Policy implications of current account deficits

Zaid Bakht | Sunday, 20 March 2022

In a developing country like Bangladesh, the overall trade balance (which shows the gap between imports and exports of goods and services), is usually negative as the import needs of such countries often exceed their export capabilities. In the national income accounting framework, the trade balance is the counterpart of resource balance that shows the difference between domestic savings and investment. So, one can say that the higher investment needs compared to the lower level of domestic savings in these countries translate into a negative trade balance.

Apart from the trade flows, the external sector also involves primary and secondary income flows. The main component of primary income is Net Factor Income (profit, interest etc.) that accrues from abroad. In Bangladesh, this item has been negative historically, due to the underdevelopment of the economy.

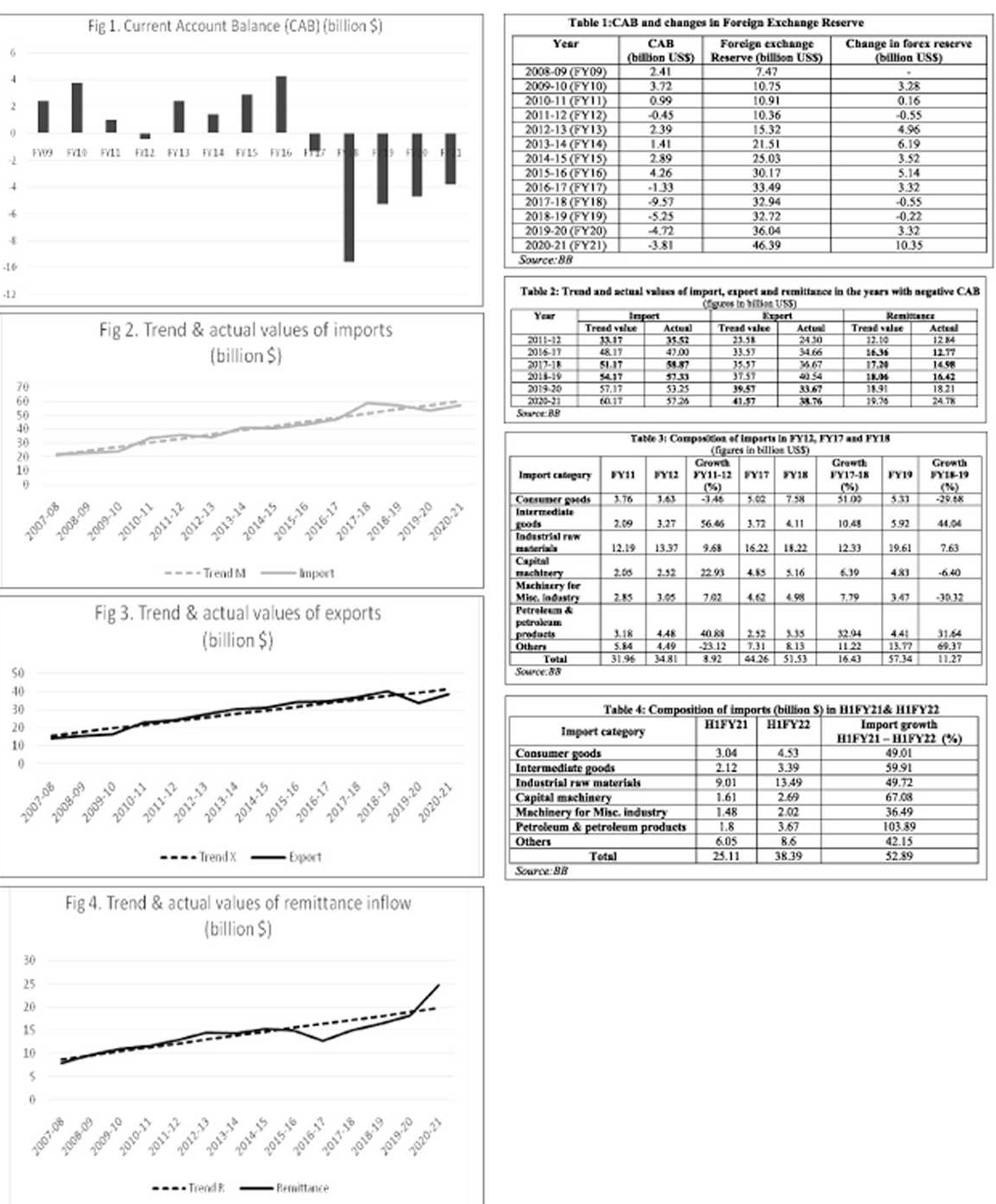

However, in the case of Secondary income, the dominant element of which is Net Workers' Remittance, Bangladesh enjoys a big surplus. The current account balance (CAB) is obtained by adding Primary and Secondary income to the overall trade balance. In Bangladesh, CAB was positive in seven out of the last 13 years (FY 09 - FY 21), while it was negative in the other six years (Fig 1).

As is evident from Fig 1, CAB in FY 12 was only marginally negative. The largest negative CAB was observed in FY 18 but since then the deficit in the current account has been steadily declining.

Negative CAB means that the current account outflow of foreign currency is more than the inflow of the same. In terms of national income accounts, it implies that the national savings is not large enough to finance our investment.

It should be clear, however, that a negative CAB does not necessarily mean that the foreign exchange reserve will decline as the net outflow of foreign exchange on current account may be more than offset by the net inflow of foreign exchange on capital account, which includes items such as foreign investment, foreign aid and grants etc. In fact, of the last six years in which CAB was negative in Bangladesh, foreign exchange reserve marginally declined in three years (FY12, FY18 & FY19), and the reserve actually increased in the other three years despite CAB being negative (Table-1). Clearly, if foreign exchange reserve and net capital inflow are healthy, there is no immediate reason to panic due to a negative CAB.

To figure out an appropriate policy response to negative CAB, one first needs to identify the reason behind CAB turning negative. The above discussion suggests that the CAB can become negative due to one or more of the following reasons - (i) decline or slow growth in remittance, (ii) decline or slow growth in exports, and (iii) rapid growth in imports.

