Burden builds up on banks, citizens

NPLs reach record-high Tk 2.11tn

JASIM UDDIN HAROON AND JUBAIR HASAN | Wednesday, 4 September 2024

Banks' non-performing loan (NPL) volume reaches a record-high of over Tk 2.11 trillion as of last June-end, official statistics show and economists worry over its domino effect.

Bankers and economists say the pressure on the banking sector continues mounting under the load of NPLs or classified loans and weakens the financial health of the key financial sector.

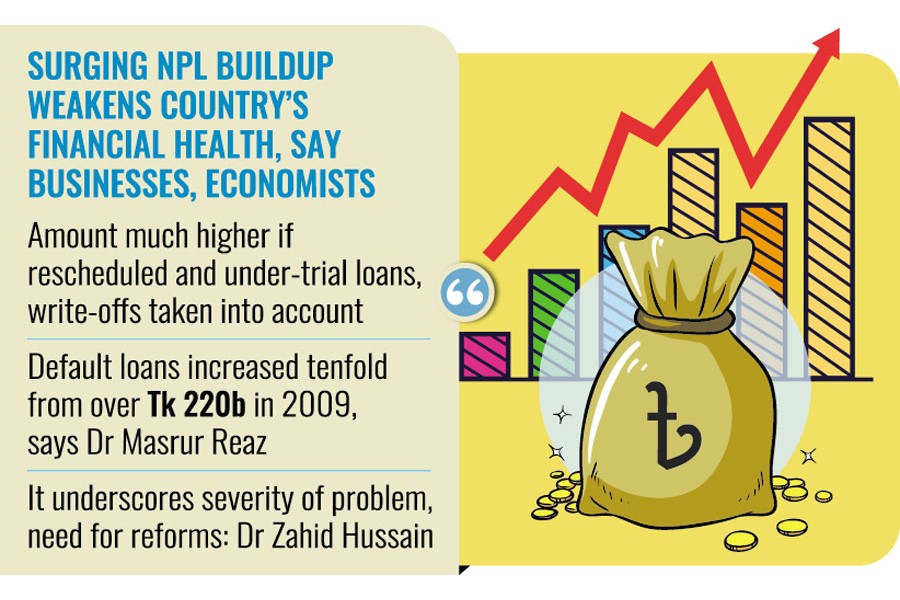

In fact, they think, the actual size of the stressed assets in banks would be much higher than the NPL amount if the volumes of loan rescheduling, under-trial disputed loans and write-offs are taken into account.

According to the central bank data released Tuesday, the bad loans increased by over Tk 290 billion in just three months from March 2024 when the volume of classified loans was over Tk 1.82 trillion.

At the end of June this year, the total disbursed loans stood at Tk 16.83 trillion, of which Tk 2.11 trillion became defaulted-the highest in the history of Bangladesh.

With this latest surge, the overall ratio of NPLs or classified loans stood at 12.56 per cent - 1.45-percentage-point higher than the March figure.

In terms of the category of banks, the volume of classified loans in the state-owned commercial banks (SCBs), like on other occasions, remained high in total outstanding.

The total outstanding loans from the SCBs stood over Tk 3.13 trillion until June 2024, of which Tk 1.02 trillion or 32.77 per cent got defaulted. The volume of bad loans in the SCBs surged by 5.77 percentage points in June from 27 per cent recorded over the March-end period. The share of NPLs for private commercial banks (PCBs) increased 0.35 percentage points to 7.94 per cent or Tk 992 billion against their disbursed loans worth Tk 12.59 trillion.

The share of dud loans for foreign commercial banks (FCBs) against their outstanding of Tk 681 billion dropped to 4.74 per cent (Tk 32.29 billion) until June last from 5.20 per cent.

The rise in bad loans is also observed in the operations of specialised banks where the ratio of NPL declined to 13.11 per cent (Tk 57.56 billion) out of their outstanding loans of Tk 439 billion in June from 13.88 per cent recorded three months earlier, according to the official data.

Talking to the FE, Bangladesh Bank spokesperson Md Mezbaul Hoque said the rise in the volume of NPLs in the country's banking industry is concerning. He said they just received the NPL-related data and would soon start examining the factors contributing to the surge and take actions accordingly.

Seeking anonymity, a BB official mentioned that the central bank in early February announced a roadmap with 11-point measures to cut the NPL stress down 8.0 per cent by June 2026.

"Where are the measures? Why has it (NPL) increased significantly?" the official raises questions over implementation of the NPL-containing steps.

The burden will not be reduced only for making strict statements. It will be lessened if the steps are periodically implemented, the central banker said. Managing director and chief executive officer of Dhaka Bank Emranul Huq says it is very alarming as the volume of bad loans keeps soaring. The banks need to pay more focus on cash recovery to cut down the burden.

Prominent economist Professor M.A. Taslim notes that the growing amount of NPLs is not just a burden for the banks but also burden for the common people as banks will pass it on to the people by raising the cost of funds with its cascading impact.

Dr Zahid Hussain, former lead economist of the World Bank's Dhaka office, told the FE that the reported non-performing-loan figure represents the lower bound of distressed assets in the banking system.

"The reported amount is based on lax NPL-recognition criteria, where loans are considered overdue after 180 days or more. The amount would be significantly higher if the 90-day rule was applied," he said.

The fact that the NPL amount is so high even under these lenient criteria underscores the severity of the problem and the urgent need for reforms to address it.

"Equally important are reforms that will help prevent the growth of NPLs going forward," Dr Hussain notes.

Dr M. Masrur Reaz, Chairman and CEO of the Policy Exchange of Bangladesh, also spoke to the FE from abroad through WhatsApp, stating that banks forcibly acquired by certain business groups, including S Alam Group, should have their shares divested to qualified foreign investors to inject new funding.

He stresses identifying the reasons behind the rising NPL buildup and bringing the wilful defaulters who benefit from these practices to justice.

"These individuals may be within the banks, outside the banks, or even within political circles," he notes about what are dubbed vicious circles.

Dr Masrur points out that over the past 15 years, default loans have increased tenfold as the volume of classified loans was over Tk 220 billion at the end of 2009 when Awami League government came in power after eight years.

"There are many reasons behind the high level of NPLs, but one key factor is government patronage at the highest level," he says.

He further states that this patronage from above has undermined discipline in the banking system.

"Politically aligned groups have taken control of bank boards, rendering them ineffective and destroying their efficiency." And these groups have also been involved in "hostile takeovers of banks, and the role of the central bank has been severely compromised by government actions at the highest level, leading to the current NPL crisis in the banking system," the economist concludes.

jasimharoon@yahoo.com and jubairfe1980@gmail.com