries suffering financial outflows due to transfer-pricing trickery.

Bangladesh had suffered illicit financial outflow of US$ 34.8 billion since 1990 till 2008, the UNDP report indicated. The report estimates that trade 'mispricing' accounts for 65 to 70 per cent of illicit outflows from the Least Developed Countries (LDCs).

The UNDP underscored the need for adopting the TP law, terming it a 'potentially important' step for revenue mobilisation.

According to the TP rules, a prescribed form should be signed and verified by the person authorized to sign the return on income. Their accounts and records will be maintained separately as prescribed.

The document will also furnish particulars of international transactions, tangible property of revenue and capital nature of transaction.

"For every person who is involved in international transaction or transactions, if the aggregate value of which, as recorded in the books of accounts, exceeds taka 30 million during an income year, shall furnish, on or before the specified date in the form and manner as may be prescribed, a report from a chartered accountant," says the TP rule.

The Deputy Commissioner of Taxes (DCT) may impose a penalty equivalent to a maximum of 1.0 per cent of the value of each international transaction in case of failure to keep, maintain or furnish information, documents or records to him or comply with the notice.

The DCT can impose a penalty up to Tk 0.3 million for failure in furnishing report by chartered accountants (CA).

In case of failure on keeping SIT, DCT can impose 2.0 per cent penalty.

SIT reporting is a must for all taxpayers having international transaction. However, taxpayers having above Tk 30 million international transactions in a year have to maintain records as per guideline in the TP law.

doulot_akter@yahoo.com