Juggling revenue gaps and spending obligations in an election year budget

M A Razzaque | Tuesday, 16 May 2023

The Bangladeshi economy continues to grapple with macroeconomic stress. These challenges began surfacing domestically when imports spiked due to pent-up demand in the wake of economic recovery after the Covid-19 shock. The rising value of the US dollar across the world exacerbated the situation. The Russia-Ukraine conflict further contributed to the strain by disrupting supply chains and escalating global commodity prices, which in turn made imports even more expensive.

On the contrary, for Bangladesh and many other developing countries, earnings from exports and remittances didn’t rise proportionately, leading to a rapid depletion of foreign reserves. To stem this decline, the Bangladesh Bank was compelled to let the taka depreciate and impose import restrictions. These measures fuelled high inflationary pressure within the domestic economy.

As of July 2022, the gross foreign exchange reserve was at a robust US$39.6 billion. However, it experienced a significant reduction over the year, dropping to $30.34 billion by May 8, 2023. Inflation also saw a sharp rise, peaking at 9.5 per cent in August 2022 and maintaining an average of 8.9 per cent over the subsequent 10 months, overshooting the annual target by 3.5 percentage points. On the other hand, remittances accumulated from July 2022 to April 2023 amounted to $17.72 billion. Projections from PRI Study Center on Domestic Resource Mobilisation (PRI-CDRM) suggest that by the close of the current fiscal year, the total remittance earnings will amount to $21.26 billion. However, this figure still falls short by S$6.10 billion of the revised remittance target outlined in the Monetary Policy Statement.

The export outlook also appears to be rather bleak. From July 2022 to April of FY23, total earnings from exports amounted to S$45.7 billion, falling short of the target by 3.46 per cent. Given the recent downward trend, the PRI-CDRM projects exports at the end of FY23 to stand at about S$54—a shortfall of $4.2 billion from the budget target. Additionally, due to the dollar crisis, import figures have also seen a significant decrease.

These recent developments have significantly affected the growth trajectory. The global economic growth is anticipated to decelerate to 2.6 per cent in 2023, and in line with this trend, the IMF has projected a 5.5 per cent growth for Bangladesh. Most recently, the provisional estimate by the Bangladesh Bureau of Statistics (BBS) pegged the country’s growth rate at 6.08 per cent for FY23.

Given the recent macroeconomic developments and the upcoming national election—widely expected at the end of the calendar year—the forthcoming budget for FY24 takes on increased significance. The fiscal framework of the upcoming budget is of particular interest in assessing how the IMF program conditions will be met in the backdrop of macroeconomic stress, uncertain global economic and financial climate, and unfolding electoral dynamics.

