Is stage set for derivatives trading?

Jasim Uddin Haroon | Sunday, 24 November 2019

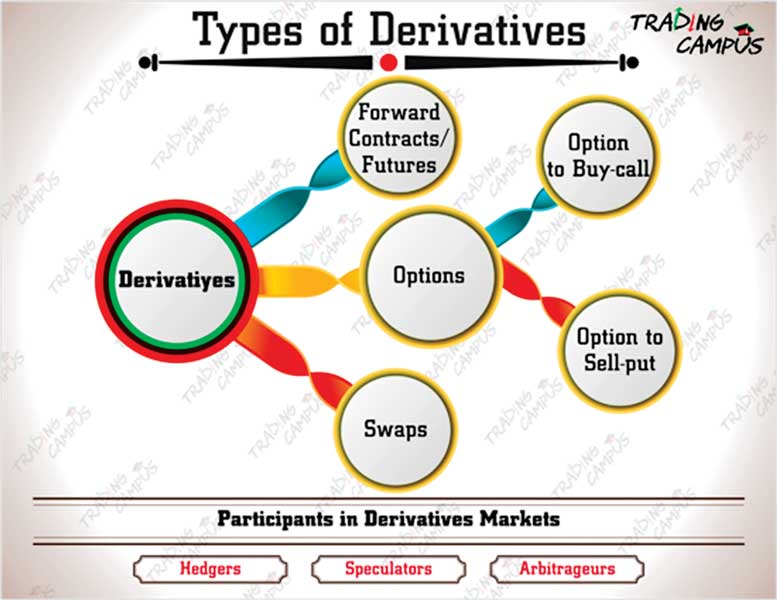

![]() Derivatives are complex financial instruments that are used by retail and institutional investors for managing risks. A derivative can be defined as a financial instrument whose value depends on the values of other underlying variables. Very often the variables underlying derivatives are the prices of traded assets. The forward contracts, future contracts, swaps, options are mostly common types of derivatives across the globe while alternative assets are real estate and hedge funds.

Derivatives are complex financial instruments that are used by retail and institutional investors for managing risks. A derivative can be defined as a financial instrument whose value depends on the values of other underlying variables. Very often the variables underlying derivatives are the prices of traded assets. The forward contracts, future contracts, swaps, options are mostly common types of derivatives across the globe while alternative assets are real estate and hedge funds.

It is believed that such types of securities are among the most actively-traded financial instruments that help deepen the capital market. According to the relevant literature, these securities have no 'intrinsic value'; their returns are linked to, or derived from, some other products or underlying assets.

Globally, the size of derivatives market advanced by around 24 per cent a year in terms of notional amount outstanding, far outpacing other financial instruments such as equities (11 per cent) and bonds (9.0 per cent). The 2018 data available with the Bank of International Settlement (BIS) showed the derivatives market was more than four times as much as the combined global equity and bond markets measured by market capitalisation.

These tools offer risk protection and innovative investment strategies in many capital markets, even in the developing world. Derivatives can be traded Over-the-Counter (OTC) or on the exchanges. OTC derivatives are created (and privately negotiated) by an agreement between two individual or institutional counterparties. Most of these contracts are held to maturity by the original counterparties, but some are altered during their life. Derivatives such as swaps, forward rate agreements, and exotic options are almost always traded in this way.

Derivatives can be traded Over-the-Counter (OTC) or on the exchanges. OTC derivatives are created (and privately negotiated) by an agreement between two individual or institutional counterparties. Most of these contracts are held to maturity by the original counterparties, but some are altered during their life. Derivatives such as swaps, forward rate agreements, and exotic options are almost always traded in this way.

Exchange-traded derivatives (ETD), on the other hand, are fully standardised and their contract terms are designed by derivatives exchanges. A derivatives exchange acts as an intermediary to all transactions, and takes the initial margin from both sides of the trade to act as a guarantee.

In Pakistan, derivatives based on financial assets trade on the Pakistan Stock Exchange (PSX), while commodity-based derivatives trade on the Pakistan Mercantile Exchange (PMEX).

In India, derivatives trading do the same through National Stocks Exchange (NSE) and other stock exchanges.

