Nano loans surge as early wage access platforms reshape worker finance

ISMAIL HOSSAIN | Saturday, 7 March 2026

Bangladesh's nano loan and earned wage access (EWA) market is expanding rapidly as digital payroll systems, rising living costs and growing fintech adoption increase demand for short-term liquidity among low-income workers.

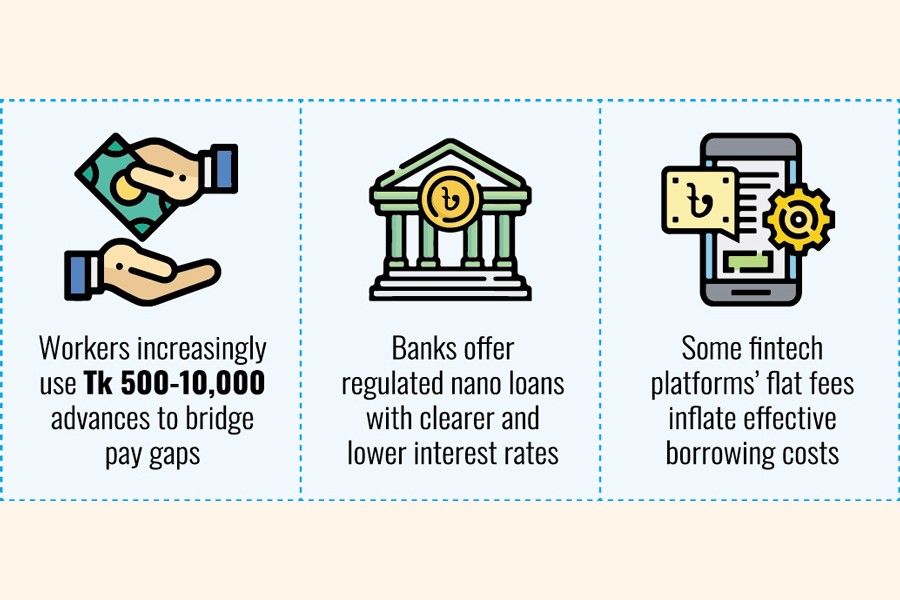

Small-ticket advances -- often ranging between Tk 500 and Tk 10,000 -- are increasingly being used by workers to bridge cash-flow gaps between pay cycles.

Commercial banks have already entered the segment with regulated and transparent pricing structures.

BRAC Bank offers its Shafollo-RMG facility at 16 per cent per annum, translating to roughly Tk 1,600 in yearly interest on a Tk 10,000 loan.

Dhaka Bank provides nano loans at 9.0 per cent per annum plus a 0.5 per cent processing fee, bringing the annual cost to about Tk 950 for a Tk 10,000 loan.

Bank Asia also offers app-based nano loans at around 9.0 per cent annually for tenures of up to six months, with fully digital application and repayment processes.

Fintech payroll platforms have also begun offering similar services. Agam, for instance, charges payroll-linked clients 9.0 per cent interest plus a 0.5 per cent processing fee, while non-payroll clients pay 14 per cent interest with an additional 0.5 per cent processing fee.

The model broadly mirrors conventional banking practices and provides borrowers with a clear understanding of interest rates and total repayment obligations.

The rapid growth of nano-credit and wage-access services in Bangladesh reflects a broader international trend.

However, analysts warn that the fee structures used by some nano-loan platforms can lead to significantly higher effective borrowing costs than conventional bank lending.

For example, certain slab-based pricing models charge fixed service fees rather than clearly stated interest rates.

A Tk 5,000 advance with a Tk 120 fee for a one-month period implies a monthly rate of about 2.4 per cent -- equivalent to roughly 28.1 per cent on an annualised basis.

If the same advance is repaid within 15 days, the effective annualised rate could rise to nearly 67 per cent.

Industry observers say such pricing structures may obscure the true cost of borrowing because the fee is not presented as an annualised interest rate.

One platform operating in Bangladesh, Wagely, uses a slab-based fee structure in which workers pay Tk 120 for advances between Tk 500 and Tk 6,000, and Tk 150 for advances between Tk 6,000 and Tk 10,000.

While these charges may appear small in absolute terms, the effective annualised borrowing costs can far exceed those charged by banks, particularly when the repayment period is short.

Contacted, a senior banking official declined to comment on the comparatively high charges associated with such models.

Financial analysts say that compared with regulated bank lending -- typically ranging between 9.0 per cent and 16 per cent per annum -- repeated reliance on short-term advances with flat fees can substantially raise borrowing costs for workers.

Internationally, fintech platforms such as Earnin and DailyPay in the United States allow workers to access a portion of their earned wages before payday. These services generally charge subscription fees or voluntary "tips" instead of conventional interest.

In the United Kingdom, Wagestream partners with employers to offer early wage access, typically charging a small flat transaction fee.

The UK's Financial Conduct Authority has encouraged transparency in such services and is examining how they should be regulated as the sector grows.

Across Southeast Asia, similar platforms are emerging in Indonesia, Vietnam and the Philippines, where regulators are closely monitoring the sector to ensure that digital micro-credit products do not carry hidden costs or excessively high effective interest rates.

Meanwhile, some platforms are experimenting with alternative models that avoid interest-based borrowing.

Grocery and agri-supply platforms such as Apon Bazar and Agroshift provide limited deferred-payment facilities, where financing costs are absorbed through product pricing or supply-chain arrangements rather than direct interest charges.

Such approaches highlight the potential for safer and lower-cost credit mechanisms if designed carefully.

While Bangladesh Bank has encouraged digital financial inclusion and fintech innovation, detailed regulatory guidelines for earned wage access and nano-credit products operating outside traditional loan frameworks remain limited.

bdsmile@gmail.com