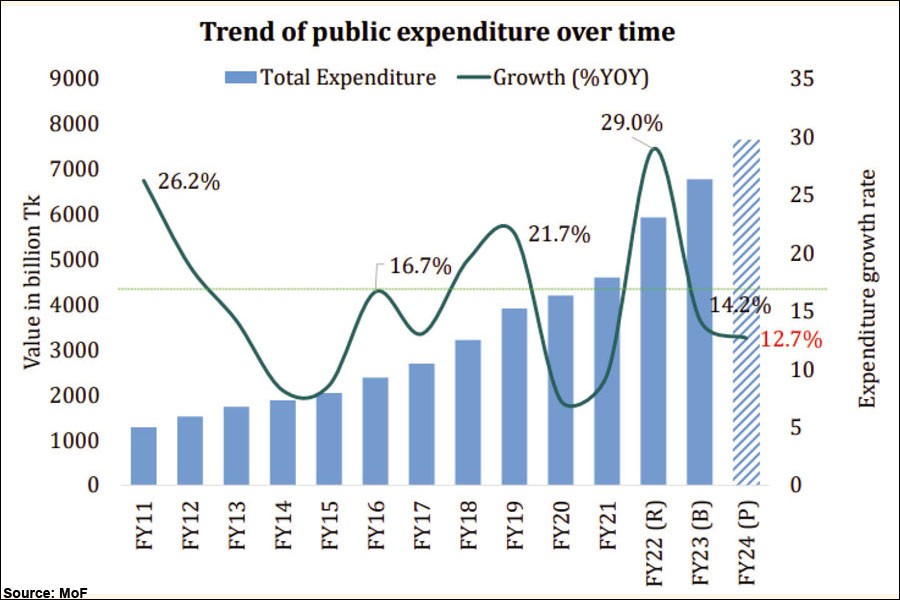

The budget context: A national budget for FY24, amounting to Tk. 7.60 trillion, was approved in a Cabinet meeting held on May 11 and will now be placed before the Jatiya Sangsad. It represents a 1 per cent increase in national spending from the previous year. The revenue collection target for the upcoming fiscal year has been set at Tk. 5.0 trillion, marking a 15 per cent rise from the current fiscal year. The National Board of Revenue (NBR) is tasked with collecting Tk. 4.3 trillion, a target 16.2 per cent higher than that of the previous year. Furthermore, the non-NBR revenue and non-tax revenue collection targets are set at Tk 200 billion and Tk 500 billion respectively.

As the government plans to increase the size of the upcoming budget, it is vital to acknowledge the expected substantial shortfall in overall revenue receipts for the current fiscal year. As of March, the NBR has collected Tk 2,255 billion (5.1 per cent of GDP). That is, it will need to mobilise further an amount which is about 40 per cent of the overall budget target for the year (i.e., Tk. 1,445 billion) in the last quarter of April-June (see Figure 1).

Given the preset revenue milestones, the NBR is supposed to gather Tk 816.7 billion from VAT and SD, Tk 498.5 billion from income and other profits, and Tk 129.7 billion from customs and excise duty. However, according to PRI-CDRM estimates, if the NBR’s revenue growth trend of the past quarter persists, the projected revenue shortfall could be around Tk 546 billion.

To meet the NBR revenue target for FY23, an average monthly collection of Tk 482 billion (representing a monthly average growth of 60 per cent) would be required in the last quarter. The revenue target set by the IMF, Tk 3368 billion, is significantly lower, as it opted for a more realistic one considering the weak record of revenue collection over the past several years. To meet the IMF’s target, the NBR will need to mobilise Tk 1113 billion in the final quarter of this fiscal year. This demands an average monthly generation of Tk 371 billion during April—June, which corresponds to a growth rate of 24 per cent compared to the preceding nine months’ 8 per cent growth. According to PRI-CDRM estimates, the NBR could face a revenue shortfall of Tk 214 billion when measured against the IMF target. There remains a slim chance for the NBR to meet the IMF target, although this would likely necessitate aggressive collection efforts. Conversely the chronic underutilisation of budgetary allocations remains a characteristic feature of Bangladesh’s fiscal landscape, a trend that continues in FY23. However, this does provide a modicum of relief to policymakers by assisting in maintaining a lower deficit-GDP ratio for Bangladesh. As of February in the current fiscal year, only 20 per cent of the annual development program (ADP) budget has been used, according to the data from the Ministry of Finance. Despite a 32 per cent higher ADP allocation (in FY23 over FY22), the actual spending during July-February of this fiscal year was 5.1 per cent lower than that of the same period of FY22.

An increasing trend in the allocation of resources for interest payments, subsidies, public servant wages and allowances, and pensions and gratuities persist. The total allocation for interest payments, subsidies, and wages and allowances is expected to surpass Tk. 3 trillion in the forthcoming FY24 budget, eating up a significant part of the overall NBR revenue earnings. As seen in previous years, the government continues to rely heavily on both domestic and foreign borrowing to bridge the budget deficit. Interest payments on both foreign and domestic debts are escalating and are projected to cross Tk. 1,000 billion in FY24, which could constitute about 30 per cent of the NBR revenue in FY23. Despite shortcomings in revenue collection, the budget deficit might not be a significant concern as total public spending consistently falls well below the proposed budgetary allocations. However, this comes at the expense of inadequate expenditure in crucial sectors such as social protection, health, and education.

In the proposed FY23 budget, expenditures on social protection, health, and education constituted 2.55 per cent, 0.8 per cent, and 1.8 per cent of GDP, respectively. Compared to countries in a similar stage of development, Bangladesh’s spending in these sectors is markedly lower.

Conditions linked to the IMF loan package: The drive to enhance revenue collection and optimise existing tax systems could facilitate the generation of necessary resources. These could then support the allocation of additional funds towards social protection programs and other pressing expenditure needs. The IMF has also attached several conditions to its loan package to reinforce the fiscal framework of the country.