In Bangladesh, there is no derivative, though this is mentioned in the Securities and Exchange Ordinance 1969, the key law governing the country's stock market. The Bangladesh Securities and Exchange Commission (BSEC) also prepared a guideline in 2016.

With a population of 168 million, Bangladesh's economic growth has averaged 6.0 per cent during the past decade. The per capita GDP (gross domestic product) is slightly higher than US$1,900. But the country's capital market is not deeper enough—part of the reason is it lacks diversified instruments like derivatives.

The capital market had crash-landed in early December 2010. There was another such debacle in 1996, but the investors had little scope for diversifying their risks.

The volatility in the share market still persists and has become a matter of concern for both investors and policymakers. The key Dhaka index is now 4,600, same as the level in November, 2016.

There are two types of risks in the capital market–systematic risk refers to the risk inherent in the entire market, also known as "un-diversifiable risk." This risk cannot be mitigated through diversification, only through hedging or by using the correct asset allocation strategy.

Another risk is unsystematic risk that is unique to a specific company or industry. It is also called beta or "diversifiable risk". This type of risk can be minimised through diversification. But the investors are helpless in the market as they cannot dilute their risks. Due to the lack of such diversified products, the investors cannot reduce their risks. Ideally, investors build portfolios by dividing weights to different types of securities. The local investors have been missing such an opportunity.

As the financial market matures, the demand for the derivative instruments typically rises. Bangladesh's financial market is an exception. But some institutions, especially the private banks, have now been pursuing some derivatives products, although mostly plain vanilla types, not traded on exchanges.

The trend in such products is witnessed in the foreign exchange market, which usually remains highly volatile. Many who had contracts for floating exchange rates usually prefer fixed rates. Some enterprises prefer derivatives as a strategy to remain competitive. While some do the same to avoid potential defaults. Under such circumstances, the banks or non-bank financial institutions prefer to expand their lending or cash in on such type of volatility market through hedging.

It is evident that Bangladesh is becoming increasingly globalised, especially in the first decade of the century, driven by rapid growth in exports and imports. There is a phenomenal growth in exports in clothing, around 83 per cent of total exports. Similarly, the imports such as capital machinery, commodities and of late equipment meant for publicly-funded mega projects are on the upswing. Exporters and importers prefer derivative products as they notice it in their counterparts.

Non-traded or plain swap like the interest rate swaps is becoming popular in the financial market. Swap is gradually becoming popular in the country's financial market as many firms have been showing interest in the instrument to avoid volatility in the interest rate regime. Interest rate swap is the exchange of one set of cash flows for another—from floating to fixed rate or vice versa.

Usually taking place over the counter, the contracts are between two or more parties according to their desired specification and can be customised in different ways. For example, if a party borrows from abroad having floating rate, swaps will happen when it wants to convert it into fixed rate considering its long-term uncertainty in the foreign exchange market.

There are three different types of interest rate swaps: fixed-to-floating, floating-to-fixed, and float-to-float. In recent times, two local banks—Eastern Bank and BRAC Bank—cut two big deals valued at US$ 140 million.

Eastern Bank had struck an interest rate swap deal with Summit Group, the first of its kind by a local bank in October last year. The deal pertains to the interest payment on the US$71.25 million loans taken out by two concerns of Summit Group—Barisal Power and Summit Narayanganj Power Unit II—in December 2016.

On the other hand, BRAC Bank signed another swap with Ace Alliance Power Limited in March. BRAC Bank provided hedging for the electricity producer's exposure to LIBOR against its borrowing of $68.60 million for over 10 years. The deal is arguably the highest tenor interest rate derivative for any private bank in the country's banking history.

Ace Alliance Power Limited, a 149MW independent power project is situated at Kodda, Gazipur, jointly owned by Summit Corporation Limited and Summit Power Limited.

The inter-bank currency swap, an agreement to exchange cash flows in the future, dominates the country's foreign exchange market, according to the Bangladesh Bank. This type of derivative signifies that some banks hold adequate amount of greenback while the others belong to huge amount of local currency.