Table 2 presents the actual values of import, export and remittance in Bangladesh for the recent six years in which the CAB was negative along with the trend values of these variables derived from a trend line fitted to the data for last 14 years (Fig 2,3 & 4).

As can be seen from the Table, the main reason behind negative CAB in FY12, FY18 and FY19 was the significantly high actual import over the trend value. On the other hand, major short fall in actual export compared to the trend value caused CAB to be negative in FY20 and FY21. Similarly, the decline in remittance inflow in FY17 was mainly responsible for causing CAB to be negative. The actual remittance inflow fell short of the trend value also in FY18 and FY19, which further intensified the pressure on CAB already affected by high imports.

The decline in remittance inflow in FY17 was caused mainly by diversion of remittance from official to unofficial channel, commonly referred to as hundi. Several factors contributed to this process. Due to sluggish investment and import demand, there was a significant misalignment of the exchange rate with Taka experiencing appreciation while other currencies were depreciating vis-à-vis US dollar. The consequent gap between the official exchange rate and the curb market rate encouraged a shift to unofficial channels. Illegal use of mobile financial services particularly bKash, further facilitated sending of remittance through unofficial channels. Also, there were allegations that some Bangladeshi businessmen in their bid to invest abroad started mopping up remittances offering higher rates.

In FY18, import demand picked up and the misalignment of the exchange rate gradually disappeared. Bangladesh Bank asked bKash authority to investigate unauthorised use of their channel for illegal money transfer and bKash ultimately cancelled the licence of some 214 agents suspected of involvement in such hundi business. Major operators in the remittance field such as the Agrani Bank strengthened their remittance delivery capacity by setting up agent banks in potential destinations of remittance, and also through linking up with mobile financial services for quick disbursement of remittance. These measures improved the situation significantly and FY18 saw more than a 17 per cent increase in remittance inflow. The process got a further boost in 2020 when the government provided a 2.0 per cent incentive for remittance sent through official channels and this measure helped achieve a 36 per cent increase in remittance inflow in FY 21.

The decline in export in FY20 and FY21 was mainly due to the global Covid-19 pandemic that kept the CAB in the red. However, timely intervention by the government in support of the production sectors, particularly the export-oriented industries in the form of subsidised credit for wage payment and working capital requirement helped the export sector bounce back and post a healthy 15 per cent growth in export in FY21.