Notably, one of the key IMF requirements involves bolstering revenue mobilization efforts by an additional 0.5 per cent of GDP annually in both FY24 and FY25, followed by a further 0.7 per cent increase in FY26. This implies elevating the tax-GDP ratio from the current 7.8 per cent of GDP to 8.3 per cent in FY24, to 8.8 per cent in FY25, and finally to 9.5 per cent by FY26. The IMF has also recommended the establishment of Compliance Risk Management Units within the customs and VAT wings of the NBR by December of this year.

Furthermore, the IMF has provided a comprehensive set of conditions, which includes reducing tax expenditures across major sectors, developing and adopting a Medium-Term Revenue Strategy (MTRS), a Tax Compliance Improvement Plan, and a modernised Customs Act. These measures aim to bolster the government’s revenue generation in the quest for fiscal stability and sustainability.

Recently, an IMF team visited Bangladesh to review the progress made since the country received the first instalment of $476 million as part of the IMF loan package. The NBR has reported the following major measures, amongst others, as part of its efforts to boost revenue:

• The NBR is collaborating with the World Bank to develop a medium-term revenue strategy to meet loan conditions.

• The NBR is implementing extra measures for enhanced revenue growth, such as plans to reduce duty exemptions for additional revenue collection, reorganize duty rates, strengthen the duty recovery process, initiate speedy disposal of cases, enact new customs laws, automate the duty collection process, and fully operationalse the Customs Risk Management Unit within three years.

• The NBR will adopt case-by-case tax benefits and review existing exemptions (which, according to NBR estimates, currently account for 2.8 per cent of GDP).

• The NBR plans to install 60,000 Electronic Fiscal Devices (EFDs) in retail shops in Dhaka and Chattogram and aims to install 0.3 million devices over the next six years. As of January 2023, around 9097 EFDs have been installed in various shops.

• The NBR is developing specialized software, known as the “Risk Management Engine”, which will bring transparency to the tax audit process, check the discretionary power of tax officials, detect tax evasion, and alleviate audit fears among taxpayers. The piloting of this automated computer program will commence soon in one or more circle offices of Tax Zone 6 in Dhaka.

Policy recommendations: After analysing the overall macroeconomic context and government revenue situations, PRI-CDRM proposes the following broad policy options:

• Prioritise fiscal reforms. There have already been extensive discussions on this topic, and the 8th Five-Year Plan (8FYP) provides some concrete measures for reforming the fiscal sector. It is crucial to make significant progress on implementation.

• Expand the tax net. Despite a population of more than 160 million, only 7.8 million (4.8 per cent) have Tax Identification Numbers (TINs). It is crucial to bring a greater number of people under the tax net to increase the tax-GDP ratio.

• Reduce indiscriminate tax exemptions. According to an estimate by the NBR, tax exemptions currently account for around 2.3 per cent of GDP. Reviewing these exemptions on a case-by-case basis could significantly decrease this percentage.

• Increase compliance with corporate tax. Out of the 2.8 million companies registered under the Registrar of Joint Stock Companies (RJSC), only 1.99 million have TINs, and among them, only approximately 15 per cent of the companies paid tax in FY22, with just 31,000 submitting a return.

• Increase the compliance rate of the personal income tax system. If all households in the top 10 per cent income decile were subject to a 10 per cent tax rate, the tax-GDP ratio could be increased by 1.6 percentage points.

• Reform VAT – the VAT yield—i.e., VAT revenue as proportion to GDP—remains low and almost stagnant between FY10 to FY22. Short-term VAT reforms could increase the tax-GDP ratio by up to 0.6 percentage points, and additional reforms could further increase this in the medium to long term.

• Reform state-owned enterprises (SOE). This should be introduced to improve their financial performance by implementing a hard budget constraint, improving pricing policies, and strengthening corporate governance.

• Improve quality of spending. Placing an emphasis on judicious spending of public resources can ensure effective utilisation and higher returns on government spending.

Dr M A Razzaque is Director, Policy Research Institute of Bangladesh (PRI) Study Center on Domestic Resource Mobilisation (PRI-CDRM). The piece is based on his presentation in the Press Briefing on PRI-CDRM Pre-Budget Discussion held on Sunday last in Dhaka. m.a.razzaque@gmail.com