In accordance with the central bank, currency swap accounts for around 86 per cent of the forex market followed by spot. The forward, another derivative, has the least share in the forex market at 3.0 per cent. The cost of swap or the interest rate varies depending on the demand and supply. It usually ranges from 2.0 (annualised) and 3.0 (annualised) per cent. But the rate rose to 8.0 per cent at a time when the supply of dollars and other foreign currencies was scarce a year ago. The swap is typically used for liquidity support and as a hedging tool against the market risks.

Alternative investment complements bonds, stocks and other traditional financial instruments traded in the international financial market. Before issuing the alternative investment guidelines, there were a handful of venture capital firms in the country. Though the number has hit 16, only five are in operation.

Other tools like impact fund are largely neglected. A local TV channel had initiated the move to introduce the impact fund, but it has yet to get the operating licence from the BSEC.

Recommendations for introducing derivatives in Bangladesh:

1: Mindset

There is a need for mindset change for launching the derivatives by policy makers. There is also need for political commitment to explore the financially viable derivatives. This has become relevant in the era of the United Nations-led Sustainable Development Goals. Our policymakers and regulators are largely in the dark about this.

Given this, an assessment should be made as to whether the financial market is matured enough to launch such type of derivatives. The authorities can learn lessons from the neighbouring countries on how they introduced these advanced financial instruments.

2: Raise public awareness

Regulators, financial institutions and export/import entities have vague ideas about the concept and uses of derivatives.

This limited understanding of derivatives trading on the part of major players can constrain the development of the market. Hence, the initial process of creating a derivative market should involve sending customised videos and other creative visual products.

3: Rigorous training and faster licence issuance

Since institutions face hassle in getting licences, the authorities should pro-actively consider offering the operating licences based on merits. Derivatives products by nature are complex and the success of a derivative market is coherent with the knowledge and expertise of the participants.

4: Introducing new system

As soon as a feasibility analysis is done and a regulatory framework is in place, the focus should shift towards upgrading infrastructure to accommodate derivative trading. A deep and liquid market is a sine qua non of the development of an efficient derivative market. The easy movement of capital between different markets and currencies is essential for eliminating pricing discrepancies and efficient functioning of the markets. The stock market probe report highlighted the need for restructuring the capital market regulator and also strengthening other institutions, including the Central Depository Bangladesh Ltd. (CDBL). Such actions should be taken on a priority basis, both for improving our stock market and creating a platform for a derivative exchange. In order to boost investors' confidence, the potential derivatives exchange must establish online system for trading of such instruments and there should real-time market surveillance systems to detect market abuses.

A specific sub-group of an advisory committee comprising mathematicians, analysts and derivative exchange consultants should be in charge of preparing all rules pertaining to trading, clearing, settlement, margin maintenance and membership eligibility criteria.

5: Establish a central counterparty (CCP)

The move is on to set up the CCP by the DSE. A project has been undertaken. In order to maintain the efficiency and transparency of the derivatives security exchange, clearing and settlement of such products should be executed through the central counterparty with multilateral, multi-product close-out netting arrangements.

Clearing houses can be organised in a wide variety of ways: some are organised as departments of their affiliated exchanges (vertically integrated) while others are independent legal entities.

In the present scenario, all transactions are settled by clearing house, which is part of the DSE and the settlement is based on the category of shares (such as A, B, N, G, and Z). The CDBL, on the other hand, acts as a record keeper by electronically recording and maintaining securities accounts and registering the transfer of securities.

But the modern concept of clearing house for a derivative exchange is distinct. The central counterparty acts as a buyer to all sellers and a seller to all buyers and assumes the responsibility of a guarantor to both parties.

Bangladesh should establish an independent clearing corporation/clearing house for the proposed derivative exchange, which should become counter party for all trades or alternatively guarantee the settlement of all trades.

To conclude, there is a need for coordination among all required regulatory and administrative bodies—the BSEC, Bangladesh Bank, Insurance Development and Regulatory Authority and the financial institutions division of the ministry of finance. Bangladesh's financial market is not growing as it should be due to the lack of coordination among the key actors.

The writer, a special correspondent at the FE and a certified research analyst, can be reached at: jasimharoon@yahoo.com