Plastic money boom amid Bangladesh's uneven cashless shift

Sajibur Rahman | Sunday, 24 May 2026

From supermarket checkouts and online shopping carts to utility bills, overseas travel and freelance payments, plastic money is rapidly reshaping how Bangladeshis spend, save and transact. And this transition signals a major shift toward a more digitally connected and cashless economy.

Bangladesh's card-based payment ecosystem has undergone a remarkable transformation over the past five years, driven by rapid digitisation, changing consumer behaviour and stronger financial connectivity across the country.

Nowadays, cards have become one of the most widely used means of transaction globally, with many countries increasingly relying on plastic money for everyday payments. In Bangladesh, a growing segment of the population is now using debit, credit and prepaid cards for shopping, travel, utility payments and online transactions, although many people still remain reluctant to use cards due to limited awareness and fears related to digital transactions and security.

In this context, Bangladesh Bank launched an initiative in 2012 to expand the use of plastic money and promote a cashless banking system powered by information technology. To strengthen the legal foundation of the payment ecosystem and protect consumer interests, the Payment and Settlement Systems Act 2024 came into effect on November 4, 2024.

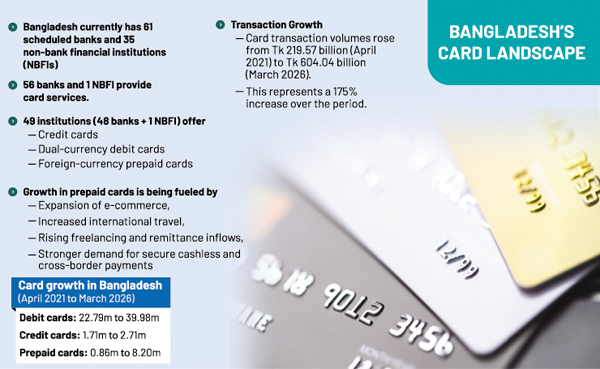

Currently, 61 scheduled banks and 35 non-bank financial institutions (NBFIs) operate in Bangladesh, of which 56 banks and one NBFI are providing card services. Among these institutions, 49 entities -- including 48 banks and one NBFI -- are offering services such as credit cards, dual-currency debit cards and foreign-currency prepaid cards.

The rapid growth of prepaid cards in the country is being driven by the expansion of e-commerce, rising international travel, growth in freelancing and remittance inflows, and increasing consumer demand for secure cashless and cross-border transactions.

According to Bangladesh Bank, the number of debit, credit and prepaid cards issued as of April 2021 stood at 22.79 million, 1.71 million and 0.86 million respectively.

By March 2026, the debit, credit and prepaid card numbers had risen to 39.98 million, 2.71 million and 8.20 million respectively, reflecting an overall growth of 101 per cent across the three card categories.

Meanwhile, transaction volumes through these cards increased from Tk 219.57 billion in April 2021 to Tk 604.04 billion by March 2026, marking a 175-percent growth over the five-year period.

Top bankers and payment -industry leaders say the country's card ecosystem is now entering a new phase of growth, supported by the rapid expansion of e-commerce, digital lifestyle platforms, QR-based payments, virtual cards, cross-border transactions and rising consumer confidence in secure digital payment.

They said growing international travel, freelancing income, remittance inflows and the increasing shift toward online transactions are creating major opportunities for banks to expand prepaid, dual-currency and virtual -card services across different customer segments.

Bankers also have noted that investments in EMV-secured CHIP and PIN cards, two-factor authentication, tap-and-pay solutions and QR-based payment systems are strengthening the country's digital payment infrastructure and improving transaction security.

However, they warn that several structural challenges continue to slow wider adoption of card-based transactions, including limited digital infrastructure in rural areas, the high cost of smartphones and POS machines, low digital financial literacy, cybersecurity threats and the growing shift of rural customers toward mobile-financial services instead of traditional debit cards.

Industry leaders also say regulatory barriers, including mandatory TIN requirements for credit cards, along with weak merchant- acceptance infrastructure outside major urban centres, remain obstacles to faster growth in the cashless-payment ecosystem.

They have stressed that stronger policy support, lower duties on smart devices and payment equipment, improved cybersecurity awareness and broader collaboration among banks, regulators and payment networks will be essential to building a more inclusive and digitally connected cashless economy in Bangladesh.

Syed Mohammad Kamal, Country Manager, Bangladesh, Mastercard, says: "Debit cards are increasingly emerging as an important gateway to formal financial inclusion in Bangladesh. As consumers become more inclined toward safer, faster, and more transparent payment methods, debit cards are driving everyday transactions across grocery, transportation, healthcare, education, and e-commerce."

The growing adoption of cashless and digital banking services also reflects rising consumer confidence in digital payments and Bangladesh's broader digital transformation journey, he adds.

Many countries of the world have made Debit-card issuance mandatory with every CASA account issuance. In Bangladesh, this is still an option, which needs to be reviewed by regulators, Kamal points out.

