NPL surge triggers systemic banking shock

JASIM UDDIN HAROON | Sunday, 14 December 2025

Bangladesh is facing a growing "systemic shock" from non-performing loans (NPLs), with bad debts reaching record highs in 2024-25 and laying bare deep vulnerabilities in the country's banking sector.

The sharp deterioration in asset quality has constrained banks' ability to lend and raised fresh concerns over financial stability, according to an analysis prepared by the Policy Research Institute of Bangladesh (PRI) and shared at a recent event.

A systemic NPL shock refers to a severe and widespread decline in loan quality across the banking system, affecting multiple institutions simultaneously.

In Bangladesh, this phenomenon has intensified rapidly, driven by long-standing governance failures, weak loan recovery mechanisms and a tightening of classification rules.

The PRI analysis warns that without a comprehensive, system-wide mechanism to resolve distressed assets, the mounting burden of bad loans could further erode bank capital and undermine confidence in the financial system.

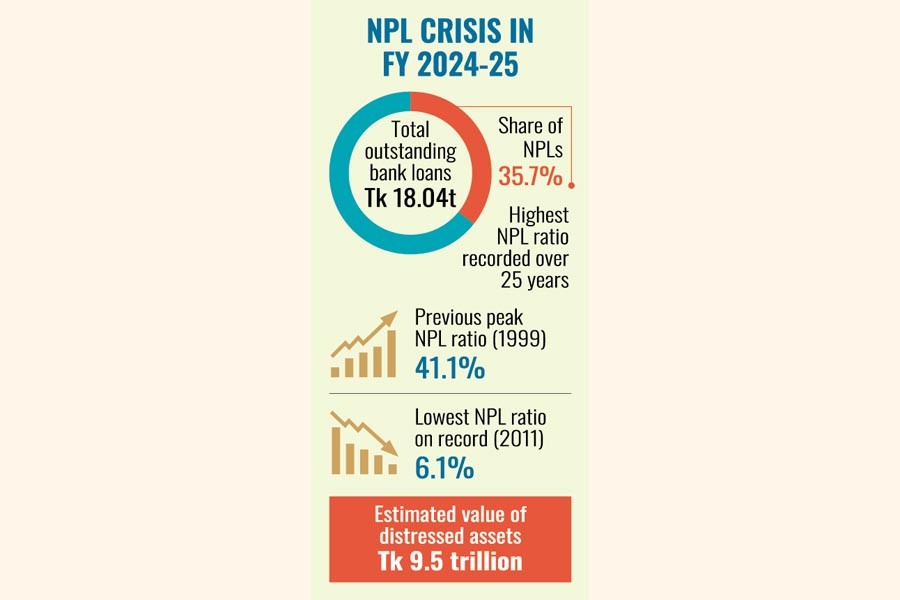

The NPLs rose by 42.75 per cent in the final quarter of fiscal year 2024-25, which ended in June. Total non-performing loans now account for 35.7 per cent of Tk 18.04 trillion in outstanding credit, marking the highest ratio in 25 years.

The NPL ratio previously peaked at 41.1 per cent in 1999 before declining steadily to an all-time low of 6.1 per cent in 2011. Since then, it has reversed course and continued to rise.

The Policy Research Institute estimates that distressed assets may now total around Tk 9.5 trillion. "NPLs climbed to record levels through late 2024-25, constraining banks' credit capacity and eroding capital," the study said.

From April 2025, stricter loan-classification rules, under which loans overdue by three months are deemed non-performing, significantly inflated reported bad loans, the analysis found.

Despite an increase in absolute recoveries, overall recovery rates remain weak, with around 222,000 default cases trapped in slow-moving court processes.

The report argues that a dedicated, system-wide NPL resolution mechanism is no longer optional but essential for maintaining banking stability.

A large share of defaults, it noted, stems from fraud, insider lending and unenforceable or missing collateral, leaving many loans with little realistic prospect of recovery.

PRI said Bangladesh's situation differs from that of countries such as the United States, the United Kingdom, China and Malaysia, where NPL pressures have emerged under different macroeconomic and institutional conditions.

In Bangladesh, high inflation persists alongside weak legal enforcement and chronic governance failures, compounding the problem.

Meanwhile, the government has included the creation of an asset management company (AMC) in its national resolution toolkit.

The finance ministry has already drafted a distressed asset management ordinance, with completion targeted by June 2026.

The proposed ordinance aims to establish a centralised vehicle to manage and resolve non-performing loans across the banking system.

jasimharoon@yahoo.com