NBFIs’ profits halve in H1 as interest spread hits historic low

New market-driven interest rates will boost profits in H2, say businesses

BABUL BARMAN | Monday, 7 August 2023

Non-bank financial institutions' (NBFIs) overall profit halved year-on-year in the first six months of this year, owing to rising costs of funds rendered by shrinking interest spread.

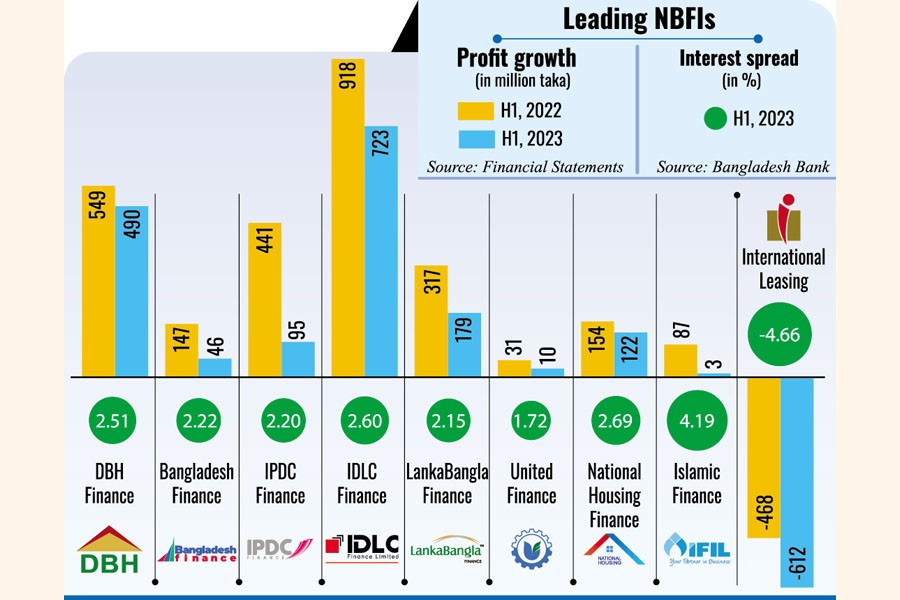

The gap between borrowing and lending rates came down to a historic low at 0.27 per cent on an average in June for the NBFI industry, while it was 0.75 per cent for January-June this year, according to the Bangladesh Bank data.

"The main business of the non-bank financial institutions was hit due to the narrowing of the gap between the interest rate on deposits and the lending rate," said Mominul Islam, managing director & CEO of IPDC Finance.

Interest spread of International Leasing [among the nine that disclosed earnings] and eight others, which are yet to make disclosures, turned negative up to 11.36 per cent in June, meaning they offered higher interest rates on deposits than what they charged against loans.

Market insiders said the NBFIs had to narrow the gap between borrowing and lending rates to stay in business, as weaker financial institutions offered higher rates to attract savers amid a liquidity crunch. That inevitably took away a major chunk of profits.

This happened against the backdrop of dwindling deposits in banks and other financial institutions amid raging inflation and economic distress.

NBFIs normally offer higher rates than banks to encourage both institutional and individual depositors to choose them for investments.

When some banks offered deposit rates as high as 8 per cent in the wake of a liquidity crunch, many institutional investors moved their money from NBFIs to banks for higher returns.

To remain in business, weak NBFIs started offering higher rates, driving their costs of funds higher. But the lending rate was capped at 11 per cent for NBFIs up until June this year. Hence, the interest spread kept shrinking, hurting the business.

Moreover, provision for loans and investments coupled with lower income from the stagnant stock market eroded their profits.

The Investment Corporation of Bangladesh (ICB), for example, saw a 70 per cent decline in profit to Tk 490 million in the nine months through March this year, compared to the same period of the previous year, as it failed to generate expected capital gains.

"We could not sell-buy shares due to the floor price [of securities]," said Md Abul Hossain, managing director of the ICB.

The Corporation's capital gains slumped 59 per cent year-on-year to Tk 2.61 billion in the nine months to March. ICB's financial year begins on July 1.

Earnings of all nine NBFIs that published half-yearly financial reports dropped between 11 per cent and 97 percent year-on-year. One among them, International Leasing saw a negative growth of its profit compared to the first half of 2022.

Of the 23 listed NBFIs on the Dhaka Stock Exchange, five others have not released data for several quarters while their financial condition deteriorated due to widespread scams and irregularities.

The rest are yet to publish financial reports.

The aggregate profit of the nine NBFIs plummeted 51 per cent year-on-year to Tk 1.06 billion in January-June this year.

Industry insiders partly blame the lower profits on the pile-up of non-performing loans. Asset quality of a number of scam-hit NBFIs has worsened drastically.

There are expectations that the industry will experience a turnaround in the coming months for the new interest rate regime introduced in the latest monetary policy of the Bangladesh Bank.

Since July 1 this year, the maximum deposit rate of NBFIs is SMART (six-month moving average rate of treasury bills) plus 2 per cent while the maximum lending rate is SMART plus 5 per cent.

Currently, the six-month moving average rate of treasury bills is 7.10 per cent, which may change. The flexible, market-driven rate created a wider space for the businesses to maneuver.

IPDC's profit plunged 78 per cent to Tk 95 million in the first half of this year, although its April-June quarterly profit soared to Tk 80 million, about five times what it earned in the previous quarter.

The quarter-on-quarter improvement in performance indicates a turnaround point. The second half should be better as the company eyes faster recovery supported by a wider interest spread.

LankaBangla Finance's consolidated profit fell 45 per cent year-on-year to Tk 179 million in January-June while Bangladesh Finance too reported a 69 per cent year-on-year decline in its consolidated profit to Tk 46 million due to lower interest income and sluggish stock market trading.

Islamic Finance and Investment logged the highest profit erosion, 97 per cent, as the company suffered a loss of Tk 5.6 million in the April-June quarter due to increase in provision and profit suspense against non-performing loans.

It disbursed loans amounting to Tk 3.72 billion in 2022 without any eligible security, such as a mortgage or a lien on shares, according to its independent auditor.

DBH Finance, the largest and specialised housing finance institution in the private sector, saw the lowest, 11 per cent, year-on-year decrease in profit in January-June.

Meanwhile, eight listed NBFIs --- Bangladesh Industrial Finance, Fareast Finance, FAS Finance, First Finance, International Leasing, Peoples Leasing, Premier Leasing, and Union Capital --- are trading below the face value of Tk 10 each share.

Scam-hit four financial institutions -- People's Leasing, International Leasing, BIFC and FAS Finance -- are struggling to repay their depositors upon maturity of the schemes.

Prashanta Kumar Halder, former managing director and CEO of NRB Global Bank, who was arrested last year in India, had been charged with embezzling a huge amount of money from the four NBFIs. He had taken control of the financial institutions by buying shares anonymously.

Due to widespread scams in some NBFIs, the overall volume of non-performing loans of the industry jumped nearly 25 per cent to Tk 178.55 billion at the end of March, according to the central bank.

People's Leasing and Financial Services bore the highest amount of non-performing loans, 99.62 per cent, followed by Bangladesh Industrial Finance 96.90 per cent, Fareast Finance 94.25 per cent, International Leasing and Finance 90.93 per cent and First Finance 89.63 per cent until March.

babulfexpress@gmail.com