Listed MFs: What lucrative returns over last 5 years suggest

MOHAMMAD MUFAZZAL | Thursday, 9 March 2023

Investor participation in transactions of listed mutual funds (MFs) was nearly zero percent of the total March 2 turnover of the Dhaka Stock Exchange.

The 36 MFs saw transactions amounting to Tk 0.7 million only on the day while the IT sector, which comprises small-cap companies and has market cap of almost equal size, recorded a turnover of Tk 1.31 billion.

Investors have been nearly as uninterested in the MFs over the years while their participation grew with time in the 18 other sectors of listed securities.

That explains why a majority of the MFs have been traded at below their face value of Tk 10 in the secondary market.

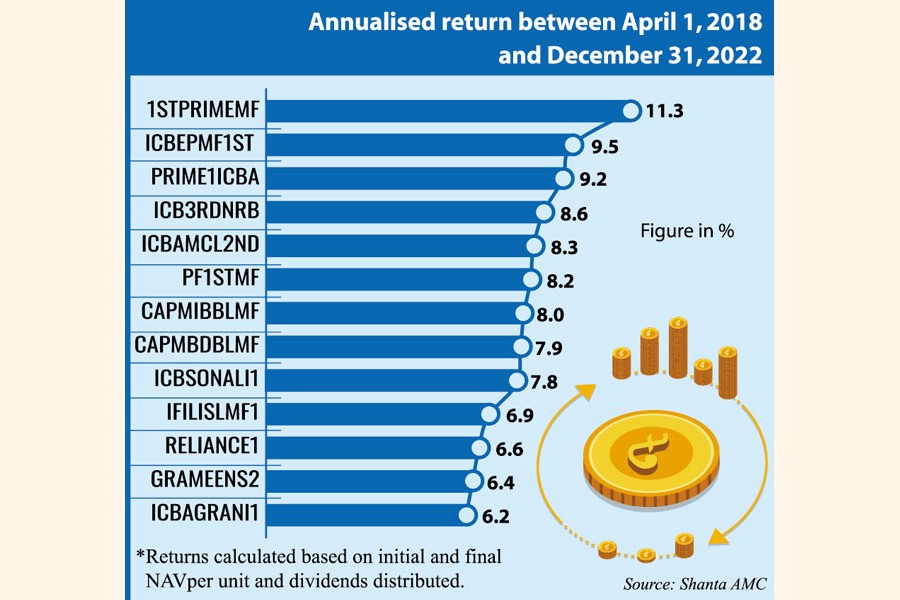

But if the last five years' returns of the closed-end MFs are taken into consideration, it seems they benefited unit holders more than other securities. In cases, some MFs ensured returns at a higher rate than the bank interest rates.

Prime Finance First Mutual Fund (1STPRIMEMF) topped the chart with 11.30 per cent annualised return between April 1, 2018 and December 31, 2022, based on its initial and last net asset value (NAV) per unit and the sum of annual cash dividends per unit distributed during the period.

Of the remaining listed MFs, the annual returns of 12 were between 6.2 per cent and 9.5 per cent.

The securities include ICB Employees Provident MF 1: Scheme 1, ICB Employees Provident MF 1: Schem-1, ICB AMCL Third NRB Mutual Fund, ICB AMCL Second Mutual Fund, Phoenix Finance 1st Mutual Fund, CAPM IBBL Islamic Mutual Fund, CAPM BDBL Mutual Fund 01, and ICB AMCL Sonali Bank Limited 1st Mutual Fund.

Most of these funds are managed by ICB Asset Management Company.

During the period, the compounding annual growth rate (CAGR) of the market was 1.6 per cent.

The closed-end MFs' returns are determined with cash dividends and NAV as investors can liquidate their holdings at NAV at the maturity of the funds and the standard practice of such securities is to distribute income through dividends.

Unit holders could also make capital gains if the unit prices go up in the secondary market.

Even if unit holders of Prime Finance First Mutual Fund did not wait until the maturity date, they received 8.5 per cent cash dividend in 2018, 7 per cent in 2019, 8 per cent in 2020, 10 per cent in 2021, 11 per cent in 2022.

An investor, who purchased the fund units at the face value of Tk 10, realised dividends at an average rate of 8.9 per cent for keeping the holding for the period, which is still higher than dividend yields of most stocks.

1STPRIMEMF was floated in 2009 and its 10-year tenure was supposed to end in 2019. Before completion of the tenure, it was extended for another term of 10 years until 2029.

The listed MFs distributed higher cash dividends because of the regulatory provision that they give away at least 70 per cent of their annual income.

The MFs also distribute dividends out of their reserves.

Why did investors turn away from closed-end MFs?

MFs are usually considered long-term investments. But investors lost the opportunity to liquidate assets as per NAV when the tenures of MFs were extended.

The regulatory decision was taken after the 2010 stock market crash to the frustration of local and foreign investors.

Those, who had injected huge funds in the closed-end MFs, were awaiting liquidation of the assets at NAV.

On condition of anonymity, an official of a leading asset management company in Dhaka, said the CITY of LONDON, an investment management company, was a big one among the foreign investors.

The total assets under management (AUM) of closed-end MFs are worth Tk 57.51 billion, according to data available until the end of 2022.

A mutual fund needs to invest at least 60 per cent of the fund in listed securities and the remaining 40 per cent in non-listed securities.

In the bull run of 2010, most of the listed MFs had investments far above the stipulated limit in listed securities. Some even had injected the whole fund in the secondary market.

After the unprecedented market debacle, the portfolios managed by the fund managers squeezed badly and the funds suffered huge price erosions in the secondary market.

Of 36 listed MFs, the market prices of 33 are below the face value of Tk 10 whereas the remaining three funds are traded slightly above the face value.

Md. Moniruzzaman, managing director at IDLC Investments, said the MFs had been traded at a premium to NAV [5-6 times NAV] before the market debacle.

The price erosions resulted in heavy discounts to NAV, he added.

The extension of the MFs' tenure irked investors further.

Mr. Moniruzzaman said that when the tenures of the closed-end funds were extended for 10 years people lost the remaining hope.

This is the backdrop to no new closed-end MFs being floated now as investors are not interested in purchasing units of a new fund at Tk 10 each unit. The units of most old MFs are available at below Tk 10.

Investors also lost confidence in such securities due to several scams committed by fund managers.

Another regulatory decision to issue re-investment units (RIU) diminished whatever potential the MF industry had left.

The size of a fund has been increased through RIU and so management fees of the asset management companies went up. But the newly-issued units brought no benefit for investors as they have to sell units at prices below the face value in the secondary market.

mufazzal.fe@gmail.com