At the same time, innovation in the debit card is rapidly evolving in the country. From the introduction of dual-currency debit cards to enabling more secure experiences coming through the country's first numberless debit card launched with Prime Bank or Debit Sticker Cards, he says.

Mastercard continues to work closely with partner banks to bring innovative and customer-centric solutions to the market.

However, realising the full potential of debit cards requires stronger ecosystem-wide collaboration. Expanding acceptance infrastructure beyond major urban centres, increasing cybersecurity awareness, and improving digital financial literacy at the grassroots level remain key priorities, he notes.

"At the same time, lowering the existing high duties on smart cards and POS machines could help accelerate merchant acceptance and encourage greater investment in payment infrastructure. A supportive policy environment, combined with innovation and trust, will play a critical role in advancing inclusive digital payments in Bangladesh," Kamal suggests.

M. Khorshed Anowar, Deputy Managing Director, Head of Retail & SME Banking, Eastern Bank PLC, says: " Over the past five years, we have seen significant growth in the usage of debit, credit, and prepaid cards across different customer segments, driven by convenience, security, and the expansion of digital commerce."

One of the key drivers behind this shift is the remarkable growth of e-commerce, online services, and digital -lifestyle platforms. Customers are now more comfortable making payment digitally for everyday needs, including shopping, utility bills, travel, healthcare, and entertainment.

"We have continuously focused on developing innovative solutions to meet evolving customer needs. Products such as the EBL Aqua Prepaid Card and the Daraz EBL Cobrand Prepaid Card have received strong market response by addressing specific customer segments and transaction requirements", he says as an instance of advances on the latter-day financial front.

EBL issues EMV-secured CHIP and PIN-based cards, which provide significantly stronger protection compared to traditional magnetic stripe cards, Anowar adds.

To further strengthen online- transaction security, Eastern Bank has implemented 3D Secure technology with two-factor authentication for e-commerce transactions, according to him.

The bank is continuously expanding the deployment of ATMs, CRMs, QR-based payment solutions, and POS machines to make banking and digital transactions more accessible and convenient for customers across the country, he adds.

Md. Altaf Hossain, Managing Director (Current Charge) of Islami Bank Bangladesh PLC, says a key driver behind Islami Bank's accelerated digital card adoption has been its migration to an advanced backend platform capable of seamlessly handling high-volume transactions across Visa, Mastercard and UPI networks.

In addition, the growing popularity of the bank's Cellfin app has further strengthened the shift toward digital payments through innovative features such as versatile virtual cards and frictionless tap-and-pay solutions, according to Hossain.

As a leading Shariah-based lender, his bank remains committed to strengthening the digital -payment ecosystem through innovative card solutions, enhanced cybersecurity, financial -literacy initiatives and broader access to modern banking services for underserved and unbanked communities nationwide.

As the country's largest Shariah-based bank, Islami Bank is expanding its prepaid and dual-currency card portfolio through solutions such as Hajj Prepaid Card, CellFin Virtual Card, Union Pay International cards and SME cards to meet evolving customer needs, Hossain points out.

The bank is also strengthening its cross-border payment capabilities through partnerships with global payment networks, QR-based payment systems, and remittance integration, enabling safer and more convenient international transactions for travelers, freelancers, and expatriates, he mentions.

"Furthermore, by aggressively deploying low-cost Bangla QR merchant- payment solutions across rural bazaars, the bank converts daily cash-reliant micro-transactions into secure digital settlements. Ultimately, this comprehensive strategy ensures that underbanked communities gain equitable access to global payment networks and Shariah-compliant digital banking, driving grass-roots financial inclusion nationwide," he adds.

The bank is also expanding customer -awareness initiatives on phishing, cyber-fraud, and safe digital banking practices while deploying secure QR and POS transaction ecosystems nationwide.

Syed Mahbubur Rahman, Managing Director and CEO of Mutual Trust Bank PLC, appreciates that the country's card-based payment ecosystem is playing an important role in advancing a cashless economy. "Plastic cards still have value and importance."

He says that MTB is set to introduce a virtual debit card soon.

He notes that some customers are shifting from debit cards to mobile financial services (MFS), particularly in rural areas where setting up ATMs is not always commercially viable.

"It is not possible to establish ATMs in many remote rural areas. As a result, people there are increasingly relying on MFS services," Rahman says.

He stresses the need for supportive government policies to accelerate digital financial inclusion, especially by making smartphones more affordable.

"The government should shape the duty structure in a way that helps people buy smartphones within Tk 5,000 to Tk 6,000. Mobile handsets need to become cheaper," he suggests.

He says some people are still reluctant to use debit cards, while the requirement of a Tax Identification Number (TIN) for obtaining credit cards remains a barrier to wider adoption.

"Although the number of debit and credit cards has increased over the years, growth is still below the expected level," MTB MD notes.

sajibur@gmail.com