Margin loans: The tale that has not been told

Lenders target big investors for hefty commission earnings but in the end the flow of borrowed money into stocks helps no one

Mohammad Mufazzal | Sunday, 31 March 2024

General investors and the country's capital market repeatedly become victims of accumulated burden of margin loans disbursed to big investors.

General investors and the country's capital market repeatedly become victims of accumulated burden of margin loans disbursed to big investors.

The recent rapid market erosion is the latest such event that befell them.

The regulatory bodies have always claimed that they take "market supportive measures", for example expanding the scope of margin loans or imposition of floor price, to protect small investors, but representatives of several brokerage houses and other stakeholders that the FE talked to rejected the claims.

They have put forth arguments that explain past and present market behaviour.

High net-worth individuals can avail of large loans against big investments of their own, which in turn help boost transactions and earnings in the form of commission of the broker involved.

For individual and professional success, executives or any other officials of brokers may encourage wealthy investors to borrow money for stock investment. Such investors themselves also negotiate large loans at times while opening BO (beneficiary owner's) accounts or making high investments into stocks through a broker.

When the market takes a nosedive and margin accounts lose equity value, brokers on one hand assure borrowers of a quick recovery while on the other request the securities regulator for time extension for provisioning against losses in margin accounts.

The presence of general investors, who account for 80 per cent of the market investors, is insignificant in a scene like this.

But they bear the brunt of the ramifications of forced selling in margin accounts when lenders go on a drive to recuperate the money lent.

Ill intension behind the scene

Brokers prefer high net worth individuals who have injected or are willing to inject large amounts of money into the market.

"Disbursement of margin loans to small investors is not cost effective," said Managing Directors of Midway Securities Md. Ashequr Rahman.

For example, a margin loan worth Tk 50 million to a big investor makes more business sense than Tk 0.1 million to a small investor.

Officials at brokerage houses do not advise putting the fund into purchasing any blue chip stocks, such as Square Pharmaceuticals, said Mr Rahman.

Instead, they directly or indirectly persuade investors into buying stocks whose rally or even the price fall will benefit the brokers, he added.

Echoing Mr Rahman, chief executive officer of another leading brokerage firm, said forced sales did not occur in fundamentally strong stocks.

"Forced sales happen in speculative stocks that somehow get the label of marginable security," he said.

Who is benefitted?

Lenders provide margin loans at a ratio of 1:1. So, if an investor has assets worth Tk 50 million in the stock market, he/she can get an equal amount in loan.

In most cases, the investor gets trapped.

When he thinks he would be able to liquidate his assets and come out of the debt repayment obligation with a small loss, those working at the brokerage house assure him of a loss recovery after a certain period.

The investor may see further depletion of his asset value and then he fails to shift to any other firm due to erosion of his own fund and the burden of margin loans.

Many market operators say it is difficult to gain profits by investing borrowed cash into stocks after a high interest payment.

But officials working for the broker in the meantime have successfully projected good commission earnings from transactions of high share volumes.

"The person [gainer] can be anyone between traders and the top executive in a firm that has disbursed margin loans," said Mr Rahman, of Midway Securities.

Preferring anonymity, two senior officials of two leading brokerage firms said a few lenders had even appointed agents to bring high net worth individuals as clients.

"The market is mainly driven by margin loans. That's why the floor price protected [big] borrowers from margin calls but for the time being," said Mr Rahman, adding that the borrowers eventually failed to recover losses.

However, the regulator many a times said small investors would be affected if the floor price were withdrawn.

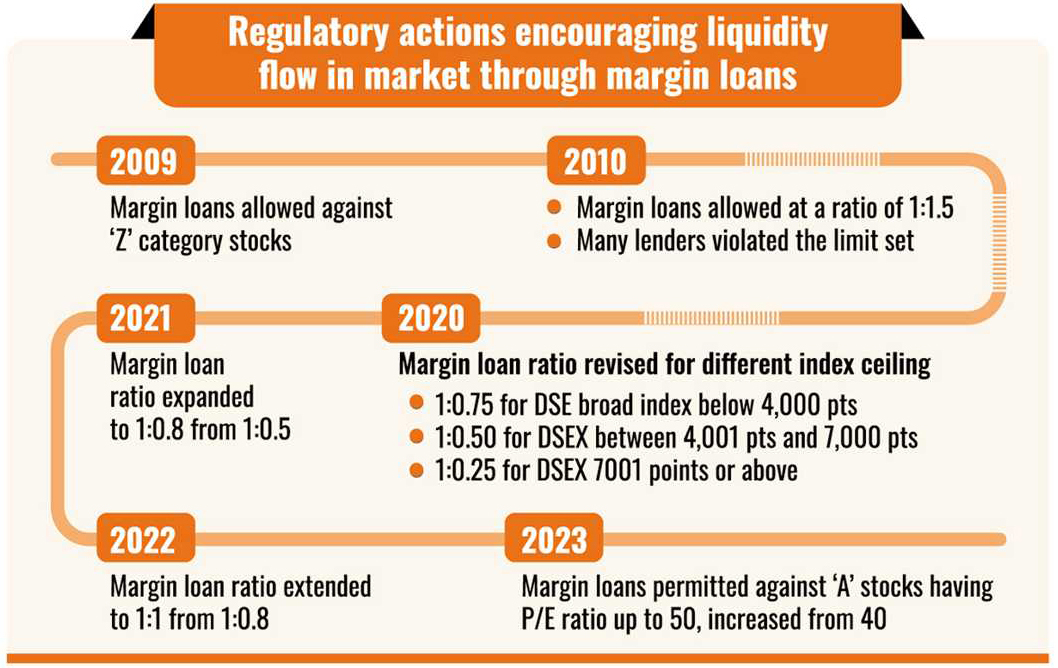

Regulatory actions that went against market

A probe report mentioned the imprudent disbursement of margin loans as the main factor for the 2010 stock market debacle.

After the debacle, the securities regulator informally asked lenders not to execute forced selling in a bid to contain the market fall.

Meanwhile, two investors filed a writ petition with the High Court for an order against execution of forced selling. The HC issued a ruling in their favour.

That, however, did not benefit borrowers.

A director of a leading brokerage firm, which was one of the then top 10 lenders, said the expectation regarding loss recovery in margin accounts had been proved wrong and that the majority of margin accounts with negative equity experienced further erosion.

Following the suspension of forced selling, the market exhibited an upward trend but it retreated quickly.

The then broad index DGEN rose to 8771 points on December 7, 2010 from 6436 points on August 1, 2010. It then declined to 5603 points by May 2011.

"The decisions [regarding margin loans] did not benefit lenders. Neither did they benefit the clients," said the director on condition of anonymity.

The market has been suffering from a huge burden of negative equity created in margin accounts.

The regulator, as some stock brokers said, no longer puts up resistance against forced selling.

But the damage is already done and it is reflected on the market time and again like the recent stock plunge on the Dhaka Stock Exchange.

mufazzal.fe@gmail.com