To design an appropriate policy response to negative CAB caused by rapid growth in import, one needs to examine the composition of the import basket. If the increase in imports is triggered by rising private/public consumption or displacement of local products by imports, the corrective measures will entail restricting non-essential imports and taking austerity measures. However, if an increase in import relates to productive expenditure involving the import of industrial raw material, intermediate and capital goods, we have a different story. Persistent growth in the import of industrial raw materials is a welcome news as it contributes to growth in output.

Table-3 shows the composition of the import basket during the three years FY12, FY18 and FY19 in which, higher than the trend level of imports were identified as the main reason behind the deficit in CAB. As can be seen from the Table, the main contributing factor behind the observed moderate deficit in CAB in FY12 was significant growth in the import of intermediate goods and capital machinery in that year. On the other hand, FY18 saw a big surge in the import of rice necessitated by flood damage of crops in that year. Consequently, import of consumer goods recorded a 51 per cent rise in the level of import causing CAB to be negative. In FY19 the need for enhanced rice import subsided but significant growth (44 per cent) in the import of intermediate good caused CAB to remain in the red zone. Also, in all three years, there has been significant growth in the import of petroleum & petroleum products. Persistent growth in petroleum imports was due to rising international price and increased imports by private power plants.

During the first half of the current fiscal year (H1 FY22), there has been sudden worsening of the situation. The half-yearly CAB plummeted to an all-time low of $-8.18 billion. This has happened because of simultaneous rapid growth in import (52.9 per cent) and decline in remittance inflow (-20.9 per cent) compared to the same period in the previous year. Export recorded a respectable growth of 28.4 per cent but this was not good enough to halt the downward slide of the CAB.

If one looks at the composition of the import basket during this period (Table 4), one finds that each and every component of import experienced a significant rise during this period. The post Covid-19 global inflation explains a large part of the rise in the import cost. In addition, the strong recovery of the post-covid economy, particularly concerning private and public investments and higher orders for apparel exports had implications for the import surge. Credit flow to the private sector registered a striking 69 per cent growth during this period.

The decline in remittance inflow can once again be attributed to the diversion of remittance money from formal to informal channels due to the emerging gap between the exchange rate prevailing in the formal market and the curb market. The gap emerged as the nominal exchange rate was allowed to depreciate at a slower pace than the rate at which the supply-demand gap for foreign exchange expanded.

Given Bangladesh's experience with deficit CAB, is there a need for major exchange rate correction? Perhaps not. We have noticed that the occurrence of substantial deficit in the CAB during the last 13 years has been rather infrequent with very little adverse impact on the foreign exchange reserve. Moreover, the deficits appeared due to some year-specific reasons and were transitory. There is no evidence of persistence or rising levels of deficit in CAB, and therefore, major adjustments in the exchange rate, are really not called for.

Because of the prevalence of somewhat higher rate of inflation in Bangladesh compared to that in the economies of the trading partners, the Real Effective Exchange Rate (REER) has shown a rising trend. Bangladesh Bank has all along followed a policy of gradual depreciation of the nominal exchange rate to prevent major appreciation of the Taka and consequent erosion of the competitiveness of Bangladeshi products. Between December 2020 and December 2021, the REER index rose from 112.47 to 115.34 indicating an appreciation of Taka by nearly 2.55 per cent. In contrast, the Nominal Exchange Rate of Taka/dollar increased from 84.90 to 85.80 showing depreciation of 1.06 per cent. So far, this policy of gradual depreciation seems to have served well both the purposes of maintaining price and exchange rate stability and attending balance of payments concerns and might as well be continued. However, if the after effects of Ukraine war exacerbates the global inflation situation, Bangladesh Bank may need to go beyond its gradual depreciation mode and make more substantive corrections in the nominal exchange rate. In the meantime, the government decision to give a 0.5 per cent incentive since January 2022 in addition to the existing 2.0 per cent incentive for sending remittance through official channels seems to be helping. Remittance inflow in January 2022 stood at $1.70 billion and is expected to reach $ 2.0 billion in March 2022. The pressure on the balance of payments is also expected to ease out as the initial post-Covid import spree, hopefully tapers off in the coming days.

Dr Zaid Bakht is Chairman, Agrani Bank Ltd. zaidbakht@gmail.com