Mobile Financial Service attains spectacular success

writes Khondoker Shakhawat Ali in the first of a two-part article titled \'Question of ownership of mobile financial services by MNOs\' | Wednesday, 18 November 2015

Mobile Financial Service (MFS) is a core vehicle for development in the present context of the developing countries. Bangladesh has already laid the foundation of success and it has drawn the attention of many local and global leaders. It has been possible due to the appropriate policy, discreet decision and bold steps of the Government. Bangladesh's MFS success story has taken the centre of interest for Mobile Network Operators (MNOs), the World Bank, the Queen of the Netherlands, Bill and Melinda Gates Foundation, local corporate NGOs, local banks and local corporate media. The only lacking in their excitement is our 'national interest' and 'consumer rights'. The origin of their interest lies in the size of our massive market and to remain involved in our root-level financial activities. I had the opportunity of representing the 'customer rights' in the USSD Technical Committee of Bangladesh Bank in 2014 along with all the relevant stakeholders. Being there as a sociologist and social researcher, I could, on the one hand, read the values and interests of the stakeholders and, on the other, got to see the market scope, spread and depth and future opportunities of MFS. Considering the facts of national and consumer interests, I hereby present my observations.

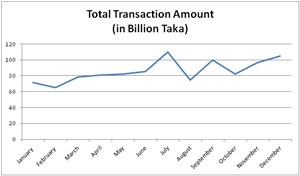

The Bangladesh Bank (BB) circulated the MFS guideline back in 2011 which specifically disallowed the MNO to lead or dominate the MFS sector. The decision was made based on intense research and efficient analysis, which helped to achieve tremendous result in this sector within the last four years. The pragmatic guideline contributed in such a penetration that the customer-base went from zero to 30 million within a little more than four years. Every day, the MFS industry is processing around 3.5 million financial transactions. The penetration grew faster than any other MFS setup in the globe. Overall analysis says, Bangladesh has established a successful MFS industry within a short time.

Since the MNO-led model was rejected by the Bangladesh Bank in 2011, the MNOs have been campaigning hard to enter this industry. During the first two-to-three years after the guidelines were issued, the MNOs claimed that they would be able to reach millions of unbanked people faster than banks or potential new MFS providers. They claimed that the goal of accelerated rate of expansion is better achieved through MNOs. On the contrary, banks and MFS providers have demonstrated their capacity for spectacular growth as well as cost-effective delivery systems in Bangladesh. So the preliminary claim from MNOs failed to show any justification in reality.

The MNOs have been putting their energy and effort to enter into the MFS industry since the beginning. In the process, various rumours are spread against the MFS industry. It was claimed that the most successful institution in MFS-bKash-is a 'monopoly'. In reality, the Bangladesh Bank has issued MFS licenses to 27 banks and 10 out of them are active and currently working in the field. Dutch-Bangla Bank, bKash's nearest competitor, has registered more than five million customers. Recently, another MFS company, Sure Cash has made a new investment of US$ 7.0 million. MFS providers like bKash and Dutch-Bangla Bank are offering the service at the lowest price in the world. Besides, the agent network that effectively covers the whole country and is the main strength of the industry, is openly shared by all MFS providers. So the reality is far away from a monopoly situation. Among the 27 banks with MFS licenses those who had done their homework well and had meticulous preparations have shown better results in the market.

The correct policy response is to further evaluate the currently successful modus operandi of the existing MFS, provide technical and other kinds of support to those lagging behind, ensure a level playing field, and prevent possibilities of unfair competition. By ensuring a level playing field, capital will be attracted into this burgeoning industry and will facilitate its growth. Hasty actions that may lead to unfair competition will achieve exactly the opposite. It is noteworthy that within the MNO industry itself, the largest operator-Grameenphone-at one point held 80 per cent of the market; but other players then learned and adopted what worked, and today Grameenphone's market share is down to nearly 40 per cent. Learning, adopting new strategies, and developing effective competition among the various players take time.

While there are voices on behalf of the MNOs that claim that they will bring bigger competition in the MFS industry, it is important to analyse and understand the possible impacts and challenges of their entrance in the already existing competitions and future market dynamics. Hence we are to revisit the guideline of 2011, to figure out how MNO's participation may put challenges and affects the growth MFS is currently witnessing.

This is why we need to revisit the rationale that went into the 2011 guidelines. There are five sets of challenges that are likely to arise by allowing the MNOs to own MFS businesses. The first challenge relates to accountability which is detailed below:

a. Regulatory space: As the financial regulator BB took a judicious step by rejecting MNO-led model in 2011 Guidelines. A critical reason for the Central Bank to reject the MNO-led model was to ensure carrying out its regulatory responsibilities. MNOs being outside Central Bank's jurisdiction would not be held responsible for the risk of controlling money supply and monetary transactions of the citizens. Bangladesh Telecom Regulatory Commission (BTRC) regulates the MNO industry; they are no way related to controlling monetary transaction. In the prevailing situation there is no scope of conflict between BB and BTRC.

b. Limiting regulatory options: The government needs to keep its regulatory options open. MFS is new and, at the same time, handling daily financial transactions of millions of low-income people. If MFS and MNOs are kept separate, the government will be able to deal with the two industries exclusively to handle the specific issues of each party. On the other hand, if they are combined, it will not be possible to segregate them later. Kenyan experience in this regard is the glaring example, where a dominant MNO in Kenya with a predominant market share has indeed created a monopoly MFS, limiting regulatory options for the Kenyan government.

c. Supplier-customer conflict: MFS providers, i.e., bulk customers of MNOs, are naturally dependent on any of the MNOs for their connectivity supply. The greater financial muscle of the suppliers (connectivity provider, MNOs) naturally build up tension on the bulk customers (the MFS providers). This natural supplier-customer tension can quickly transform into endless disputes-unless there is a clear boundary dividing suppliers and customers. This relation has become more complex with the MNO's dream of gaining ownership of MFS. Until a clear-cut demarcation is spelt out, Bangladesh Bank, as the regulator, has to create a framework that ensures justice for both the parties, so that they can bilaterally resolve their dispute. Regulators must create structures that generally lead to fairness automatically and protect the process from disputes to the extent possible. It will be impractical for regulators to constantly arbitrate conflicts and disputes that emerge from wrong structures.

d. Marginalising the risks of MFS: If we are earnest about the success of an MFS provider, we have to see how good a job it does independently as the success is related to the interest of the industry as well as the customer. bKash is an appropriate example in this case. The distinguishing difference between bKash and other MFS providers is in its focus. It is a company that does only MFS and is especially focused on the unbanked masses. bKash is doing better than its competitors because it is mandated to provide only financial services through a dedicated workforce and cannot afford to move away from its MFS focus. In fact, this could well be an important reason why bKash has done well vis-à-vis other providers of similar services. In this aspect we have to formulate policy to create more of these entities, controlled and owned by local entrepreneurs.

By definition and considering the economic perspective, MFS is, at best, a marginal business for the MNOs. They may at best consider it as another non-critical value added service, while it has become a critically needed service to millions of low-income people. This raises a fundamental question of accountability with regard to the cause of financial inclusivity. Above all, there are serious risks in handing over a sensitive industry to large MNOs who are not concerned to exclusively provide financial services nor are accountable for their performance with regard to MFS.

The writer is a sociologist and social researcher; Fellow of PPRC; Member, Bangladesh Bank USSD Technical Committee 2014.

shakhawat.bangladesh@gmail.com