Modus operandi of offshore banking in Bangladesh

Mohammad Rafiqul Islam | Thursday, 2 March 2017

Primarily, offshore banking refers to a banking system dealing with non-resident individuals and enterprises as defined by the exchange control authority of a host country where its offshore financial centre exists. Offshore banking also serves the resident enterprises as per instruction of the exchange control authority by issuing scheduled circulars and regulatory orders to enable the resident enterprises availing of low-rate foreign currency financing facilities. In a nutshell, the offshore banking is a localised global bank. An offshore financial centre or offshore banking unit is the window of a bank through which foreign currency assets and liability are moved to and from.

In Bangladesh, the motivation behind offshore banking was to get around the countries where tax is unreasonably higher. The country's offshore banking began in 1980 through the incorporation of Bangladesh Export Processing Zone Authority (BEPZA) Act - 1980 and Bangladesh Bank BCD Circular No.(P)744(27) [dated 17 December, 1985] only for facilitating foreign direct investment (FDI) and a hassle-free movement of funds - both inward and outward. The aim was to attract foreign investors towards the new Export Processing Zones (EPZs) in Chittagong. Up to 2001, offshore banking gave incentives to non-resident investors as Bangladesh-based offshore financial centres owned by numerous foreign banks took the reins. The local banks started to turn up in the market after 2001 - Agrani Bank became the country's first bank to receive offshore licence from Bangladesh Bank in 1988.

Almost all the Bangladeshi banks have established offshore banking units due to a growing demand. The customers are mostly: EPZ Enterprises (specially 100 per cent foreign-owned companies in the export processing zone in Bangladesh and the 100 per cent locally-owned companies only for discounting the bill in FC); Non-Resident Bangladeshis (NRB) who are earning foreign currencies staying abroad; any non-resident individual and enterprise incorporated outside Bangladesh; resident registered industrial entities having permission to import industrial raw materials and machinery (introduced since the Financial Crisis of 2008-09); deemed exporters who are providing raw materials to direct exporters against foreign currency payment; any enterprise intending to borrow foreign currency loan from abroad under the permission from regulators; the offshore enterprises, and the subsidiary of the domestic enterprises having investment out of Bangladesh since convertibility of the Bangladesh's capital account is being permitted on case-to-case basis by the Bangladesh Bank.

Offshore banking is a highly supervised banking system in Bangladesh. The reason behind the supervision is to avoid the risk of LC-FC (local currency-foreign currency) mix-up and flight of local capital outside the country through conversion into foreign currency.

OFFSHORE BANKING'S CONTRIBUTION TO ECONOMY: Offshore banking financial centres are offering foreign currency loan with rate of interest (around 4.50 per cent) which is three times lower than that (10 per cent) of the local currency denominated loan. The lower rated foreign currency loan is contributing to reduce the cost of capital of the borrowing enterprises. If cost of capital is reduced, the revenue generation of those enterprises will gain momentum. Regarding working capital financing or temporary trade-based financing from offshore financial centres, the products of the manufacturing-borrowing concern will be highly competitive in the local and global market due mainly to the lower rated financing to the supply chain by the offshore financial centres. Foreign currency financing to the resident enterprises help reduce the high-rated taka debt burden (including stressed loan).The major contribution to the economic growth, so far witnessed by the Bangladesh economy, is reimbursement by the offshore financial centre buyer's credit) against the Usance Payable At Sight LC (UPAS LC) issued by the authorized dealer branches on behalf of the importers of the domestic tariff area. Reimbursement under UPAS LC helps increase the credit rating of the country by timely payment of overseas commitment of the local banks to beneficiaries.

Offshore financial centres are saving foreign currencies of the country. Nearly, $5.0 billion used to be drained out annually in the name of interest and confirmation charges. After the vindication of the FE Circular No-28, 2010, cyclopean change in foreign currency interest payment has been reduced manifold.

An offshore financial centre creates confidence in foreign investors by providing various tailor-made products and facilities relating to free movement of fund in the name of inward and outward remittance for their equity capital and inter-company loan. It facilitates the transfer of dividend, capital gain to the host country of the investors by reducing required taxes.

REASON FOR INCREASING TREND IN FC LOAN: Offshore banking offers all kinds of products that are offered by the domestic or onshore banks.

Since the pricing of taka denominated loan products (around 16 per cent in trade financing) were higher in comparison with that of the foreign currency loan (around 4.50 per cent) in the international market, the borrowers were struggling to survive with the burden of higher rated bank financing after the 2009 financial debacle in the global economy; the small and medium-sized enterprise (SME) market in most of the region of the world was highly saturated, the foreign currency of that region started to flock to Bangladesh market, particularly with offshore banking; borrowing from offshore under the trade-based financing (UPAS and buyer's credit) was allowed by BB through BRPD circular No-28, 2010; the borrowers are becoming aware of the financing in FC through another widow of the domestic banks; evolvement of negative rate of interest in the developed countries which forced the banks of those countries to find the lucrative market for placement of their investment; increasing confidence of international lenders in Bangladesh economy; the higher trade cost in local currency, and no cap on single borrower exposure limit in borrowing from abroad.

CRITERIA FOR GETTING LOAN FROM OFFSHORE BANKING: Those who have foreign currency earnings are encouraged to be eligible to use foreign currency loan from offshore banking units (OBUs). The intending borrower should be a non-resident. The resident enterprises must have regulators' (BIDA/BEPZA/BEZA) approval for obtaining foreign currency denominated loan. The industrial enterprises should have industrial import registration certificate (IRC) given by the Chief Controller of Import and Export (CCI&E).The deemed or indirect exporters exporting against the back-to-back LC issued by the lien bank of exporter: Permission is required from the domestic regulators if the borrower is staying in the domestic tariff area. But the non-resident borrowers are not required to take permission from the regulators; no Objection Certificate is required from the BEPZA, if the borrower is a type-A enterprise in the Export Processing Zone (EPZ); up-to-date information of the borrower from the Credit Information Bureau (CIB) of Bangladesh Bank; the debt burden ratio should be reasonable so that the enterprises' own finances are used in the most part of the company's capital expenditure; being the lower leveraged enterprises it saves the country's foreign currency if default or calling-up any loan; no stressed loan of the borrower; borrower has all licences and permits to conduct its business; all corporate records of the borrower are up-to-date; borrower is an environmentally compliant company; borrower has obtained all industry standard certification (e.g. ISO certification); borrower is a labour law compliant company with no child labour, and borrower or the project is properly insured.

SOURCE OF FUND OF OFFSHORE FINANCE CENTRES: An offshore banking unit of a bank is a completely separate entity from the domestic banking unit. A separate but dependent entity of the bank, offshore financing has no authorised and paid-up capital to initiate business. For running its foreign currency denominated balance sheet, the offshore financial centres are sourcing fund mainly from other offshore centres, balance of the deposits accounts of offshore enterprises and individuals and own bank's treasury.

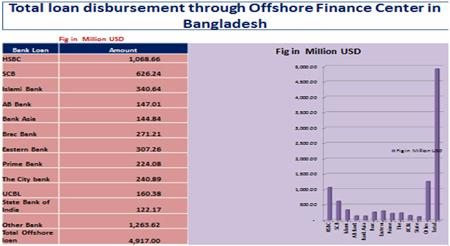

Offshore banking has disbursed almost $5.0 billion so far, but the system has been running only on Bangladesh Bank circulars from 1985, including the latest one issued in 2010. The danger of abusing the offshore finance centres is there if proper guidelines are not set by BB. (The article has been abridged.)

The writer is the Head of Offshore Banking

at Bank Asia Limited

tanhimtahmin1973@gmail.com